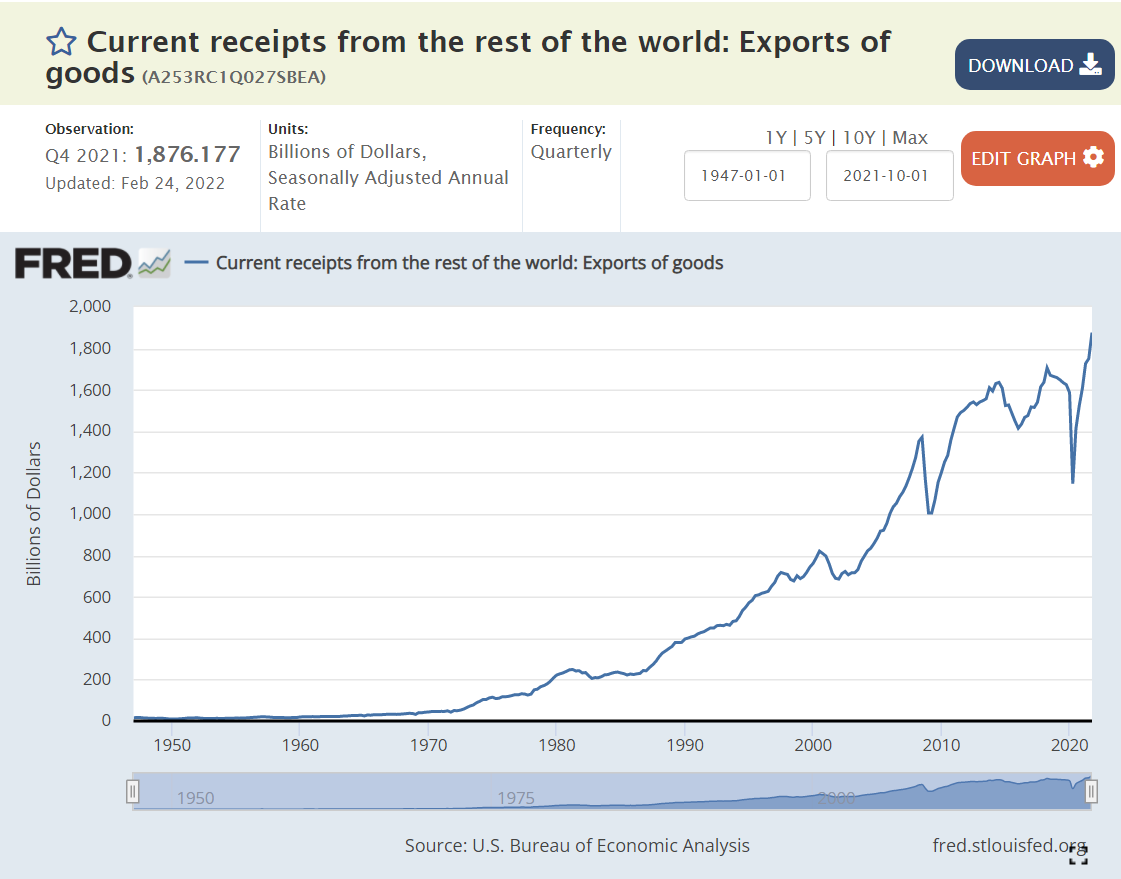

Critics complain about the US economy’s weak international performance in recent decades. Let’s set aside the trade balance (exports – imports) and focus just on exports. US exports occur when US goods and services are more competitive than ALL other countries in the world, subject to limits based upon transportation and purchasing costs, currency values and trade barriers. In real (inflation-adjusted) terms, US exports have increased by 180% since 1980, or 2.5% per year, year after year after year. Despite the 10% increased real cost of labor in the US, firms have leveraged their advantages, developed new products, found new markets and used better financing structures to greatly improve the US export results.

Total Goods and Services

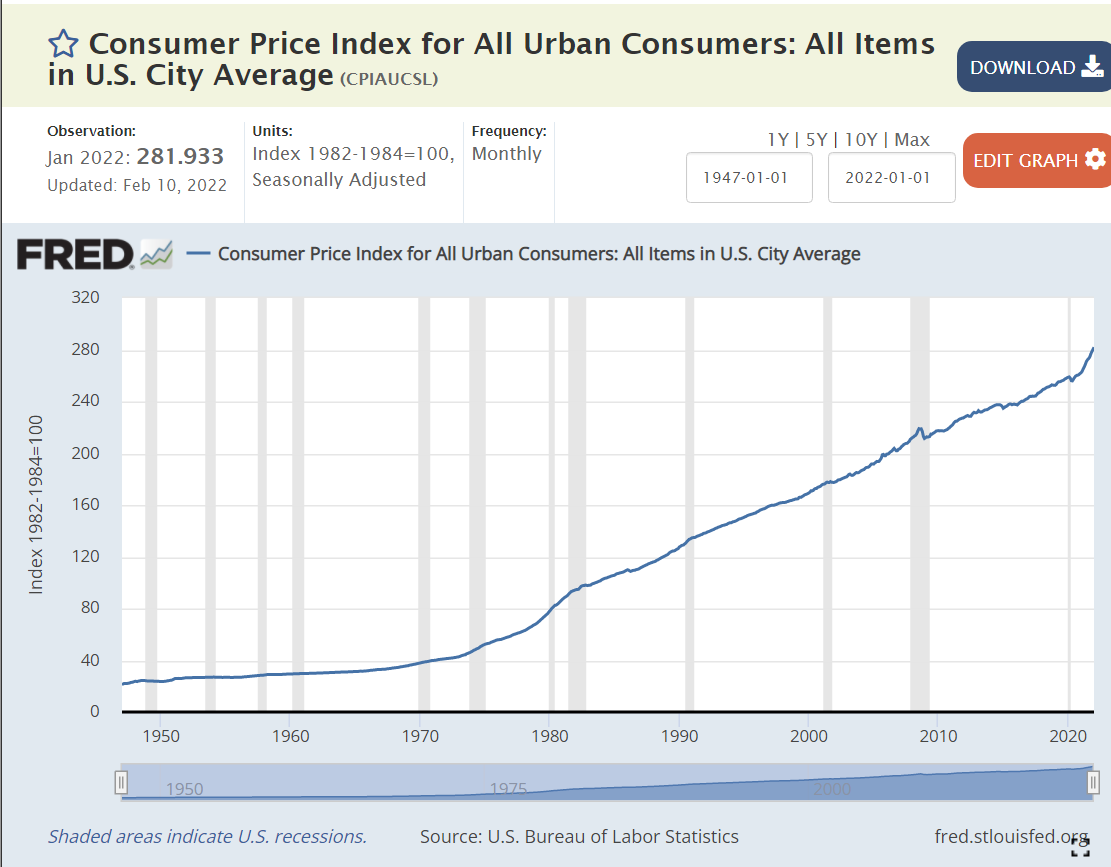

Real goods and services exports increased by 180% from 1980 until today. They increased 9-fold in nominal terms, but consumer prices increased by 230% (3.3x).

The US Dollar fell in value significantly in the 1980’s as US inflation exceeded inflation in other countries, but has since been relatively constant against a market basket of other currencies. The increase in exports is not due to a weaker US dollar.

Goods Exports

US goods exports have increased by 140% or 2.1% per year in real terms since 1980. They have fallen from 4/5ths to a little more than 2/3rds of the total as services exports have grown more rapidly.

Agriculture

Ag exports grew very rapidly in the 1970’s and then flattened through the 80’s and 90’s before rapidly accelerating in the “oughts”. Ag exports grew by 30% in real terms over these 4 decades, a little less than 1% per year.

Industrial Supplies Exports

US chemistry based and other engineered supplies and components grew by 210%, or a strong 2.8% annually.

Petroleum Exports

From zero to something, now 10% of US exports.

Capital Goods Exports

US exports of highly engineered capital goods increased by 100%, or 1.7% per year.

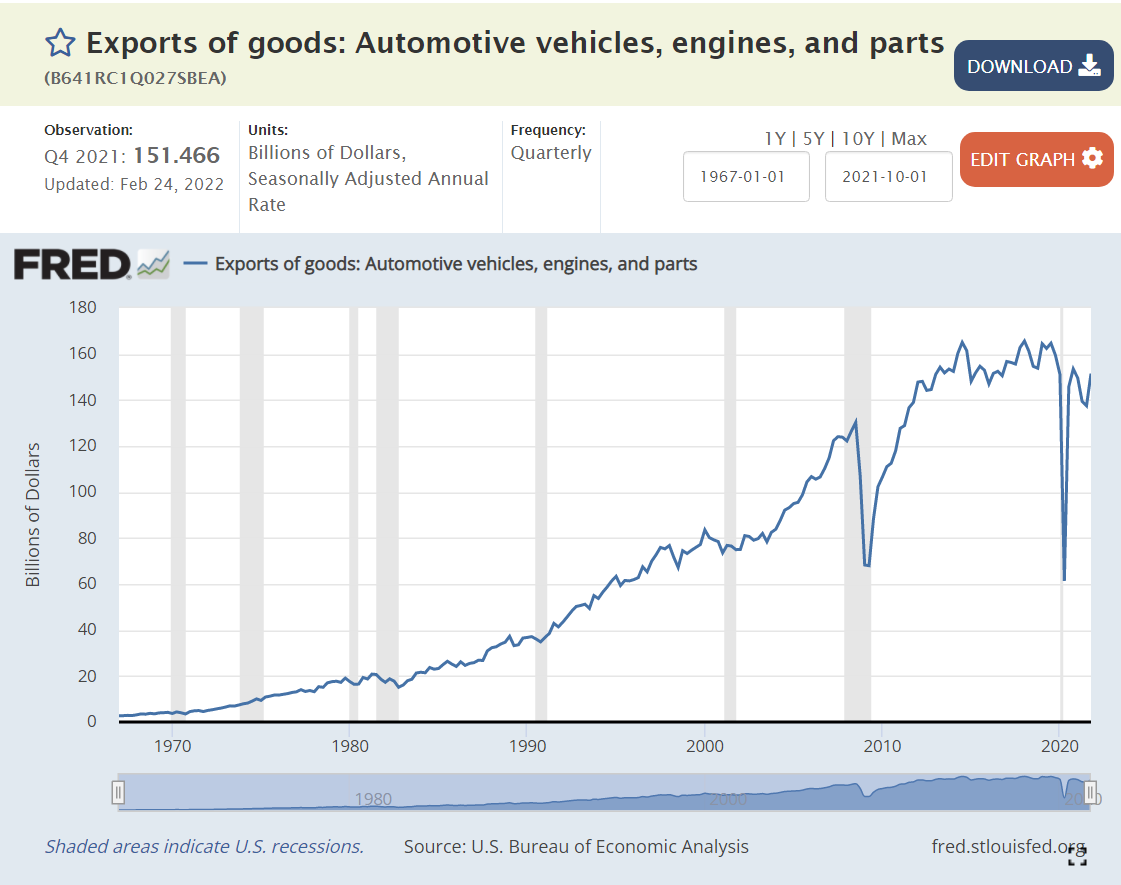

Automotive Exports

Another positive result. US auto exports are up 140% in real terms, or 2.1% per year.

Consumer Goods Exports

Miscellaneous consumer goods exports increased by 340% or 3.6% annually, an amazing performance!

Services Exports

US services exports grew by 350% in these 4 decades, by 3.7% annually. The US is very competitive in the “most competitive” areas of international trade.

Summary

The US economy continues to increase its internationally competitive real exports at a rate of 2.5% per year in the long-term. The US is very well positioned to prosper in an era of increased global and free trade.

Hotel capacity increased by 50% from 1995 to 2019.

Demand grew at the same 50% rate, although not always in lockstep.

Occupancy averaged a healthy 63% (almost two-thirds) through this period, with significant differences due to changes in construction and the economy.

The price per room averaged about $125 per night in real 2020 dollars, again varying based on supply and demand, but overall, relatively constant.

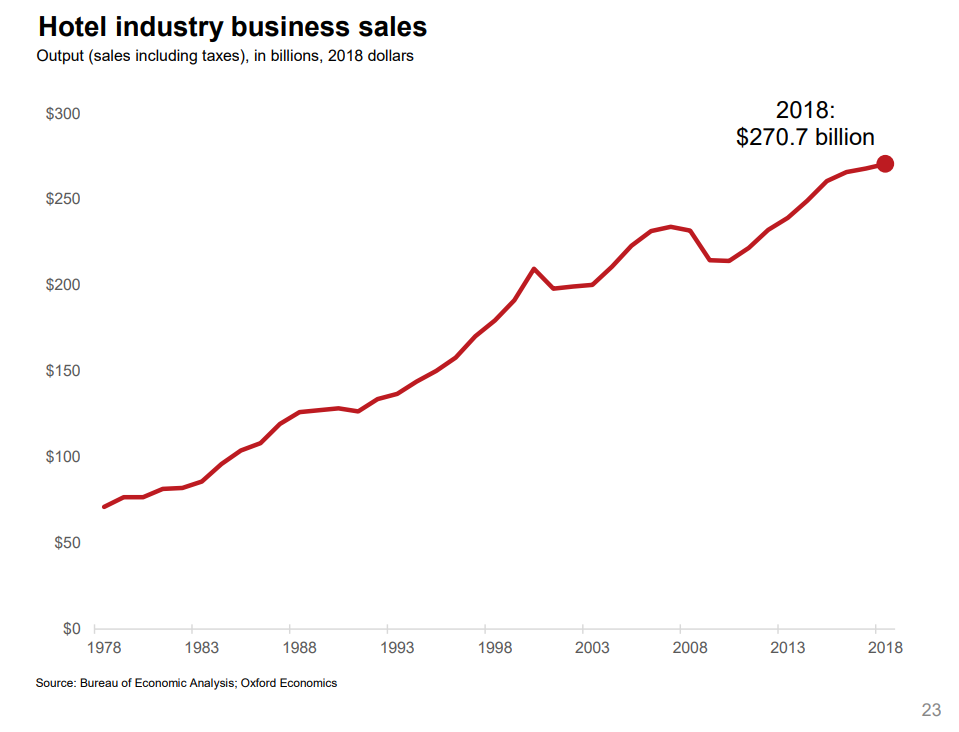

Total hotel industry real revenue ($2020) for the 21 years from 1998 through 2019 increased by a little less than 50% according to Bureau of Economic Analysis (BEA) figures.

Real consumer only (leisure) sales increased by nearly 100% during this period.

Real consumer sales per person increased by about two-thirds.

Hotel industry operating statistics before 1995 are not readily available. The tremendous growth of the industry in the last 30 years of the twentieth century is illustrated by the more than three-fold growth in industry employment, from one-half million to 1.8 million. Note that employment did not follow the growth of rooms during the first 20 years of the next century.

Oxford Economics developed an industry promotion brochure in 2019 that has some longer-term data. Total real (inflation adjusted) revenue is up more than 4 times in 40 years. Our 1995-2018 data shows relatively small changes in average hotel prices. I suspect that there were “real” increases from 1978 – 1995 as the industry was growing quickly in response to consumer demand.

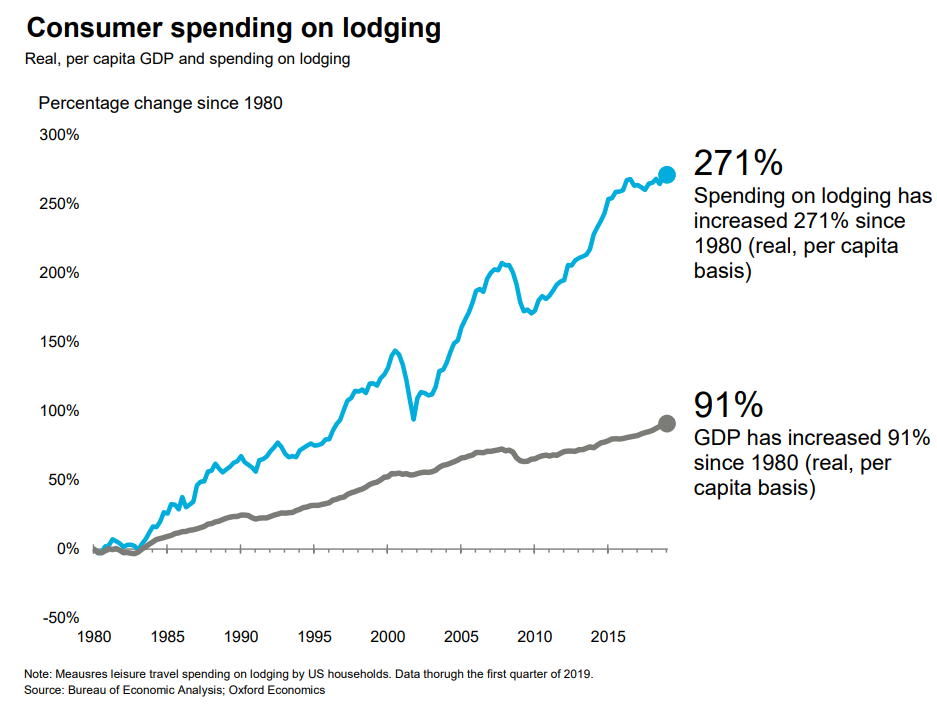

A similar measure, gross domestic product (GDP), or production value added, net of the cost of inputs, increased 3-fold in 40 years.

Consumer spending on accommodations has increased about 3 times as fast as GDP overall in the last 40 years.

Hotel purchases as a share of total consumer spending has increased by more than 80% in these 40 years.

Overall demand for hotel rooms per citizen for all uses (personal, business, government and foreign travelers) has increased by 20% across 30 years. Personal and foreign travel have grown at a faster rate.

The short-term rental market (personal vacation rentals, Airbnb) has grown from zero to 10% of the hotel room volume and appears to have years of growth ahead of it. This growth is not included in the industry summary figures.

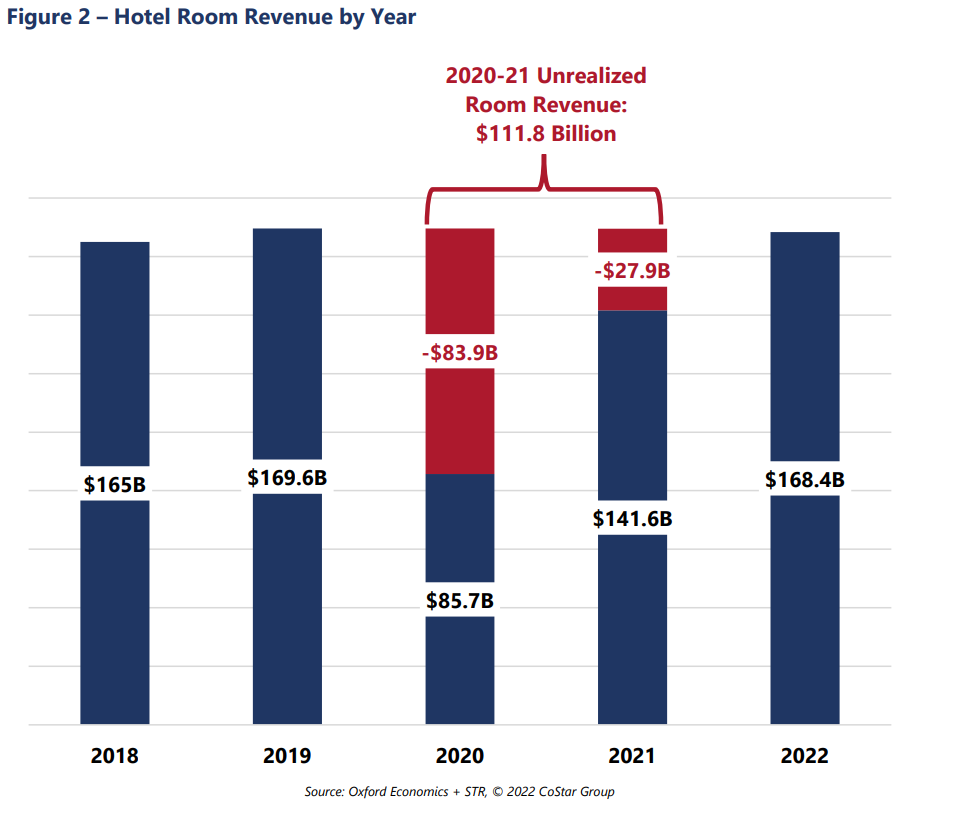

Occupancy is forecast to return to the historical average of 63% for 2022 and increase further in the following years. The industry “lost” more than $100B of revenues due to the pandemic, so analysts estimate that the industry will return to “normal” employment, prices, profitability and reserves by 2025.

Consumer access to hotels and private rentals has increased by 3 or 4 times in the last 50 years, at a faster rate in the first 25 years, and somewhat slower in the last 25 years. Hotel business models at 63% occupancy seem to justify continued capital investments in new supply. Prices have been relatively flat for 25 years. Competition between brands, pricing segments, corporations and private owners seem to be effective at providing adequate capacity and service options at competitive prices.

Democritus in 300 BCE outlined a view of the world that has strongly shaped perceptions of reality to this day. All physical things can be reduced to smaller particles (atoms) that are irreducible. Everything can be “explained” by these particles.

The progress of science since 1500 has been shaped by a principle, called Occam’s Razor, which asserts that a simpler explanation is better than a more complex explanation. This is an untestable assertion, let alone a “law”, but the general progress of “science” and the “scientific method” since that time has reinforced this bias toward simple, rational, linear, logical explanations.

The progress of modern science was accelerated by Rene Descarte’s 3-dimensional right-angle coordinate system of space. It led to the belief that all space was composed of a substance called “the ether”. Physics experiments showed that this “materialist” view of space was inaccurate.

However, the progress of science reinforced the atomist, determinist, materialist concept of the universe through the end of the 19th century (1800-1899).

Early Modern Physics was Not Atomistic, Deterministic, Materialistic.

Newton defined concepts and equations for gravity and calculus. These were true breakthroughs, but perhaps misinterpreted as purely mechanical breakthroughs.

To this day, we can describe gravity, but we have no idea how it works through space and time and matter. Gravity does not reinforce atomistic concepts, it challenges them with the notion of force at a distance, affecting those atoms.

The next major progress in physics was in describing “waves”, as they flowed between atoms. Curvilinear, not linear. Waves have a role to play in mechanics, but they are more important in electromagnetic waves.

The equivalence of electricity and magnetism was one of the first true innovative discoveries in modern physics. Counterintuitive. Not atomistic. Not easy to understand. Not understood by most.

The role of heat or thermodynamics in physics and chemistry was one that allowed atomistic views to continue into the 20th century. With a plausible description of probablistic Brownian motion, the atomistic view remained ascendant through 1900.

Research into the “nature” of the atom eventually revealed that atoms were comprised of “particles”: protons, neutrons and electrons. However, the tiny electrons did not stand still. They rotated about the core of protons and neutrons. They also rotated at specific fixed distances away from the center of electrons. Or, they “tended” to appear at these 4 distances (SPDF) away from the center, based on a very complicated probability function. Atomistic, deterministic, materialistic concepts did not apply. This did not destroy the atomistic world view, I know not why.

Einstein did not like the new “quantum theory” of the universe that was described in his time. The inherently probabilistic nature did not resonate with him, even though the physics community adopted it.

Einstein was a “determinist” at heart and devoted his later life to finding a way to reconcile the very different “forces” of gravity, electro-magnetism and atomic forces. He failed to find a simple, deterministic explanation of the universe.

All of reality is based on probability. Quantum theory of physics says that particles are connected/entangled at a distance. We don’t know which reality is real until we observe it.

The very best modern physics theory that attempts to integrate gravity, electromagnetic forces and atoms is “string theory”. It has no experimental evidence, only logic to support it. A world of “many dimensions” is far removed from an atomistic world.

Unfortunately for those who longed for a solid, formal structure, Kurt Goedel proved in 1931 that any logical system worthy of the name of mathematics could not be proven from a finite set of obvious first assumptions. Mathematicians, physicists and other scientists had long looked at classical logic and geometry as a model for their work. Goedel showed that this was impossible. Again, the world should have digested the implications of this HUGE change, but due to the complexity of the arguments it was, and has been, largely ignored.

All modern scientists conduct experiments trading off alpha and beta risks. The hypothesis may be right, but stats say it is wrong. The hypothesis may be wrong. but the stats say it is right. This is an unavoidable conflict. No deterministic system can solve this.

Atomism, determinism, materialism is an attractive view of our universe. However, we have much evidence to reject this world view. Our world is based on multiple levels of reality and probability. Most of it is “logical” and consistent, but it cannot be simply reduced to a mechanistic base.

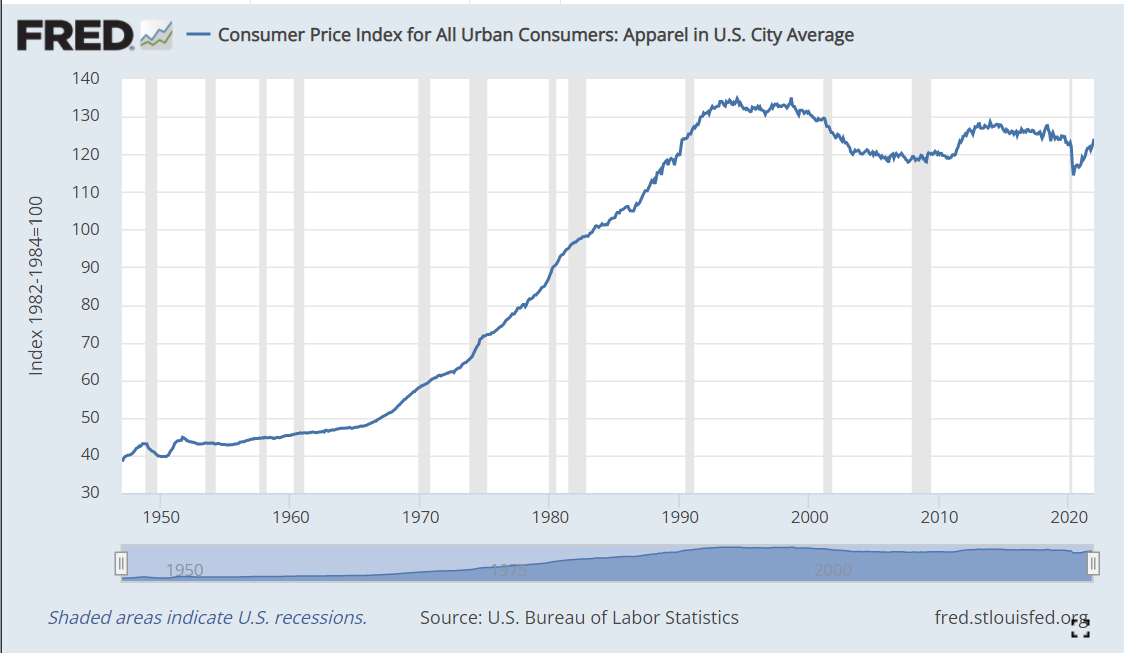

The nominal/actual average price of clothing today in the USA is 3% LOWER than it was 30 years ago, in 1991!!! Meanwhile, the overall consumer price index (CPI), has more than doubled (+106%). So, the price of clothing, relative to overall prices, has dropped by a mind-boggling 53% in the last 3 decades!

This is on top of the 37% real reduction in prices from 1970 to 1991.

From 1960 to 2021, the real reduction in clothing prices is a full 71%. More than two-thirds.

Ronald Reagan taunted Jimmy Carter with this question to voters in the 1980 debates. It helped him win.

Twelve years later, James Carville helped Democrats return from the political wilderness in 1992 with his advice to Bill Clinton that “it’s the economy, stupid”.

Politicians have used various measures, from unemployment to inflation to the “misery index” to jobs created to productivity to the stock market, to promote their success and detract from their opponents.

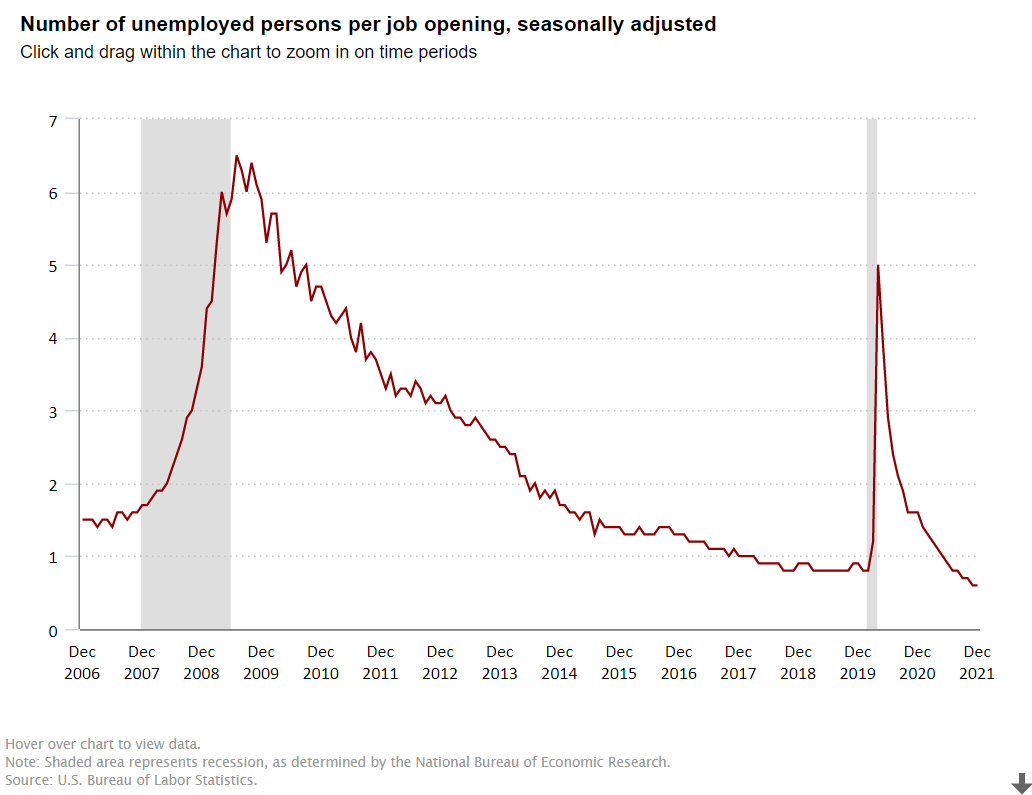

I want to focus on one measure, the ratio of the number unemployed to the number of job openings, to highlight the strength of the American economy in the last dozen years.

The Bush economy was widely criticized for its “jobless recovery” following the economically healthier Reagan and Clinton presidencies. The presidency started at close to 1 unemployed person per job opening. The recession pushed this up to 2.5x and then 3.0x. In labor market terms, this is a huge difference. At 1:1 or 1.5:1, unemployed workers expect to be re-employed quickly. At 3:1, some may enter the dark days of the “long-term unemployed”. After 3 years, the economy DID recover to 1.5:1, but it was unable to improve further. The “Great Recession” was a brutal job killer, pushing this measure of labor market tightness up four-fold, from 1.5X to more than 6X before its peak in the first half of 2010, as Obama and congress and the federal reserve bank wrestled with the situation.

Obama: Recovery and “New Territory”

Between April, 2010 and April, 2012, the economy cut this ratio in half, from 6x to 3x, a very solid performance. It took 3 years, until April, 2015, to complete the next 50% reduction, from 3x to the historically “very solid” 1.5X. The economy continued its growth for the next 2 years, but at a slower pace, reducing this ratio to 1.3X.

Trump: Even Better

The Trump economy continued to improve for the first 18 months of his term, reducing this ratio from 1.3X to 0.8X by September, 2018. This was a time of record low unemployment and economists recalculating their standard of “full employment”. While the economy continued to grow, the unemployment rate continued to decline and the stock market continued to climb, THIS measure had reached its minimum before the 2018 mid-term elections. It remained steady at the very positive level of 4 job seekers for every 5 jobs (0.8) for the next 17 months, until the pandemic disrupted everything. The ratio quickly shot up to 5X, not as high as the 6X that Obama faced, but very high. It quickly recovered to 1.4X by the end of Trump’s term. This was partly job recovery and partly fewer job seekers, but it was an amazing recovery in historic terms. Recall that 1.5X was “a good as it got” during George W. Bush’s presidency.

Biden: Even Better, Again !

In the first 6 months of the Biden presidency, this ratio dropped from 1.4X back down to the prior record level of 0.8X. Yes, by July, 2021, there were 5 jobs available for every 4 job seekers. This was as low as the ratio had previously fallen, even as the Trump economy piggybacked on the Obama economy and continued its extraordinary run. The ratio continued to fall in the next 6 months to 0.6X, an unheard-of level. 5 jobs for every 3 job seekers. It’s “no wonder” that voluntary job quits are at unprecedented levels. For, perhaps, the first time in American history, “everyone who wants to work, can find a job”. Whether you are right or left, Dem or Rep, this is “good news”. This is “great news”. Wages for the “bottom 20%” are rising in real terms. Income inequality is declining, a bit. The economy seems to be able to digest this new condition. And, the economy is not done growing, innovating, creating businesses, creating jobs, exporting, etc. About 2% of Americans are likely to be attracted back into the workforce in the next year or two, keeping the headline unemployment rate from going much below 4%, but pushing US real GDP growth to 4% in 2022 and close to 4% in 2023.

Summary

The “Great Recession” and the “once in a century pandemic” have been unable to disrupt the ongoing progress of the American economy and labor market. As a nation, IMHO, we have cultural and political challenges, but we “aught” to appreciate the power of the American economy to move forward.

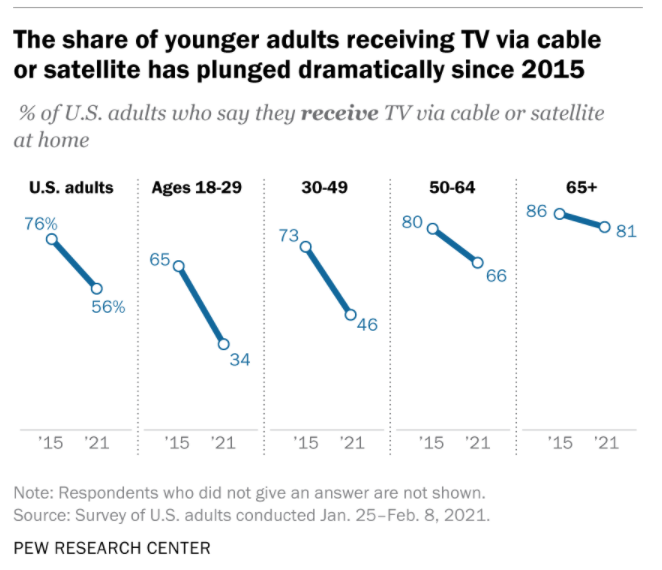

Cable TV subscribers and networks grew rapidly through the 1980’s and 1990’s reaching near universal availability. US subscribers plateaued from 2009-2014 at 100 million before rapidly declining to 74million in 2021. As the first graph shows, much of the decline has been a substitution of internet for cable access to media content. This is “good news” because everyone that wants it has access, but a new, better product has started to rapidly displace this 50 year-old technology.

Ownership of a home desktop or laptop computer also remains near universal, at 77% in 2021. The ownership of tablet computers has risen from 14% in 2012 to a majority of homes (53%) in 2021.

Broadband internet access has rapidly grown from 1% of homes in 2000 to 58% in 2008 to 77% in 2021. The retired generation (65+) lags behind at 64% connectivity. Black (71%) and Hispanic (65%) homes are below the average. Rural residents are also less connected (72%).

Internet Users

Pew Research also reports that the percentage of individuals that are internet users has nearly doubled from 52% in 2000 to (near universal) 93% in 2021. About three-fourths of older individuals (65+) are “surfing the web”. 97% of others are connected. There is no major difference between racial categories. Rural citizens are little less engaged (90%).

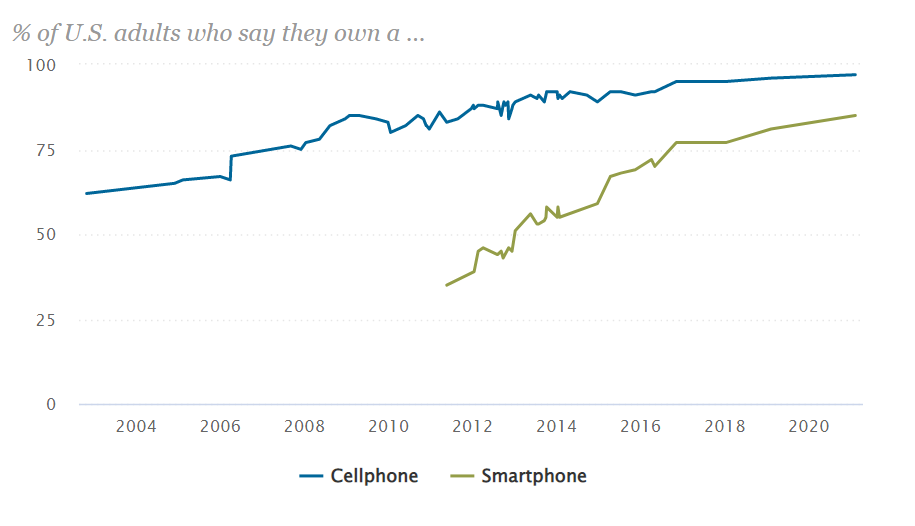

Mobile phone ownership has grown from 62% in 2002 to 97% today. Seniors (65+) have slightly lower ownership rates (92%). Racial groups have the same ownership. Rural residents have slightly lower ownership rates (94%).

Smart phone ownership has grown rapidly from 35% in 2011 to 77% in 2016 to 85% in 2021. Ownership rates vary by age: 18-49 (95%), 50-64 (83%) and 65+ (61%). There is no racial ownership gap. Rural residents have an 80% ownership rate.

Summary

Although we saw news coverage during the pandemic which highlighted the imperfect access to electronic devices and network required for effective on-line learning, the US is approaching a state where nearly everyone has access. Cable TV access is now post-peak. TV network access is increasingly through the internet. Broadband access is the weakest measure at 77% ownership. Cell phone ownership is universal and smart phone ownership will reach that level before the end of the decade.

Postscript: Economic Impact = 10% of GDP

Industry associations, journalists and consultants wrestle with each other to capture and communicate the economic value added by personal computers, smart phones and the internet. In rough terms, about 10% of GDP is due to the direct and indirect value of these technologies that did not exist in any economically material amount in 1980, just 40 years ago. Good news? No, GREAT NEWS.

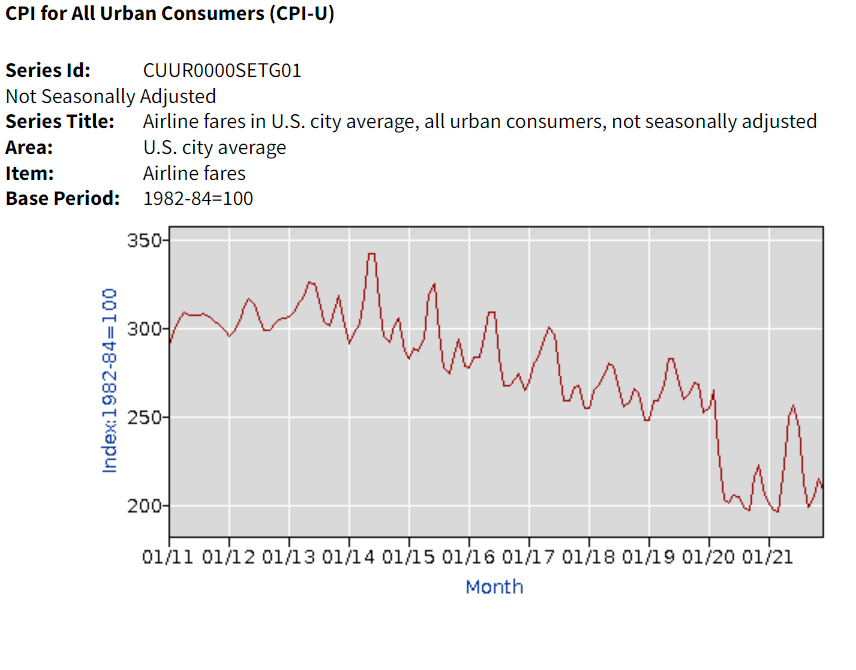

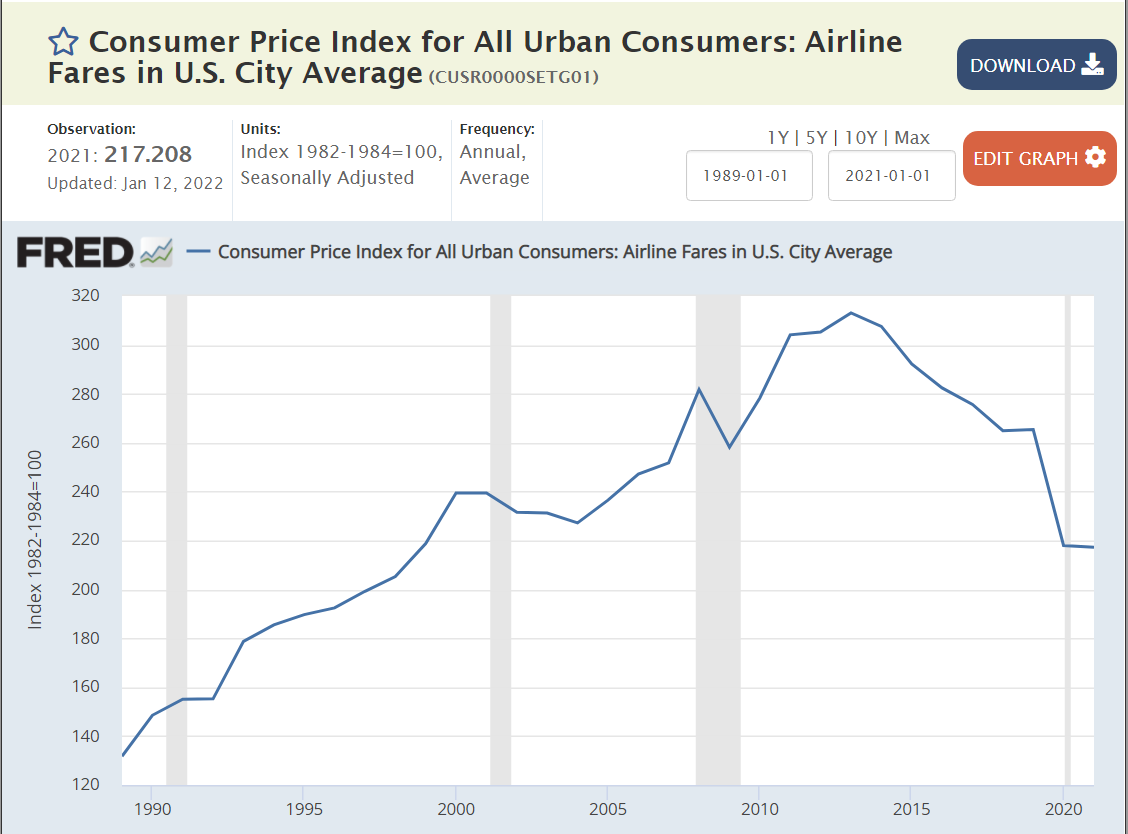

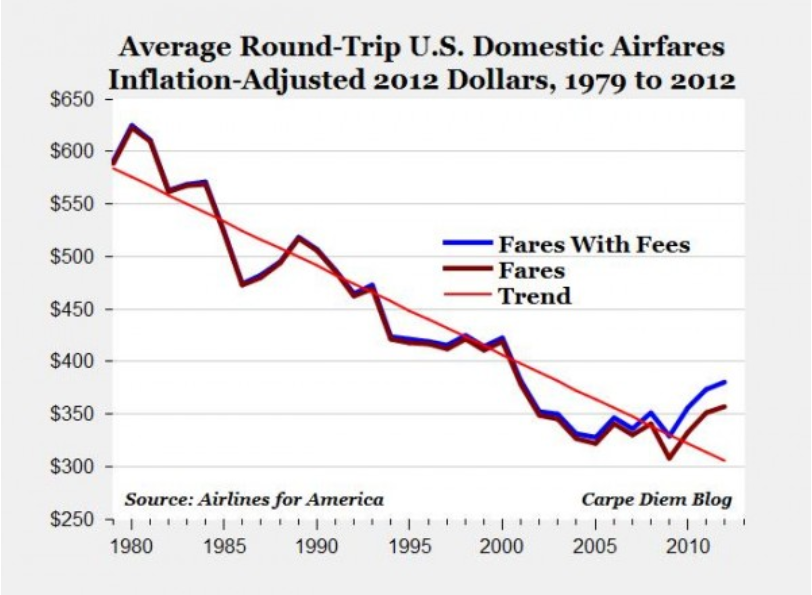

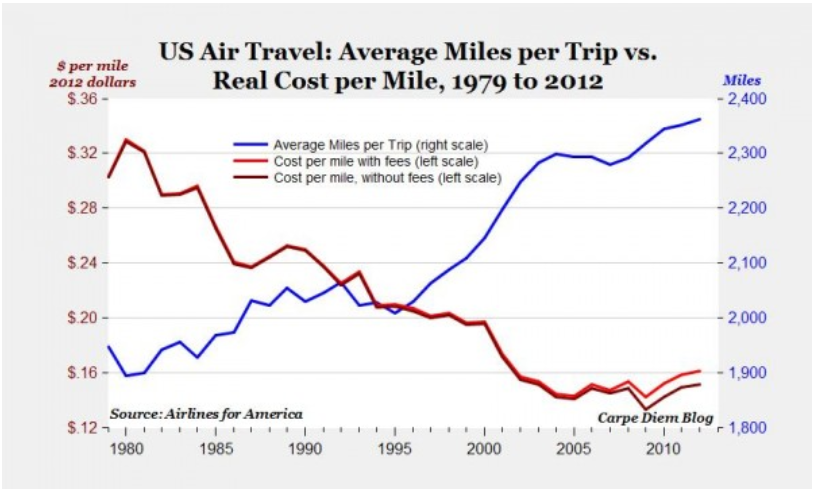

This article combines data from 4 sources with slightly different data. Airfares were flat at the end of the 20th century, but then dropped by 19% by 2004. They remained flat, in real terms, through 2009. Airlines pushed through 8% higher prices in 2010-11 and maintained real fares at the same level through 2014. After 19 years, real airfares were 14% lower than in 1995.

Fares then dropped year after year through 2019, reaching 26% below the 1995 baseline. They have fallen further in the pandemic years to 43% below the level of 25 years ago.

Bureau of Labor Statistics / CPI

The Bureau of Labor Statistics compiles a consumer price index for air travel as part of the overall CPI. It compiles average prices and tries to adjust for changes in the quality of the product.

Real airfares declined consistently throughout the period, but no data source is fully compatible with the 4 summarized above. It appears that the real cost of flying declined by about one-third between 1979 and 1995 as the airline industry was deregulated.

At the height of the cold war, in the year on my birth (1956), Soviet First Secretary Nikita Khrushchev warned the US that “we will bury you”. Agriculture was still a very large share of the USSR and US economies. He couldn’t have been more wrong.

US statisticians have long separated the farm and nonfarm economies. A “census of agriculture” is conducted every 5 years to complement other economic statistics collected. The USDA Economic Research Service (ERS) does a great job of compiling statistics for the narrow (farming), moderate (fishing, timber) and broad (ag based production) agriculture industries.

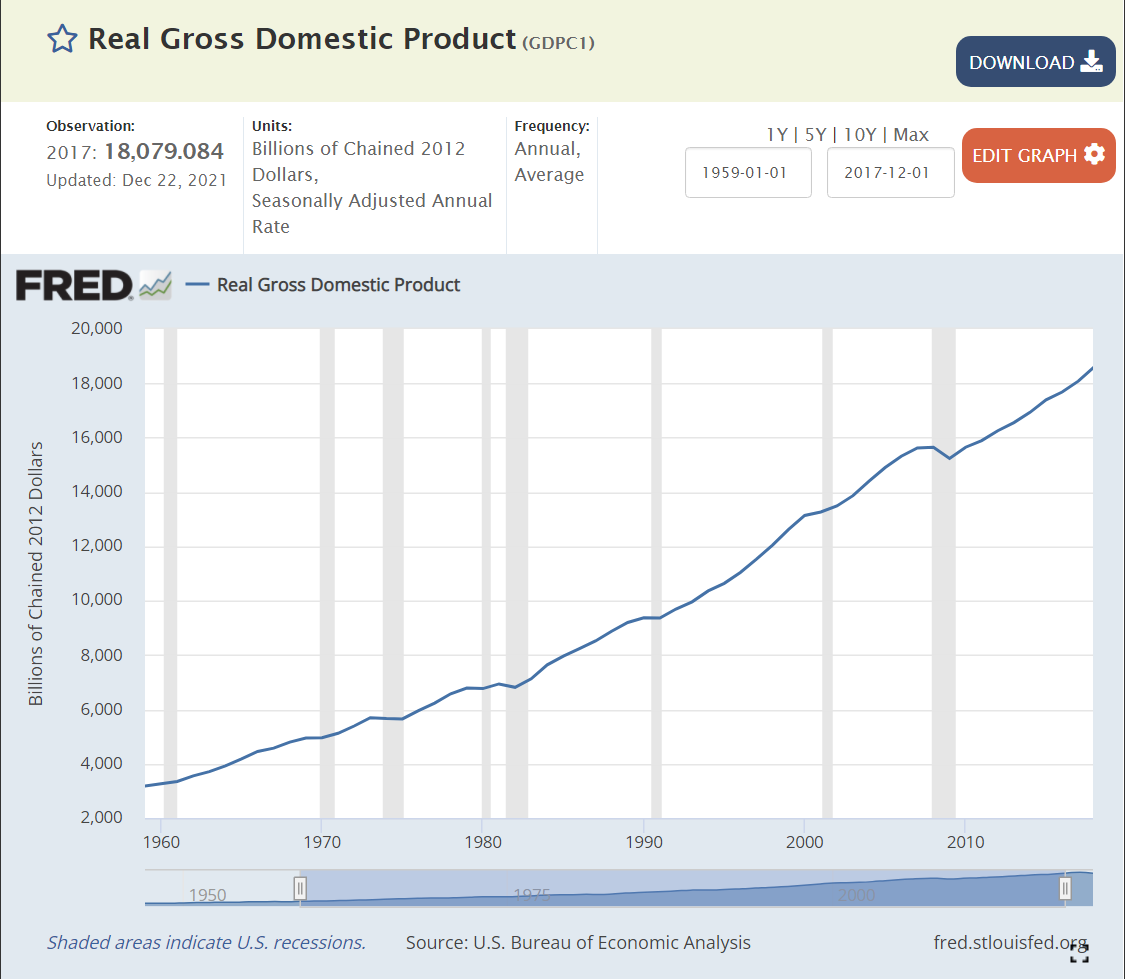

I’ve chosen to examine the near 60-year period from 1959-2017 covered by the censuses of agriculture. During this time, Real (inflation adjusted) US Gross Domestic Product (GDP), the value of all goods and services produced, increased from $3 to $18 trillion dollars, a near 6-fold increase, or 3% annually, year after year after year.

We don’t have an economic series that tracks wage and salary income back before 1979, but real disposable income per capita exists for this whole time period. This indicator or labor costs increased 3.4 times, from $12,600 to $42,900, or 2.1% annually. Given the strong growth of the US economy and its many new opportunities AND the increase in labor costs facing the oldest industry, one might have agreed with the Soviet premier back in 1956, at least regarding US agriculture. But, that prediction was wrong.

Index of Unit Outputs

The US agricultural economy grew to more than 2.5 times its 1959 base by 2017. It grew by 75% in the first 30 years and an additional 50% on top of that new base. The consistent pattern of growth is striking.

Real Market Value Produced

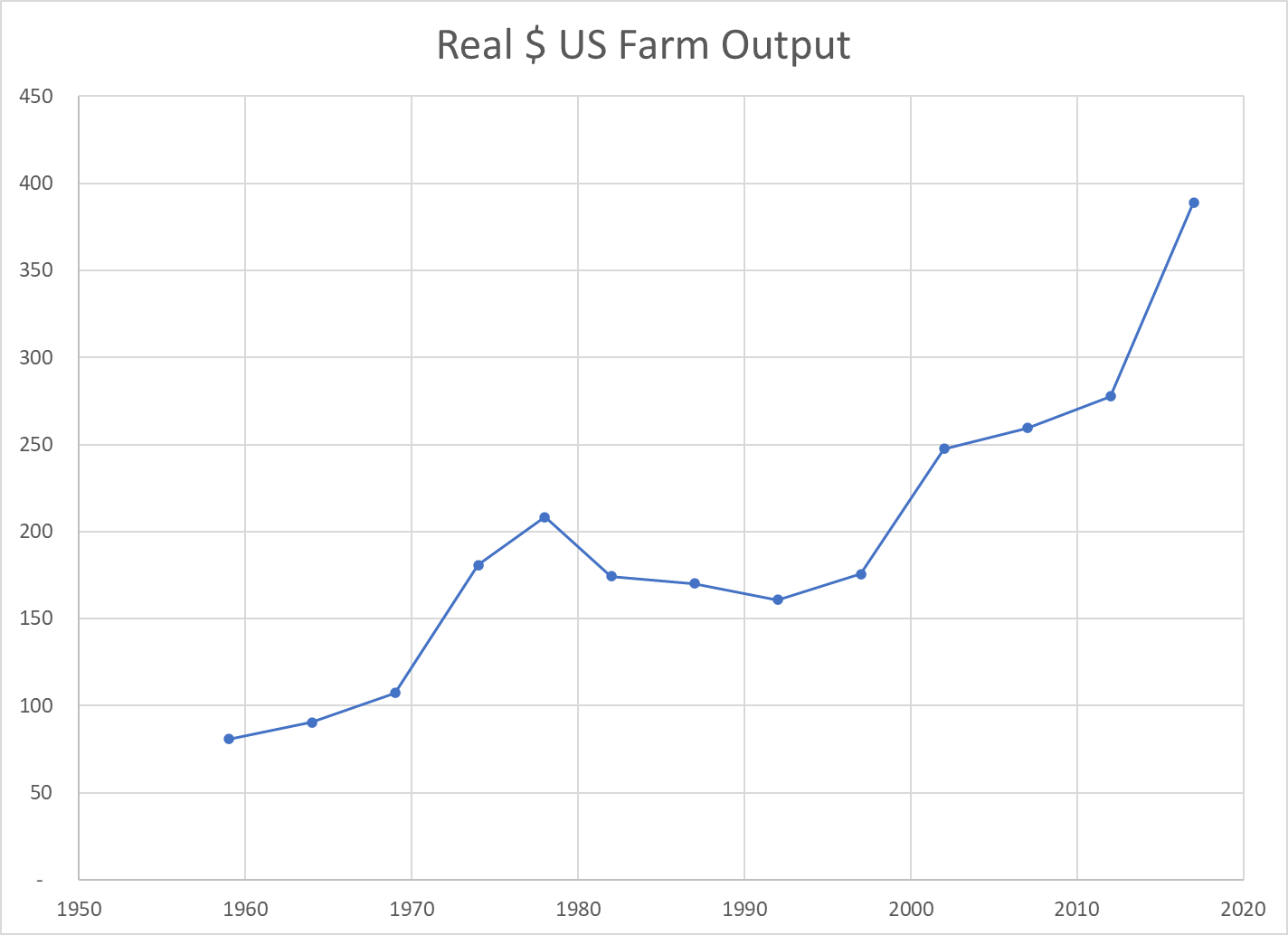

The Ag economy grew (based on variable market prices) 5-fold from $80B to $390B during these six decades, increasing by 110% in the first 30 years and a compounded 130% in the most recent 30 years.

Land Input (Acres)

The amount of land dedicated to production agriculture has decreased by 20% during our period of focus, from 1.1B to 0.9B. The decline was faster in the first 30 years (14%) than the second 30 years (7%). Despite this reduced demand for agricultural land, the value of such land has increased in real terms as its productivity has grown.

Labor Inputs FTE

The full-time equivalent labor force in the ag industry, as best as the USDA can measure it, dropped by nearly two-thirds in our six decades, from 2 million to about 700,000. It fell more rapidly in the first 30 years (50%), but a solid 25% in the most recent 30 years.

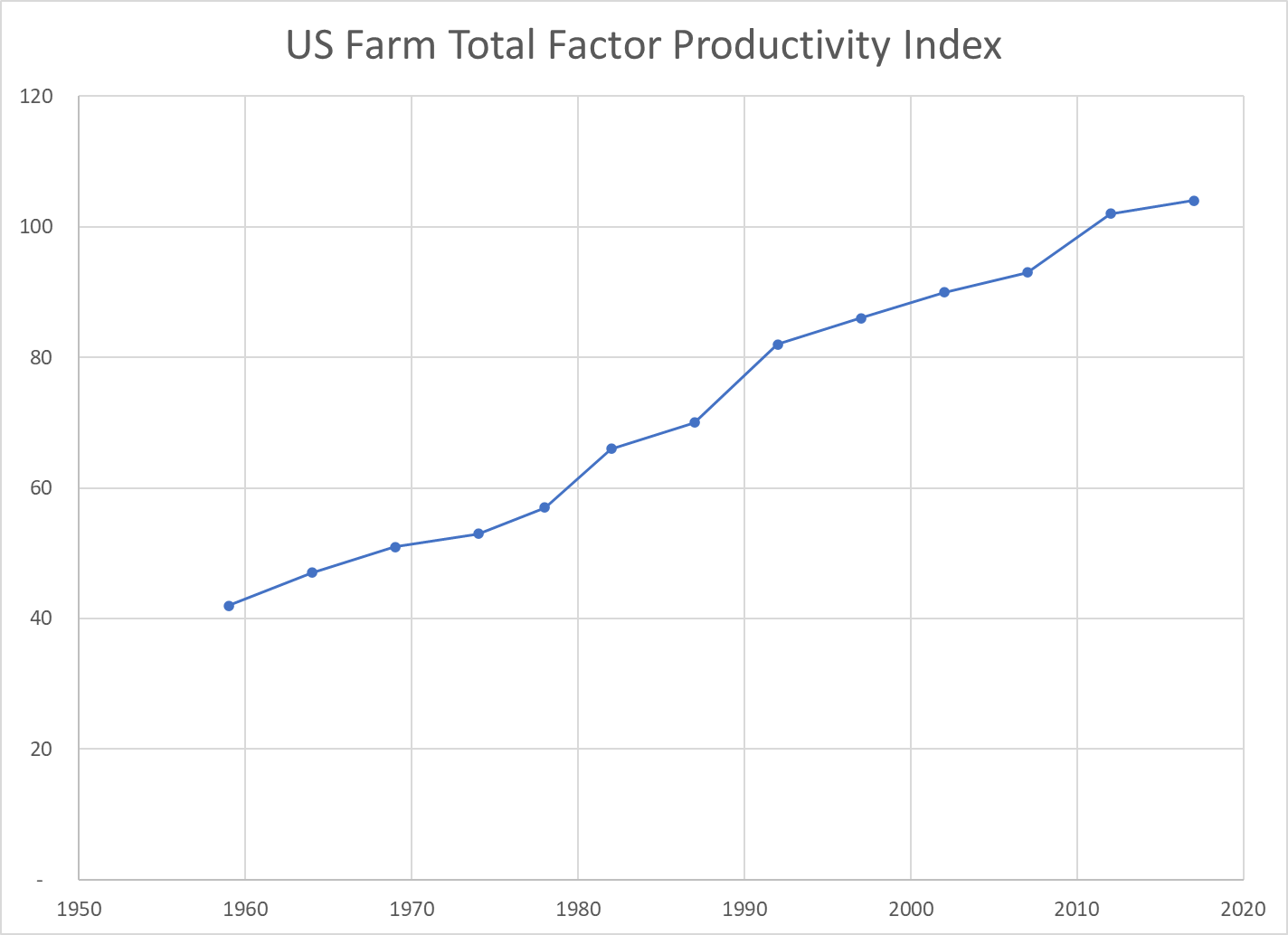

Total Factor Productivity

Economists try to measure land, labor and capital as inputs to the agricultural production process. As noted above, land and labor have declined. Capital – equipment, improvements, patents, inventory, etc. has increased. Overall, the total inputs have remained roughly flat for 60 years. Hence, almost ALL of the increased unit output is due to increases in productivity. Better crops, better labor skills, better processes, better methods, better irrigation, better crop rotation and selection, etc. Economists call this “total factor productivity”. After accounting for measurable increased inputs, the remaining improvement is called “productivity”.

The oldest industry in the world, increased its productivity in the US by 150% in these six decades; by two-thirds in the first 30 years and by one-half on the higher base in the second 30 years.

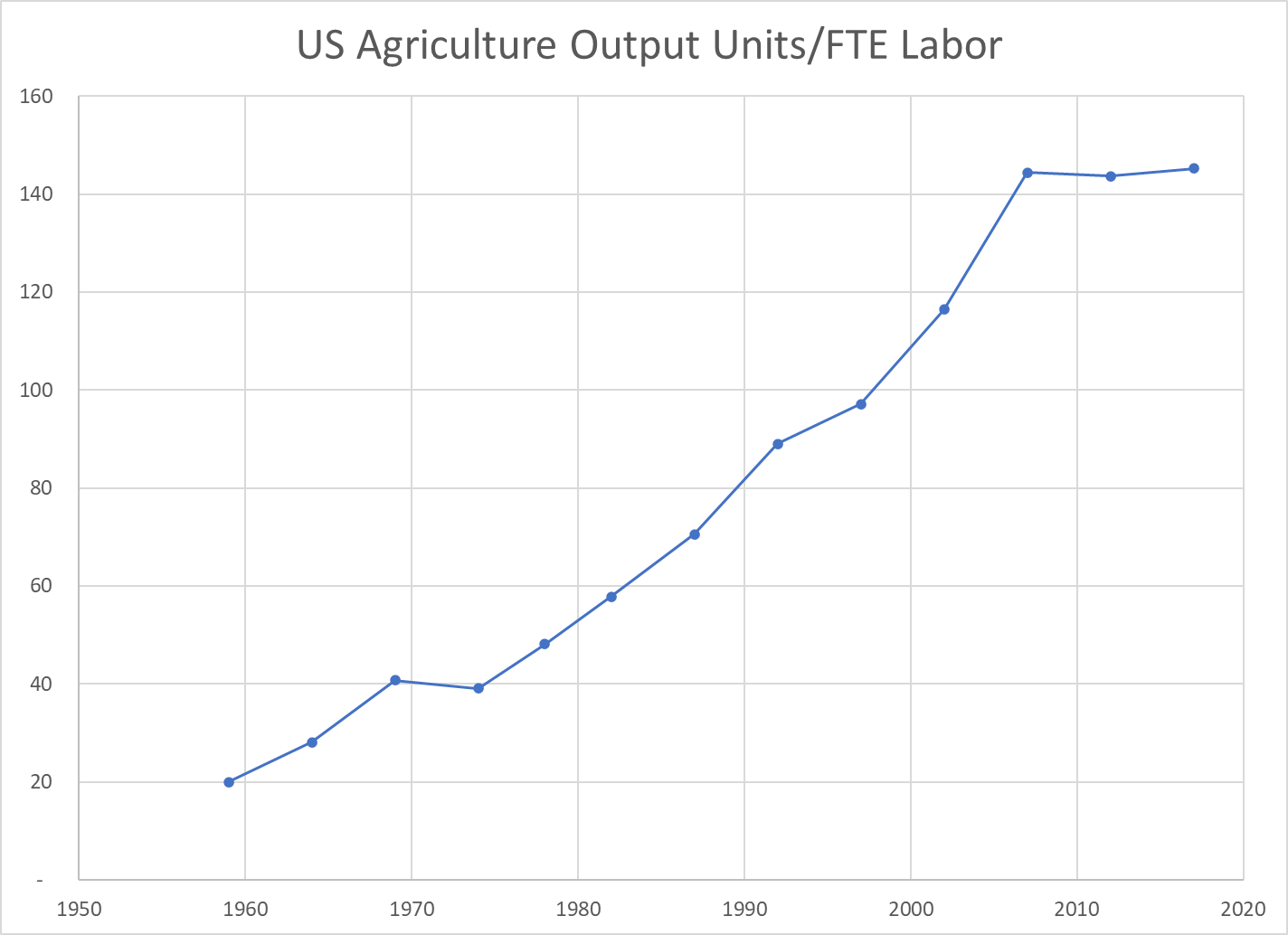

Output per Labor Unit (Labor Productivity)

The strong increase in production combined with the two-thirds reduction in FTE labor required resulted in a 7-fold measure of improved labor productivity. The land input was down by 20% and the capital input increased significantly, but in simple terms, each hour of labor in 2017 delivered 7 times as much output as the labor in 1959. The increase was 2.5x in the first 30 years and a solid 2x in the more recent 30 years.

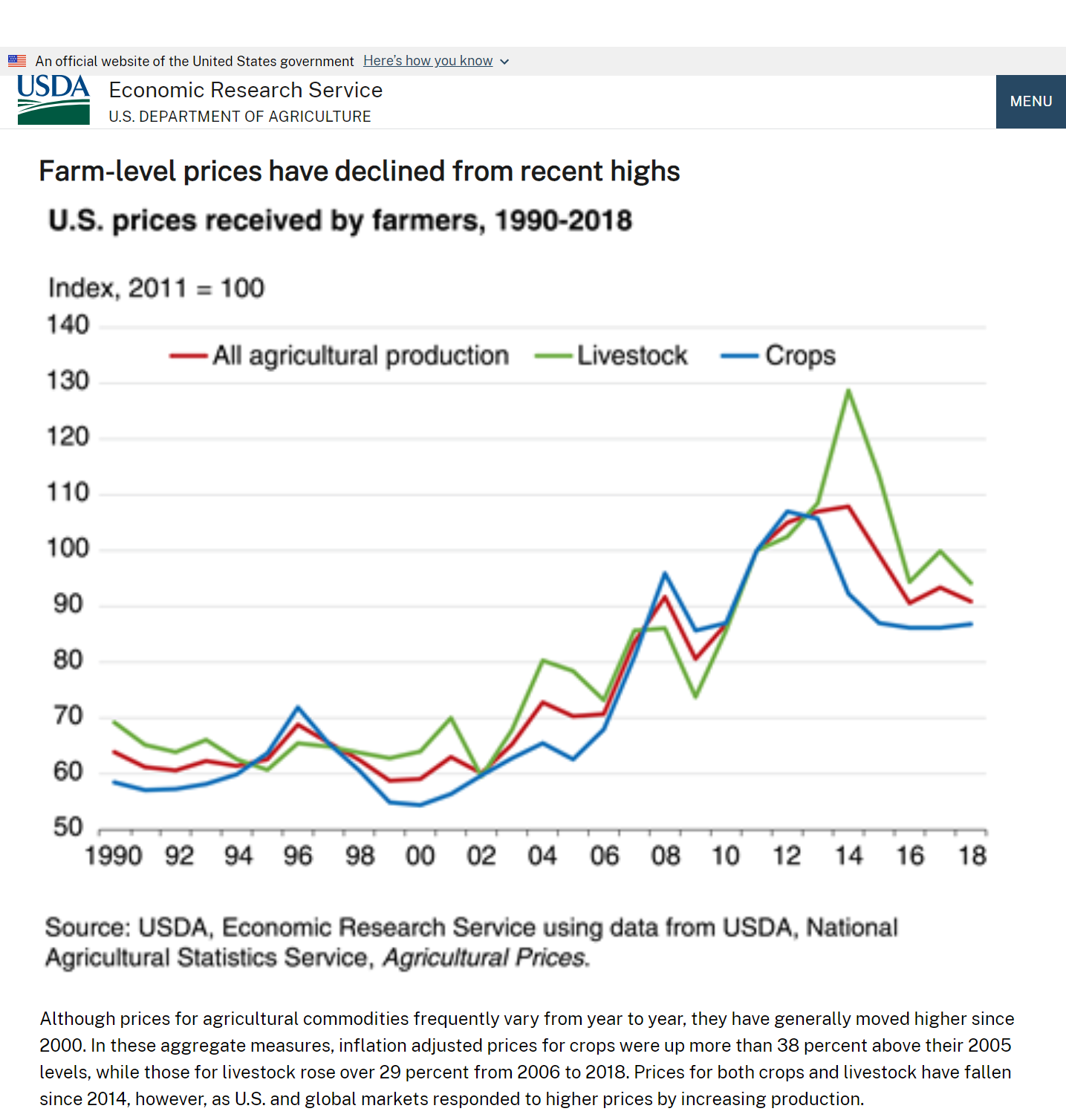

US Agriculture Output Price Index

The index of agricultural industry output prices has increased by 3-4x versus 8x for the consumer price index or GDP price index.

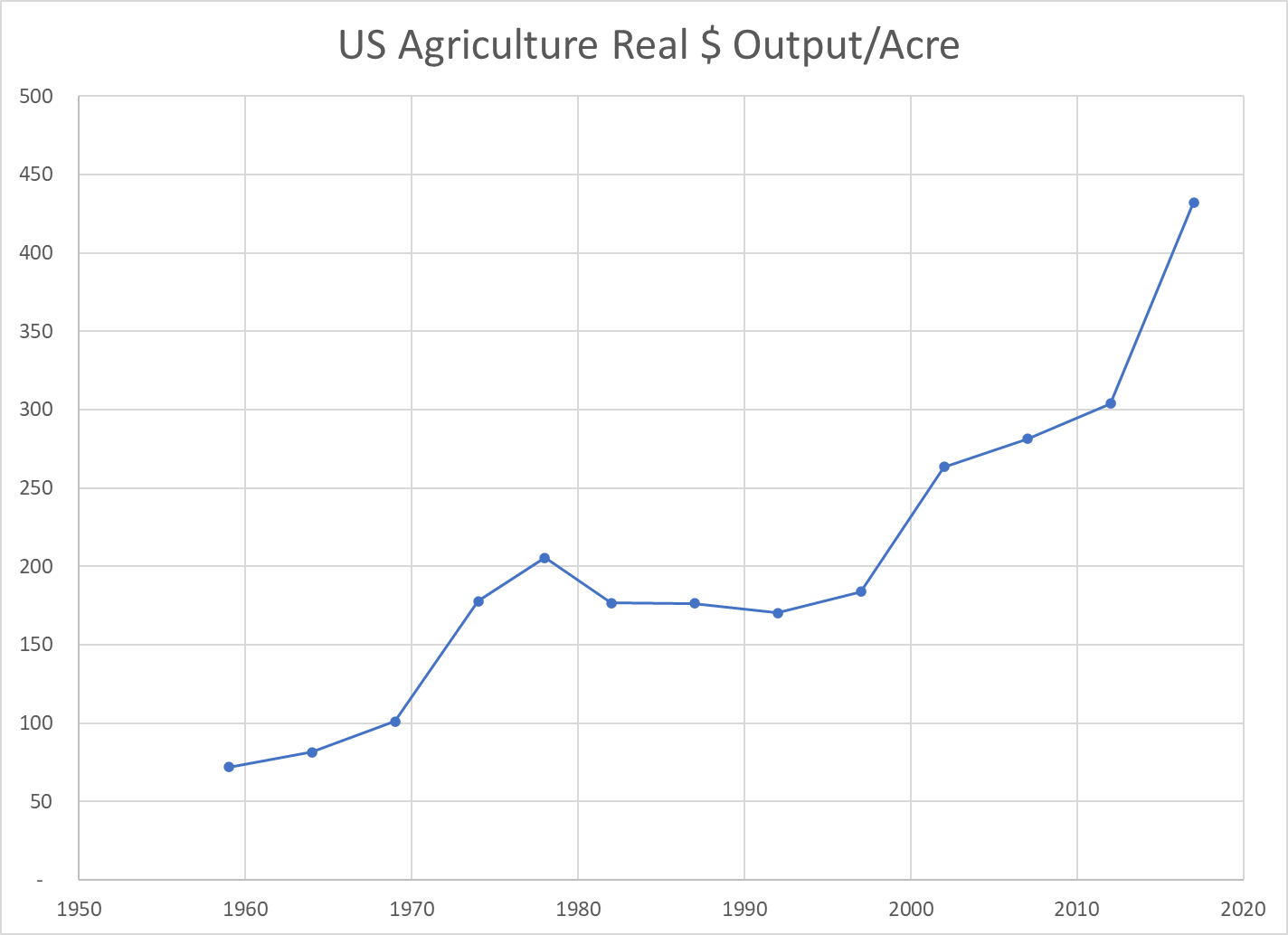

Real Market Value Produced Per Acre

The real market value of ag goods produced increased 5-fold. The land acres required declined by 20%. The output value per acre figure improved 6-fold. Again, labor inputs declined and capital inputs increased. This measure of land productivity improved by 150% in both of the first and second 30-year periods.

Real Agricultural Exports

Real ag exports increased 4-fold in these 6 decades, doubling in the first and second 30-year periods.

Summary

Less land and labor. More capital (equipment). Much better R&D and processes. Total factor productivity up by 150% across 6 decades, an average of 1.6% year after year after year.

The US ag industry faces many challenges today. Environmental issues and climate change. Water shortages. Lower public and private R&D investment. Brain drain. Political polarization. Concentration of key property rights. Low wage labor access. Changing trade rules. Nonetheless, the last 60 years indicates that this industry is capable of delivering further increases in production and productivity for the next 60 years.