Brief Analysis Below Each Chart:

Since July, overall inflation is immaterial (1%), about 2% on an annual basis.

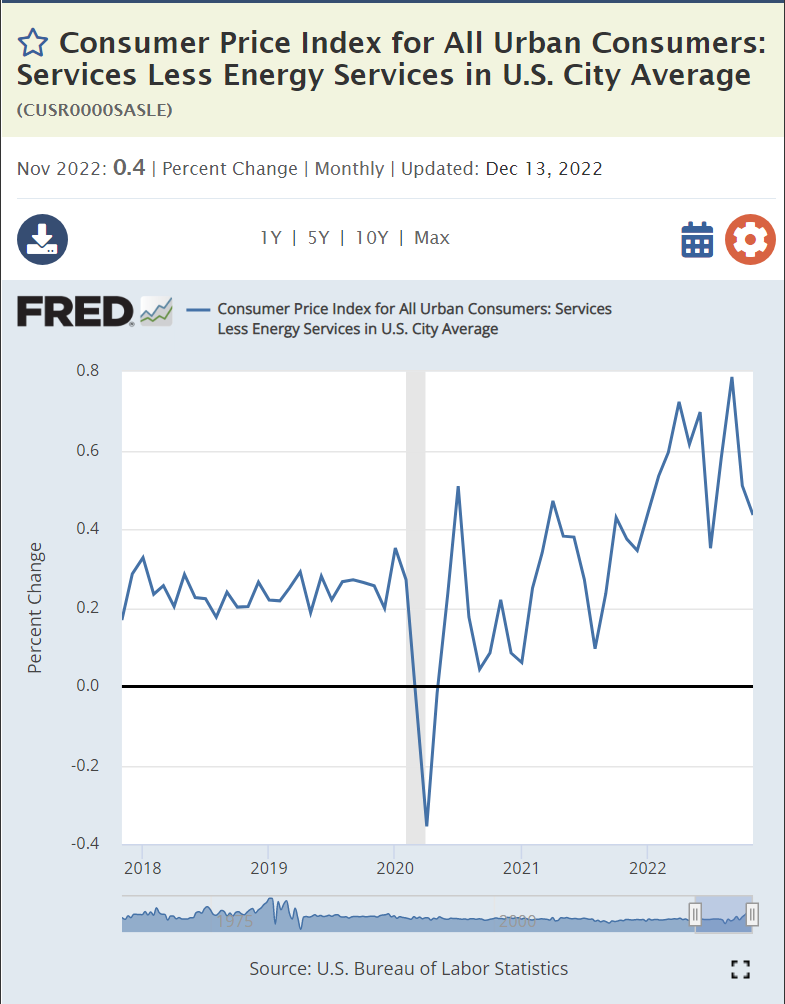

The Services sector is the most concerning, with annual inflation still running near 6%. The recovery from the pandemic started with the goods sector and then slowly rotated into the services sector as “in person” services re-emerged.

Since March, 2022 durable goods have reassumed their long-term price Deflation.

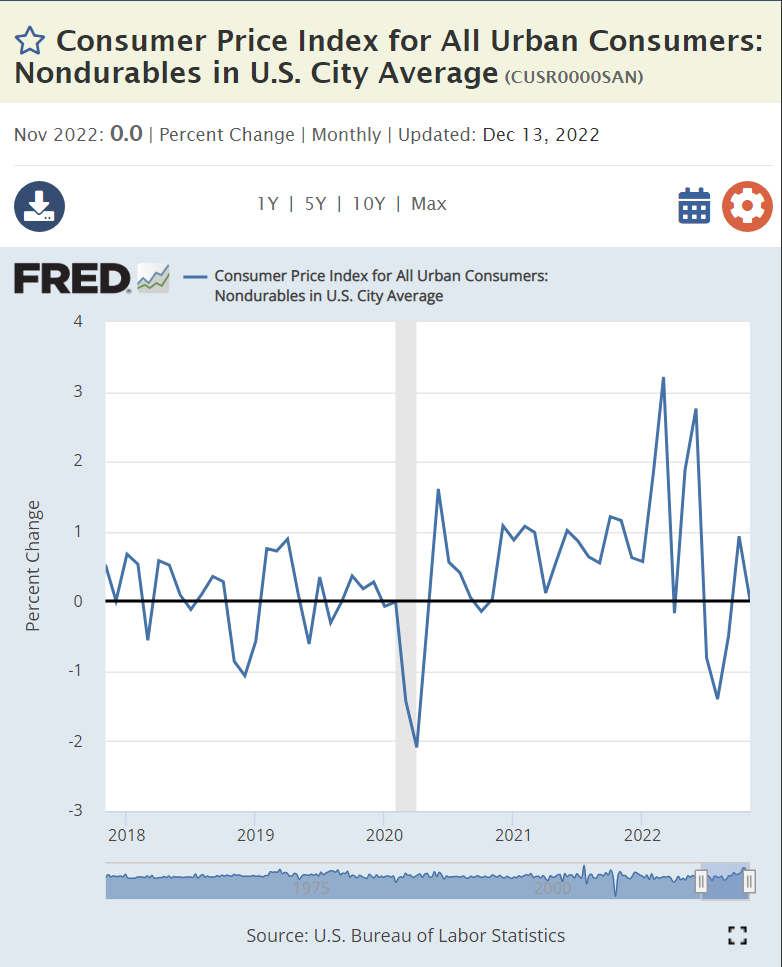

Nondurable goods are back to 0% inflation.

Energy prices are clearly falling now.

Gas prices have retreated back to $3 per gallon as quickly as they increased.

Food prices have fallen but remain abnormally high, growing at 6% annually. Global pressures may keep this category above normal during 2023.

Wage-push inflation remains a thing of the past. Real wages remain flat.

Strong economies with solid currencies are able to import cheaper goods and reduce domestic inflation.

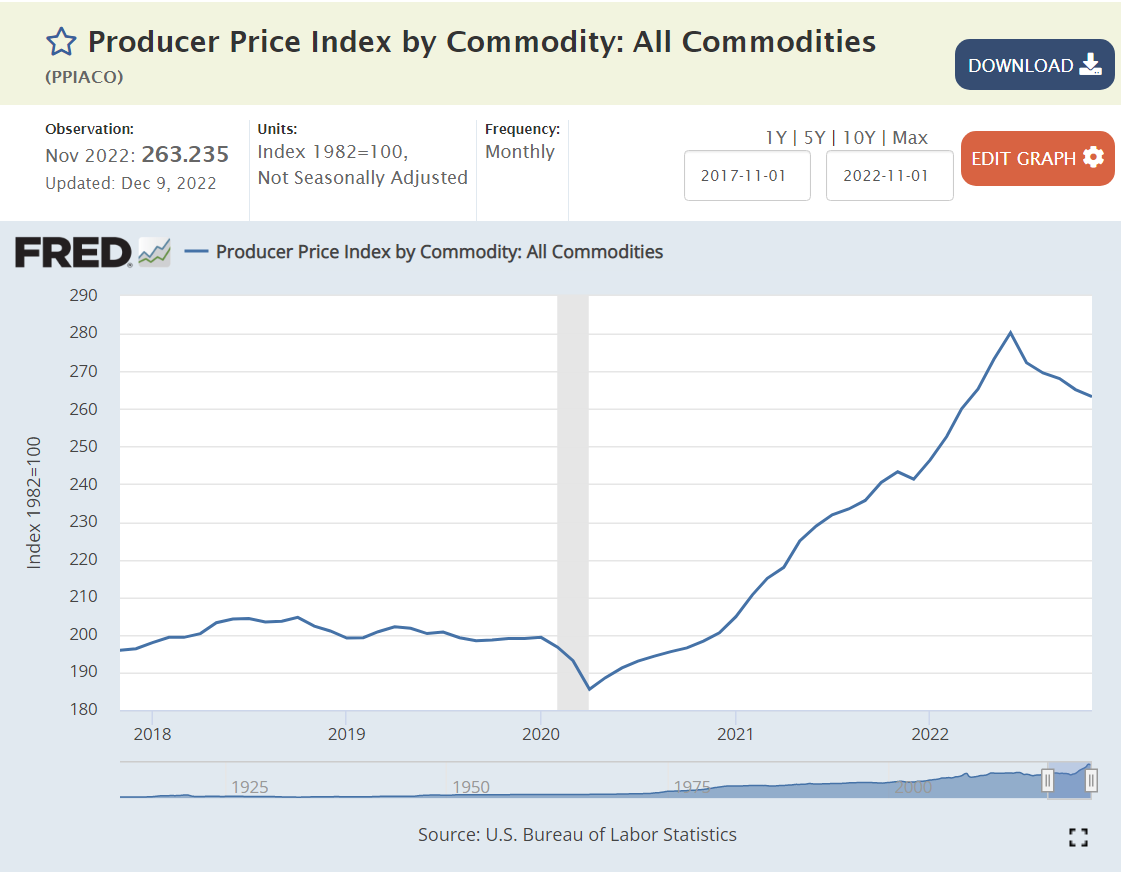

Producer prices have fallen by 6% from their peak.

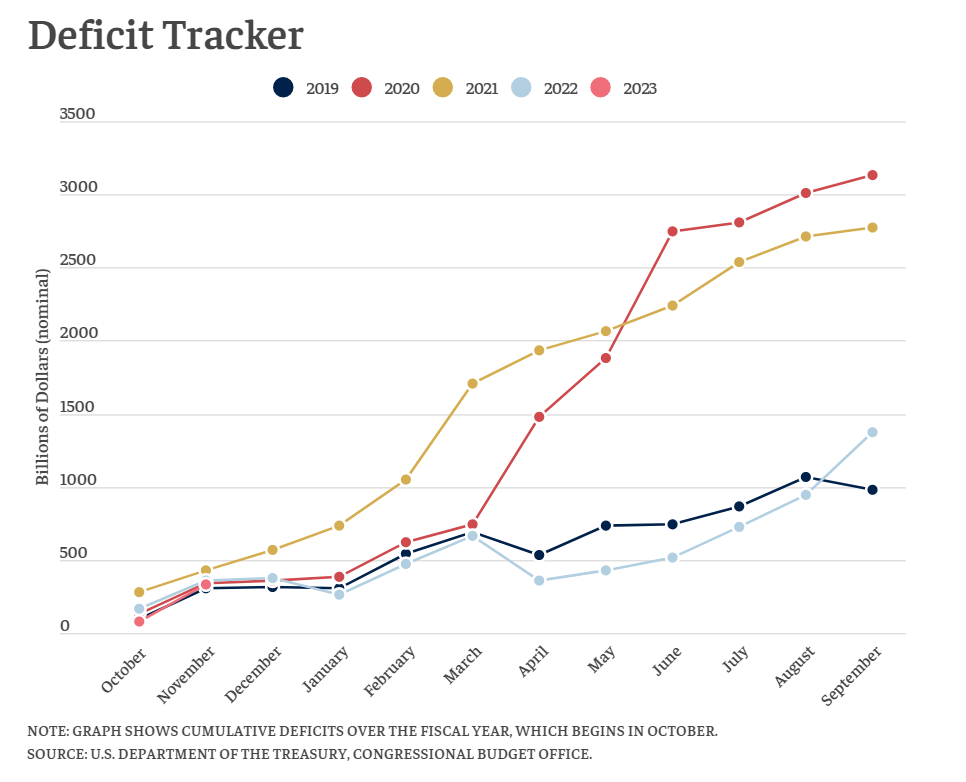

US fiscal policy for 2022 was at the same expansionary level as pre-pandemic 2019. I think it was a little too expansionary, but this level of deficit did not significantly drive the increased inflation in 2022. The budget deficit for fiscal year ending September, 2023 is expected to increase by a small amount, even though the latest official CBO forecast showed a smaller deficit.

https://www.cbo.gov/publication/58470

Monetary policy was very loose in 2020, attempting to offset the many threats to the economy. It has since been closer to “neutral”. There is no solid historical or theoretical basis to carefully predict the effect of this huge increase in the money supply two and a half years later.

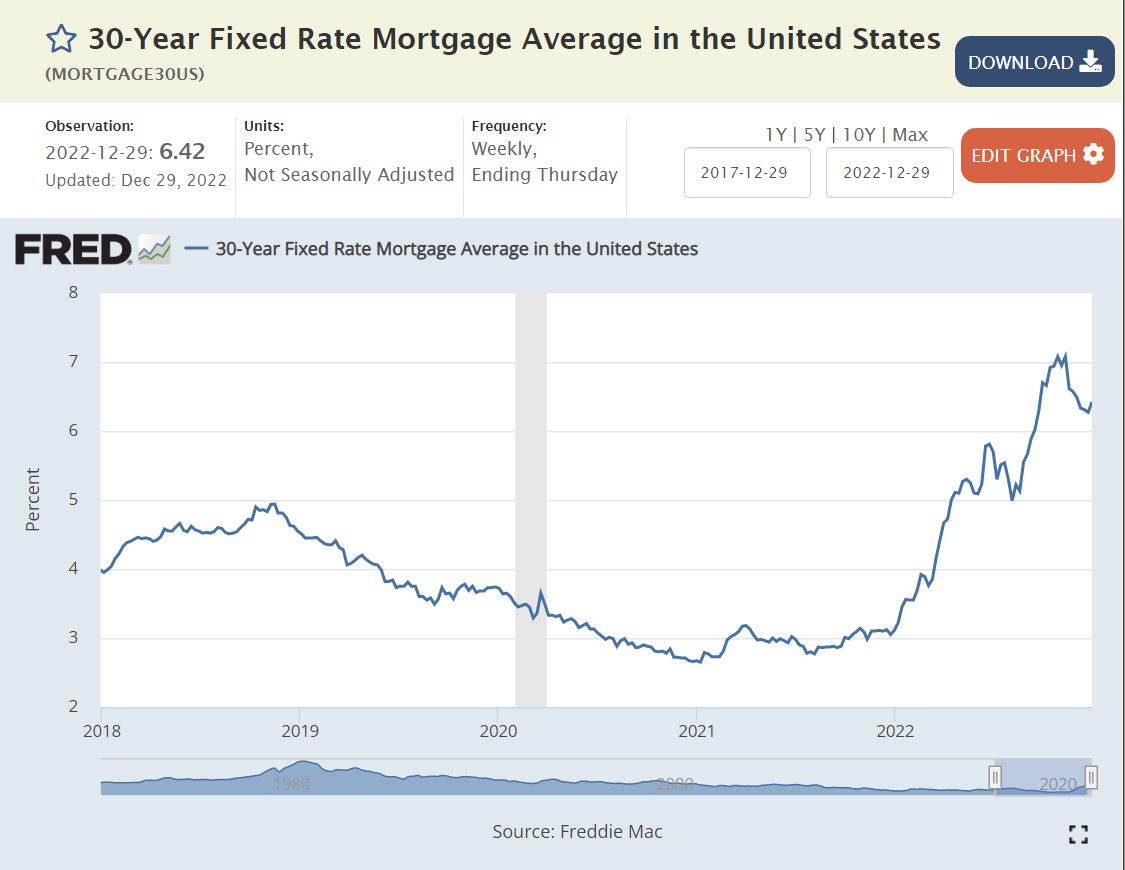

The Federal Reserve Bank has increased interest rates and the housing, stocks, bonds, construction and commercial investment markets have been impacted, slowing aggregate demand for assets, goods and services.

The stock of “excess savings” which supported the rapid recovery from the pandemic peaked in early 2021 at $2.25T. It had fallen by 20% to $1.75B by the 3rd quarter of 2022 and continues to fall, reducing aggregate demand.

Summary

The scariest inflation scenarios are no longer plausible. Durable goods, nondurable goods, producer and energy prices are falling. Food and services prices remain elevated at 6% but are not in double digits and are not increasing. Real wages spiked briefly during the heart of the pandemic but quickly returned to pre-pandemic levels where they have remained.

The federal budget deficit in 2022 was the same as in 2019 when inflation remained low. Even with a slowing economy, the forecast 2023 budget deficit remains about the same as in 2022, not adding materially to excess demand. Monetary policy in 2022 has consistently been tighter and tighter, with the Federal Reserve chairman promising to “do whatever it takes” and highlighting the much greater negative consequences of inflation that does not return to the target level. Weakened fiscal and monetary policy should help to further reduce any remaining supply chain constraints in the global economy. The housing and capital investment sectors are declining. The impacts of changed monetary and fiscal policies are seen 6-24 months later.

Double-digit and accelerating inflation are no longer credible. Deflation is the rule in a large part of the US economy. Monetary and fiscal policies are tightening. Overall inflation is falling. The economy has already slowed, so we may even be entering a period of self-reinforcing lower rates of inflation.

So do you think we will have a much slower economy with rates being high? Does this Federal Reserve indicate it would lower rates soon to stimulate?

We’re going to have zero growth for 2023 and return to 2% growth for 2024, methinks. We may have an official recession of two slightly negative quarters in 2023, but when I look in the retail shops and restaurants, people seem to still be spending. I think the Fed will increase rates by 0.5% this quarter and maybe 0.25% in March/April and then pause. I agree with the chairman that the Fed has to break the inflationary expectations. That means they have to “overdo it” a bit. I don’t think they will cut rates before 4Q, 2023. It looks like there is so much underlying consumer demand that the economy will recover on its own starting late in 2023 even without interest rate decreases. The 2 open positions for every unemployed worker is the most positive sign. It says that “money making” businesses see many, many profitable opportunities to sell more stuff and serve more “willing customers”. The extended below 4% unemployment from 2017-19 (without significant inflation) may be the new normal in a service economy. Good news, indeed.

Happy New Year Tom! Thank you for compiling all this inflation-related information in one place. Appreciate your analysis and insights! Definitely potentially encouraging trends.

[…] Create Many Jobs (!!!) Good News: The US Economy is Still Firing on All 12 Cylinders Inflation is Slowing Recession!?, Recession!?, I Can’t Find Any Recession! Has Inflation “Turned […]

[…] Inflation is Slowing […]