Trump focuses only on win/lose. If the US earns $1 trillion from trade and the rest of the world (ROW) earns $1.2 trillion, he sees this as a $200 billion loss. The ROW is winning, taking advantage of the USA and its unenlightened deal makers. If the US earns $500 billion from trade and the ROW earns only $400 billion then we are winning by $100 billion. Trump sees the second scenario as far superior to the first. Relative winnings (win/lose) are the bottom line rather than actual winnings (win/win). This is a fundamental flaw.

The Wrong Measure

Trump only sees costs; he doesn’t consider benefits. Net benefits, benefits minus costs is the right measure.

The Wrong Timeframe

Trump only looks at the short-run. He ignores the long-run. He believes that he can always renegotiate any situation.

International Relations is Complicated

Trump only sees dollar signs. The trade balance can be measured. It is positive or negative. The cost of defense can be measured. Either we pay or others pay. We trade goods and services. Defense/security benefits matter. We care about immigration, crime, taxes, personal security, climate, health, economic development, investments, rule of law, intellectual property, labor, the environment, etc. Other countries care about all of these dimensions. We must too.

International Relations is Irrational

Citizens have an irrational commitment to their nations. They are willing to die for them. Nations have sovereignty. Each has certain minimal rights. Politicians respond to these irrational beliefs. Ignoring this reality is irrational, even though it is very frustrating.

Alliances are Cheaper than Empires

The US learned from European, Japanese and American experiences. Empires are very costly to establish and maintain. Nations can be enticed into becoming reliable allies at a fraction of the cost. They are rationally willing to evaluate costs and benefits, risks and rewards, short-term and long-term, labor and capital, sovereignty and influence, security and opportunity. Trump is right to negotiate, but wrong to discount this basic approach.

Global Agencies are Cheaper than Individual Deals

The US has greatly benefited from the post-1945 system of global governance, finance, economic development, health and trade. Global deals designed by the global leaders provide a framework for low-cost transactions. Trump believes that the strongest nations can extract even more net value through individual deals. Too many countries. Too much complexity to negotiate all of these topics effectively.

Single Deal or Repeated Deals?

Trump comes from the real estate world where each deal is “one off”. International relations and trade are repeated deals. The optimal strategy is different when the “tit for tat” strategy can be used. Firms and nations will punish any bully, even at a significant cost to themselves. The strongest players must consider the weaker players’ strategies. When firms or nations find that they cannot trust someone the total costs go up significantly.

Playing Chicken

There are many strategies in the game of chicken. The strongest player does not automatically win. Bluffing matters. Posturing matters. Resources matter. The ability to endure losses and pain matter. Allies matter. Insurance matters. Flexible resources matter. Capacity matters. Creativity matters. Credibility matters. Non-negotiable factors matter. Trump seems to confuse simple economic might with certain winning.

Comparative Advantage

Trump does not understand David Ricardo’s theory of comparative advantage from 200 years ago. You can be better than someone else in everything, at least in theory. You cannot have a comparative advantage in every production process. Between any two individuals, firms, states or nations, there will be differences in relative productivity. This is the basis for trade and specialization. The U.S. cannot be better in every industry. We can be relatively better in many industries, but not in all. As our incomes and standard of living increase, we will be relatively less competitive in those activities that can use lower cost labor. This is an unavoidable fact. We can choose to subsidize low skilled manufacturing employment, but we are fighting against very strong market forces.

Dealmaking Strategy

Trump focuses on simple short-term one-time win/lose. The best negotiators know that the greatest value comes from “growing the pie” in the long-run (win/win). They don’t assume a fixed-sum game. They cooperate to grow the pie, perhaps at the expense of suppliers, competitors, labor, investors or customers. They exploit comparative advantages to lower overall costs, lower risks and increase benefits. They share or signal their relative priorities. They fulfill their commitments. They create incentives for sustained cooperation. They cooperate to build market power. They manage customer expectations. They under promise and over deliver. They manage the government. They build shared cultural expectations and priorities. They build personal relationships. They manage large risks. They manage and coordinate supply chains. Modern business is complex. The real winners understand and deal accordingly.

Summary

Trump’s dealmaking approach fails on every critical dimension. It is a losing approach for almost all firms and for all countries. His supporters need to understand that he cannot win with his approach and force him to change. His opponents need to highlight these failures. The United States has too much at risk from Trump’s losing strategies.

The US imports and exports about 1/8th (12%) of its Gross Domestic Product. Argentina, Brazil and Pakistan have a similar level of trade to GDP. China and Russia are closer to 1/5th (20%). The world imports and exports 30% of it’s GDP. European countries import and export 45% of GDP. The US is the most self-sufficient country in the world. It imports select commodities, labor intensive goods and luxury products. It exports high value-added goods and services supported by its high value-added and compensated workforce. As the US president threatens the large benefits of global trade to the US and the world, it’s very important to place the US within this context. U.S. trade may be less advantageous than someone’s vision of ideal, but based on size alone, international trade is clearly not a first-class priority for the country, its firms or citizens.

Journalists, artists, pundits, entertainers and politicians all scheme for our attention. Once upon a time … we briefly thought that the internet and social media might usher in a new age of information, selection, objectivity, useful filtering, wisdom and cooperation!!!! Unfortunately, we are now deluged by “least common denominator” communications skillfully targeted to lure us into a non-stop cycle of clicking on marketable links. These communications very effectively use every trick and technique to appeal to our emotions, prejudices, weak attention, surface thinking, fears, hopes, exaggerations, etc.

Politicians of all flavors have conspired to convince us that the whole world is comprised of “good versus evil” people, politicians, parties, religions, states, policies and institutions. Everything is “win/lose”. Disagreement is motivated by bad ideas and motives rather than differences of opinion or interests. Compromise is a sign of weakness. Every political actor is purely motivated by self-interest.

We each have a moral, political, social, religious and personal responsibility to evaluate these “conclusions”. Let’s start with overturning the idea that we have nothing in common, that we must rely upon politicians to define opposing policies, parties and philosophies and fight to the death for one or the other to finally win.

Human Nature

Biologically we are all the same.

We intuitively and rationally combine thinking, feeling and doing; conscious and unconscious drives.

We each think that we are “right”. As in Lake Wobegon, we are all “above average”. We struggle to maintain self-awareness, to consider the needs of others, to even pursue our own goals consistently and effectively. We are functionally and morally imperfect.

We have a variety of needs and desires that cannot be fully met. Safety, acceptance, achievement, agency, transcendence, control, familiarity, influence, consistency, love, health, growth, expression, authenticity, loyalty.

We are primarily “analog” beings.

Human Experience

We face death, evil, suffering, disappointments, violations, violence and pain. Random, irrational, unavoidable experiences. We often respond with fear, anxiety, cautiousness, anger and victimhood. We search for ways to “manage”.

We experience life through time, learning, relationships, lessons, goals, planning, dreams, hope, commitments, doing, feeling, thinking, feedback, taking risks, managing risks and opportunities, engaging, disengaging, focusing, relaxing, looking outward, looking inward. The journey is complex and the perspective changes.

We balance and prioritize. Limited resources. Unlimited desires. Personal, family, social, community, religious, financial, and health dimensions compete. At best, we fight the many demands to a “draw”.

We struggle to keep up in a world that becomes more complex every decade: personal choices, goods and services available, information available, technical complexity, political complexity, social choices, religious choices, communications options, philosophical choices, scientific results, business complexity, international options, cultural options. More options, more choices, greater expectations.

We live in a culture that prioritizes the economic dimension of production and consumption. We have embraced a meritocracy that offers great rewards to the winners and a modest “safety net” to those who are not winning. Economic and status anxiety are very high in the most economically successful nation in history. We promote an extreme personal responsibility that undermines those who don’t always achieve and sustain their highest goals.

We live in a world that has been labelled the “therapeutic society” or the world of “expressive individualism”, summarized by the US Army slogan of “Be all that you can be”. The individual is responsible for living and achieving a great life of personal expression reflecting their talents and possibilities. The individual has many coaches, advisors, mentors and therapists, but is alone in choosing their “destiny”. They cannot rely upon tradition, religion, culture, nation, village, parents, personality profiles, or skills assessments. This radical secular humanism view places the responsibility for identifying and achieving a “world changing” destiny upon each person. Wise individuals find some way to “balance” this personal responsibility with other influences, refusing to adopt a godlike stance. They avoid becoming like Icarus and flying too close to the sun.

We live in a world that highlights the individual above nature, community, culture or religion. Complete individual liberty, freedom and opportunity are desired. No trade-offs with the other dimensions of life. “Natural consequences” frustrate those who embrace this libertarian ideal.

Life is hard. So many advances in society, business, education and technology. The challenges to “living a good life” are greater than ever. The progressive promise is undermined. All individuals must now make choices that were once reserved for kings, priests, princes, monks, scientists, philosophers, artists, governors, generals, financiers, industrialists, explorers, entrepreneurs, and presidents.

Culture

We digest the beliefs, norms and values of our culture subconsciously. The legacy of Christian Western Civilization continues. The legacy of secular humanism continues. We live in a “secular age” where deep faith and unskeptical religious commitment is unusual for the highly educated one-third. We’re “neither fish nor fowl”. Culture really matters but is today a blend of two streams like “oil and vinegar”. There is much in common. There are some big differences. We generally share the political, economic, social, religious, scientific and literary history of Western Europe, even though parts of the intellectual community have promoted disturbing alternate views for almost 200 years.

Despite living in a “secular age” and an “individualistic age”, we all need to be connected to various communities. Although community participation frequency, manner and depth vary greatly across the decades, humans always need to be connected.

We share a legacy and currency of art, media, design, architecture, music and entertainment. High-brow and low-brow. Mass market and specialized. Push versus pull connectivity. We are connected.

The US remains an unusual Western society where the not-for-profit, religious, social, volunteer world performs major social welfare functions. We share our experiences of funding, volunteering, leading and consuming from these organizations. The individual and community experience of managing these organizations shapes our world view. Our individualistic bias combines with our social/religious obligations to create and support these organizations.

We share our experiences in pre-K, elementary, high school and college education. Mainly public schools. The content shapes our perspectives.

We have moved from 6 to 4 to 3 to 2 to 1.X children per family. We invest like never before in the growth, education, experiences, guidance, mentoring, support and direction of our children. Helicopter parents. Summer programs. Internships. International experiences. The youth orientation reigns supreme.

We continue to value the “social esteem” provided by others. We comply with social norms in every dimension of life. We seek approval. We consume good and services to signal our social status. We achieve, perform and consume based on social influences.

We adopt “tolerance” as a supreme moral value. We don’t advise, influence or interfere with others, even when we strongly disagree.

We continue to struggle with the idea of a “class structure” in America despite the obvious growth in economic, social and political influence of the wealthy (top 1%) and the professional class (top 10%).

Communications

We share the American “English language”. It dominates the whole world.

We share the mass media, local newspapers, industry and professional journals, scientific and academic journals, the entertainment industry, social media platforms, community forums and the internet.

We share modern communications and information technology. A “smart-phone” is in every pocket, instantly accessing the cumulative knowledge and information of mankind.

Religion

Americans are much more “religious” than “Europeans”. We mostly believe in God and spirituality and Christianity. We have seen that shared cultural/religious beliefs can be maintained in a religiously pluralistic society. We believe in objective “right and wrong”. We intuitively accept “the golden rule”. We see “America” as part of God’s plan and history. A place for the pilgrims. A land of religious diversity. The overturning of slavery. American victories in the 2 world wars and the cold war. The moral dimension of life matters.

Economy

We still live in the world that Adam Smith described in 1776. The degree of specialization is only limited by the extent of the market. Our world is extremely specialized. A bewildering variety of products are available. Outsourcing of many functions. Regional, national and international sourcing.

We all specialize in our most productive functions today. Profession, sub-profession and industry. We all have talents. There are most highly rewarded in their professional roles.

We are producers and consumers, investors and suppliers, professionals and managers, entrepreneurs and directors. We are deeply engaged in the financial system, markets for labor, money, trade, property, goods and services. We sometimes elevate this role to be “everything”, to our detriment.

We are interdependent. We rely upon “essential workers”, universities, governments, builders, contractors, consultants, bankers, utilities, media, lobbyists, politicians, unions, secondary markets, employment firms, lawyers, engineers, IT and communications folks, etc.

We rely upon the US macroeconomy. Budget deficits. Fiscal policy. The Federal Reserve Bank. Monetary policy. Federal banking and industry regulators. The bond markets. The credit rating agencies. Animal spirits. Wall Street. Mutual funds. Municipal bonds. Mortgage bonds.

We rely upon our commitment to the capitalist, free market, free enterprise system. Laissez faire. Limited government regulation. There are specific situations and metrics that warrant government intervention, but we lean towards allowing the natural incentives of the market to police the behavior of great firms.

We believe that economic growth provides the opportunity for the political system to effectively “redistribute income”, ensuring that the economic value added by scientific and business innovation through time does not all accrue to the owners.

Globe

The benefits from international trade are well understood and have been demonstrated for 75 years.

There are opportunities to engage all nations to manage diseases, food supplies, hunger, human rights, refugees, public health, travel, immigrants, trade, communications, and ocean resources.

There are global threats that must be managed: climate change, nuclear war, chemical and biological weapons, computer hacking, artificial intelligence, species loss, food production, energy production.

Philosophy

An objective physical reality exists. An objective moral reality exists.

The individual really, really matters. Human rights.

The scientific method applied to technical issues is great. It is not everything.

Instrumental logic is a tremendous asset for science, business and life.

Pragmatism is always worth considering. “Show me the money”. Does this theory produce measurable results?

We reject anarchy, atheism, pure commercialism, communism, fascism, necessary progress, libertarianism, national socialism, racism, sexism, totalitarianism, utopian socialism, white nationalism, Christian nationalism. In essence, we reject extreme views. We’re comfortable with a “checks and balances” political system that slows changes until they’re embraced by a solid majority.

Politics

The US is a world of skeptical politics. Less is more. Trust no one. Engage the local community to find a solution. Accept the individual bias in economic and social laws. America is a special place, worthy of patriotic respect.

Political participation is a sacred duty.

Despite the structural constraints on change, the US has generally been a positive, constructive, progressive supporter of political changes through time.

Americans are willing to sacrifice for the good of the nation.

The US constitution is framed by the rationalist enlightenment. We deeply believe in “the rule of law”.

Differences can be resolved, technically, rationally, politically.

We are comfortable with “suboptimal” results from our political system. We accept that the federal, bicameral, functionally divided system is designed to prevent the “worst case” outcomes of raw democracy or concentrated power.

In general, we strongly support our government institutions, especially at the state and local levels. Judges do their jobs. Political parties hold each other accountable. Citizens participate in the democratic process as voters, poll workers, jurors, donors, and volunteers.

Summary

We live as individuals in a complex, interdependent world. We have more opportunities but less authoritative guidance for our lives. We worry about our freedom and liberty. We make many choices. We do the best that we can. We agree on many things yet disagree on many others.

Today, we understand the world better than ever. We also understand ourselves better, our strengths and weaknesses, our possibilities and limits. We manage complex technology and institutions very effectively. We know that some political and economic options don’t work or pose unacceptable risks or threats. The U.S. and Europe developed “limited government” systems apart from religious authority because disagreements were inevitable. We need to relearn those lessons today. We’re going to have a “mixed” capitalist/government economic system. We’re not going to empower any religious denomination or secular group to impose its views on society. We can delegate issues to the states and learn from their experiences. We can compromise. We can “agree to disagree”. Ideally, we can accept that there are some intractable political differences in our society and focus on those areas where we can find agreement.

1981 Oldsmobile 98. The “Main Street” Republican party of 1981. Practical, shiny, powerful, white walls, chrome trim, leather interior, accessible, landau roof, 4 doors, large, American, fender skirts, superior, a known and consistent item.

The 2024 Trump organization has few remaining connections to the 1981 Reagan Republican Party, or that of Eisenhower in the 50’s, Nixon in the 70’s or the Bushes in the 90’s or 00’s. Let’s highlight some of the big differences.

Fiscal conservatism. Balanced budget. No debt. Trump used debt throughout his career, ran record deficits during his presidency and is now trying to eliminate the debt ceiling.

World-class agriculture exports. Trump accepts that US agriculture might take some hits from his “trade wars” approach. He uses various subsidies to partially offset the damages.

Industrial policy. Trump has an activist approach, promoting individual industries and firms that support him and penalizing those who oppose him. Republicans have historically concluded that the market alone is best positioned to invest for growth and the national government role should be minimal, preserving the institutional context.

Competition policy. The Republican party has supported a “hands off” approach. Trump prefers to intervene in the media, high technology, electronics, manufacturing, energy and banking industries. Manufacturing and extractive energy are preferred industries!

Rule of law. Republican investors and owners have relied upon a stable legal environment. Trump asserts that all laws and regulations are subject to his review and interpretation.

Imperial presidency. Republicans pushed to restrain presidential power during decades of liberal activism. Trump has permanently expanded the “rights” and powers of the presidency. Hayek’s “Road to Serfdom” was an early warning.

Fair play. Republicans traditionally sought to build citizen support for core institutions. Trump undermines the FBI, DOJ and IRS.

Free trade. Republicans supported free trade for 70 years as a way to benefit American multinational corporations and citizens. Trump takes a 1920 mercantilist approach to trade, believing that individual country trade deficits are harmful to the US. He believes that the “wins” from individual negotiations are greater than the net benefits of a free trade system for America’s strong world leading economy.

Military strength. Republicans have typically been hawks. Trump views defense spending as an optional investment which should be minimized as possible. He believes that a “strong enough” military and economy, combined with strong deal making and threats is “strong enough”.

Limit military strength. Republicans supported the WWII agreements that limited the military strength of Germany and Japan. Trump sees no reason to limit their military strength.

Alliances. Republicans have supported American alliances with Europe, Japan and other supporters of the “American Way”. Trump views these alliances as “welfare” for other countries. The U.S. is providing military, economic and institutional support without extracting tributes from the allies.

NATO. Republicans have always supported this counterweight to threats from Russia. Trump sees Russia as a “reasonable” adversary which is not interested in threatening the US. Europe should protect itself from Russia.

Global international order. Republicans have generally supported the various global organizations supporting the Western-defined economic and political systems following WWII. UN, associated organizations, WTO, IMF, World Bank. Trump views these organizations as an extra investment for the US and a threat to US interests. He prefers one-to-one negotiations rather than this universal approach to defining and enforcing US interests.

Institutions. Republicans have supported the main US institutions which have supported the American way. Trump questions all government departments, public education, universities, the mainstream media, journalists, and Hollywood.

Science. Republicans have historically supported American science and scientists, based on military, social and economic results. They have believed in professionals and objective reality. Trump believes that many scientific views are really political views, subject to political control. The contrast in medicine/public health is greatest.

Conservative philosophy. Starting with William F. Buckley, conservatives developed a consistent “conservative” world view that linked together social, political, military and economic dimensions. Trump has no conservative philosophy. He is purely transactional.

National Leaders. The Republican Party was based in the Northeast and Midwest. It dominated the country from 1860-1930 and again in the 1950-80’s. Traditional large metro areas provided intellectual and political leaders. Trump has abandoned the east and west coasts.

Conventional. Republicans embraced the preservation of history and convention. Trump is a revolutionary, seeking to overturn the “modern” FDR, LBJ “new deal” consensus on economic, social and political issues that he opposes. Judicial overturn of abortion rulings is “exhibit one”.

States rights. Republicans have supported “states’ rights” to preserve conservative social positions. Trump seeks to enforce national decisions.

Separation of Church and State. Republicans quietly accepted the need to preserve religious rights and allow the state to be “neutral”. Trump and religious conservatives question this solution. They worry that secular interests are indoctrinating students.

Anti-communist, anti-fascist, anti-totalitarian. Republicans generally embraced the “American Way” and opposed alternate views. Trump is purely transactional.

Western culture. Republicans believed that the post-war consensus of democracy, human rights, mixed market capitalism and international order was effective and right. Trump does not believe that the US should promote its ideals. All international relations are purely transactional.

Fixed monetary policy. Republicans have pushed for a “rules based” monetary policy to limit the risks of an “active” monetary policy. Trump wants to control the Federal Reserve Board to promote low interest rates.

Character. Republicans have highlighted “character” as an essential trait of any national leader. Trump dismisses “character” as irrelevant.

Russia. Republicans fought the cold war against Russia. Trump sees Russia and Putin as just another global competitor, no better or worse than many others.

Special relations. Republicans have supported historical US relations and agreements. Trumps sees everyone as transactional. NATO, Japan, Korea, Australia, Canada, Mexico, UK, France, Germany.

Summary

Republicans, like all political parties, have shuffled their coalition partners through time. The Reagan coalition was not the Eisenhower coalition, but the differences were minor. The Bushes generally embraced the broad “conservative” Reagan tent. Trump is clearly not a “philosophical” conservative. He is not trying to conserve a culture and its main institutions. He believes in a radical individualism closer to libertarianism and realpolitik. The world is dangerous. It is only win/lose. Only great deal makers can deliver results. The whole is the sum of the parts. “Trial and error” is an essential approach. There are very clear differences between the historical Republican Party and Trump’s views. I think they will become more apparent as Trump tries to implement his views.

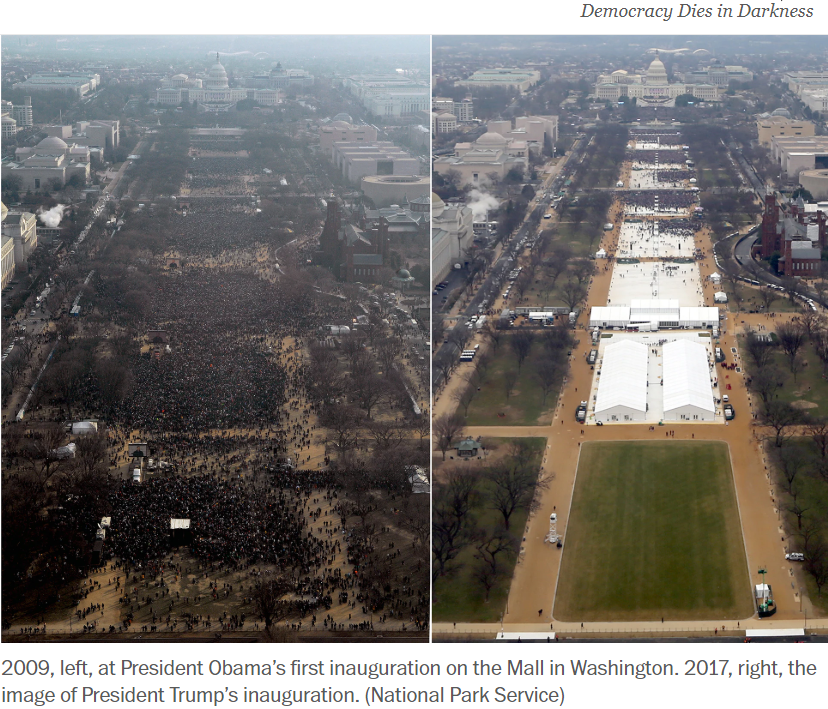

Trump’s 2017 inauguration crowd was only one-third the size of Obama’s in 2009. I was there in 2009. The wind chill was around 10 degrees. Trump’s REAL and deep foreign policy support among Republicans is similarly quite small.

Trade wars, attacking allies and driving an active industrial policy all undermine the US economy, resulting in lower GDP, lower tax revenues, higher spending, a greater budget deficit and higher inflation. Fiscal conservativism was recently the hallmark of the Republican party. It helped to unify the various flavors of conservatism. Everyone could agree on a balanced budget amendment, no trade-offs of higher taxes for increased spending, and threatening a government shutdown and possible debt default in order to force congress and the president to address the budget deficit and the growing federal debt. The real situation is worse today, with larger debt as a share of GDP, a forecast increase and a large annual budget deficit during a time of 4% unemployment. Trump’s headline foreign policies threaten the economy. Despite the Federal Reserve Bank’s reduction to the benchmark federal funds rate, long-term interest rates have drifted upwards. Will a Paul Ryan re-emerge?

(2) Corporate America

US based multinational corporations have thrived in the 75-year post-war era. They benefit greatly from the opportunities that free trade provides. Tariffs, trade wars, restrictions, industrial policy and presidential interference all reduce profits and increase risks. Trump may reduce corporate taxes and regulations, but international tariffs and regulations will hurt corporate bottom lines. The net benefits may quiet some corporate leaders. Others will incur greater harm and work to protect their interests.

(3) Agriculture/Rural America

American agriculture is a world class exporter. It thrives under consistent patterns of free trade. Trade retaliation is a big threat to agricultural revenues, profits and land values. Production agriculture is just 1% of US GDP, but it exceeds 5% of GDP in 1,130 American counties, averaging 14.11% of the value of production in this one-third of America geographically. In the other two-thirds of the country, agriculture accounts for just 0.36% of GDP, so it’s politically irrelevant. American agriculture has always been disproportionately effective in politics. Trade wars may soon have one-third of American counties up in arms.

(4) Philosophical Conservatives

Proven cultural and institutional frameworks are best. If it ain’t broke, don’t fix it. Support countries with similar cultural institutions and values. Protect the interests of the wealthy and powerful against the claims of the fringe interests. Isolationism, protectionism, and “do it yourself” foreign policy are unproven and risky strategies. The philosophical conservatives enjoyed a nice run from William Buckley’s 1950’s through the rise of the “tea party” in response to the Great Recession. They were amongst the first and strongest opponents of Trump’s views and have led the “never Trump” movement. They were never a large share of the party, but they provided a mental framework that allowed the components to work together and the conservative think tanks and media to earn a degree of respectability in the court of intellectual public opinion. Trump’s character challenges and blatant transactionalism and individualism cannot be reconciled with their views.

(5) Wall Street/Banking

America dominates international finance and banking. Raising capital, making markets, advising firms, and making risky investments. The global financial system works for Wall Street. Rapid and unpredictable changes to the “rules of the game” increases risk levels and makes global investments harder to plan, finance and execute.

(6) Hawks/Neoconservatives

Might makes right. Don’t fall for ideals. This group agrees with Trump on basic principles but can’t understand why anyone would undermine the highly valuable postwar alliances that the US has developed with NATO and individual countries because “they don’t pay enough” or “they win too much in trade”.

(7) Economic Free Marketers

True believers in capitalism and free markets see it as the best way to create and preserve value with the added side bonus of protecting individual liberty. Tariffs and active industrial policy are the traps that idealistic Democrats fall into. Republicans know that only the market, in the end, will deliver prosperity and liberty. Trump’s preference for a very active foreign economic policy and a relatively active and intrusive domestic economic policy does not match this group. They can embrace his general low tax, low regulation, only results matter views.

(8) Libertarians

Same as above on economic policy issues. There is a huge risk of the empowered centralized state, stripped of checks and balances, turning around and threatening individual liberties. A centralized totalitarian or fascist state is a huge threat that must be avoided at all costs. Trump has a libertarian streak, but he does not embrace libertarian principles.

(9) Main Street Republicans/Professional Class

This group wants to ensure that the hard-working professionals, managers and small business owners that add value for Americans overall continue to receive their fair share of the rewards. Trump’s “activist” foreign policy puts these rewards at risk. Firms and investors, large and small, will win or lose based upon imposed tariffs, regulations and industrial policies. The economic churn will be much faster, greater and random. A significant number of previously secure upper middle-class professionals will incur significant losses in a much more dynamic Schumpeterian age of creative destruction. The general demonizing of the elites, bureaucrats, experts, intellectuals, scientists, universities, teachers, media, economists, military leaders, pundits, market researchers, pollsters, high-tech leaders, foreign policy community, NGO’s, public health, etc. is a big negative for this group which naturally found a home in the Republican party in the post-war era. Trump’s belief in the “great man” theory of history is at odds with the mildly progressive culture of suburban, upper middle-class America.

(10) American Patriots/Neoconservatives

The US fought the “cold war” against communism for 50 years. Trump thinks that Putin is just another global competitor. Trump’s claim that “Putin’s actions are no better or worse than America’s historically” sounds like something Bernie Sanders might claim! He’s not worried about the communist views of China, North Korea or Vietnam. He’s ready to negotiate. He opposes the “communist” dictators in Cuba and Venezuela. There is no defense of the American values of democracy, equality, free markets or human rights in Trump’s approach. It’s simply America versus all other nations. Tactically and politically, Trump has repositioned China as the new great enemy. Historically, Americans fought the world wars, and the cold war based on the principles of democracy, liberty, freedom, individual values, capitalism and human rights. Trump wants to disengage from Europe and the Middle East while increasing assets to address China, just like Obama. Some patriots just need an enemy, others want to defend principles.

Many cultural conservatives have deep, fundamentalist religious beliefs. Their views are “right” and other views are “wrong”. Trump’s foreign policy is purely transactional. It doesn’t assert that the western or Christian world view is better, preferred or right. He’s not following Bush, Jr. to provide the world with the benefits of American political, economic and cultural systems. He just says that the American people, perhaps with their Christian/western opinions, are worth defending aggressively. It defends some dictators in Russia, Turkey and Hungary who do not share historical American values. Trump’s overall pragmatic, transactional, economics first views don’t square well with cultural conservatives who place moral and religious values first. Trump is delivering a set of Supreme Court and federal justices willing to overturn activist liberal judge rulings and to support legislation passed by culturally conservative states and the US Congress. He’s willing to poke at other cultures, races and nationalities as being “others”, not as good as the true Americans. Younger evangelicals seem less willing than their parents, who have been fighting the “culture wars” for 50 years, to embrace Trump at a transactional level and give up their ideals. Trump’s anti-immigrant posture, protecting America from the threat of the “others” does resonate with some cultural conservatives. Net, net, Trump is not losing support from this group due to his international policies.

(12) Victims of Economic and Social Change

This group clearly supports Trump’s populist diagnosis and prescriptions. The loss/decline of American industry was due to international traitors and coconspirators who undercut the owners and workers. It was all avoidable. Economic, banking, university, media and political elites conspired to undermine the domestic virtuous workers and owners in order to benefit “others”: other countries, religions, races, cultures, classes and interests. The story is just like Hitler’s description of the Weimar Republic leaders. The country was sabotaged by traitors. This is a very powerful story. Many Americans today buy this story. For how long?

Summary

Politics is all about telling a story and managing coalitions. Ronald Reagan told a very attractive story that wove together the various strands of conservatism into a coherent narrative. This story reframed American politics. Presidents Clinton and Obama confirmed the core conservative story, just like Eisenhower and Nixon confirmed the core New Deal story earlier. Newt Gingrich triggered both parties to adopt a polarized world view.

Trump leveraged this situation to attract economically and culturally disadvantaged individuals to embrace a greatly reformulated conservative, Republican, red, populist world view. Trump’s international relations policies don’t really fit well with the historical views of the Republican party. It remains to be seen if these mental conflicts will undermine his political support as he is able to implement them and deliver results. He is “riding on the coat tails” of broad popular support for “conservative” solutions to our many challenges.

International affairs have been secondary priorities for the last 50 years. They were top priority in the quarter century after WWII. Trump’s emphasis may make them top priority once again!

The world faces five issues that require global solutions.

Risk of global war, including nuclear war

Risk of a pandemic that kills billions of people

Risk of global warming accelerating out of control

Risk of China and the US unintentionally destabilizing all global systems

Risk of the international economic order breaking down, impoverishing billions

The world has found a variety forums, agreements, institutions, relationships, indirect promises, incentives and threats that have “managed” such risks for 80 years. Unilateral bargaining has not been the best solution.

Some Trump Approaches to Consider

International relations, economics, military and migration are very important and should be treated as top priority by the USA.

The US has a variety of power bases that could be more actively used. Military power, nuclear power, dollar as the reserve currency, tariffs and trade restrictions, soft cultural powers, SWIFT currency system, immigration laws and enforcement, educational systems, regulation of major global corporations, treaties, global military bases, market size to allow protectionist policies/threats, leading universities, intellectual property, strategic asset reserves, technology leadership, flexible/dynamic economy, small expected role for government, low tax rates, trusted economic institutions, support for the rule of law, independent and effective central bank, extended track record of innovation and economic growth, younger population, global economic and cultural connections, multi-cultural, multi-racial, multi-religious society. Trump emphasizes some advantages more than others, but the basic point that the US has the resources to pursue a more “active” set of foreign policies and negotiations is clear and worthy of consideration.

Pragmatic, transactional, realpolitik approaches should be balanced against idealistic, principled approaches. Win/lose and win/win frameworks should both always be considered and re-assessed based on the current situation in each area of application.

Making automatic value judgements about dictators, authoritarians, fascists, socialists, cultures, races, religions, human rights, capitalism, free trade, globalism, isolationists, and globalists is not the best approach. Countries and leaders resent this presumptuous approach. They oppose the inevitable shortcomings, inconsistencies and self-dealing of the winning post-war coalition. East vs. West. North vs. South. Emerging markets. BRICS. Everyone thinks that they are “right”. Relating at a neutral level has many advantages.

Some situations can be addressed on a purely transactional level without making them more complicated by considering all of the potential issues between the parties.

The US has leverage in specific one-on-one situations where it holds the overall advantage or a single trump card.

Other countries have internal political situations which can be exploited.

Single country deals are easier to reach than regional or global deals.

The views of America’s foreign policy elites, including the military, are relatively similar. They and we could benefit by considering alternative approaches in many situations.

Some degree of inconsistency, deception, changes, flexibility, bluffing, fakes, misdirection, multiple paths, opportunism, threats, espionage, bribes, breaking the rules, etc. are valid components of making and breaking deals.

Less powerful states should not automatically be elevated to “most favored nation” or “sovereign equality” status.

The economic, diplomatic, military, communications and polemical responsibility for maintaining the “global economic order” must be shared by all of those who benefit and not upwardly delegated to the US.

Where Trump Goes Too Far

Soft power is quite valuable for the US. Don’t undermine it on principle.

Alliances multiply the power of the US. Don’t discount or undermine them.

Global bodies and principles can support US interests.

The US is a smaller share of global population, cultural, military and economic power. Going it alone is a risky strategy.

There are very significant advantages of global free trade, especially for the most competitive US based multinational corporations.

Direct pursuit of pure power politics is not supported by many Americans.

The US benefits greatly from maintaining the existing international system of trade and finances.

Sovereign nations and politicians do not automatically respond rationally. They are willing to take “irrational” steps to protect and promote their sovereignty.

There is a value with allies and opponents of maintaining some belief or trust that the US will uphold its commitments, even in the face of adversity or opportunities.

Some results (nuclear annihilation) are so bad that they must be avoided at all costs.

Maintaining long-term allies is quite valuable.

Public criticism of allies undermines their incentive to cooperate.

Trade deficits “come and go”, no real reason to oppose them on a country-to-country basis.

Very successful countries incur trade deficits without harm for many decades.

Embracing or engaging with authoritarian leaders undermines the support of traditional liberal leaders of allied countries.

A consistently transactional approach undermines the expectation that a nation will do “whatever it takes” to pursue its big picture goals and ideals.

There are significant long-term benefits from developing and maintaining allies.

Trade wars are inherently unpredictable, but historically they have devolved into a race to the bottom, greatly reducing valuable trade.

Summary

Trump overemphasizes a win/lose perspective, leverage and direct negotiations. Individuals, firms and countries since WWII have learned that there are win/win strategies and tactics to be considered even when the stakes are highest. Actors have used these strategies because they deliver sustainable results. The best negotiators use all of the tools which are available. They don’t use a hammer as their only tool.

The US economy continues its evolution from agriculture to manufacturing to services to information. President Trump was responsible for the US economy from February, 2017 through January, 2020. President Biden assumed responsibility in February, 2020. In order to compare the two presidents, let’s look at Trump for the 3 years of sustained growth deep in the business cycle before the pandemic. For Biden, let’s look at a comparable 3-year period from June 2021 through June 2024, after the post-Covid rebound. Trump benefitted from an 8-year long business cycle expansion. Biden had to deal with a once in a century pandemic driven economic depression.

Inflation: Advantage Trump

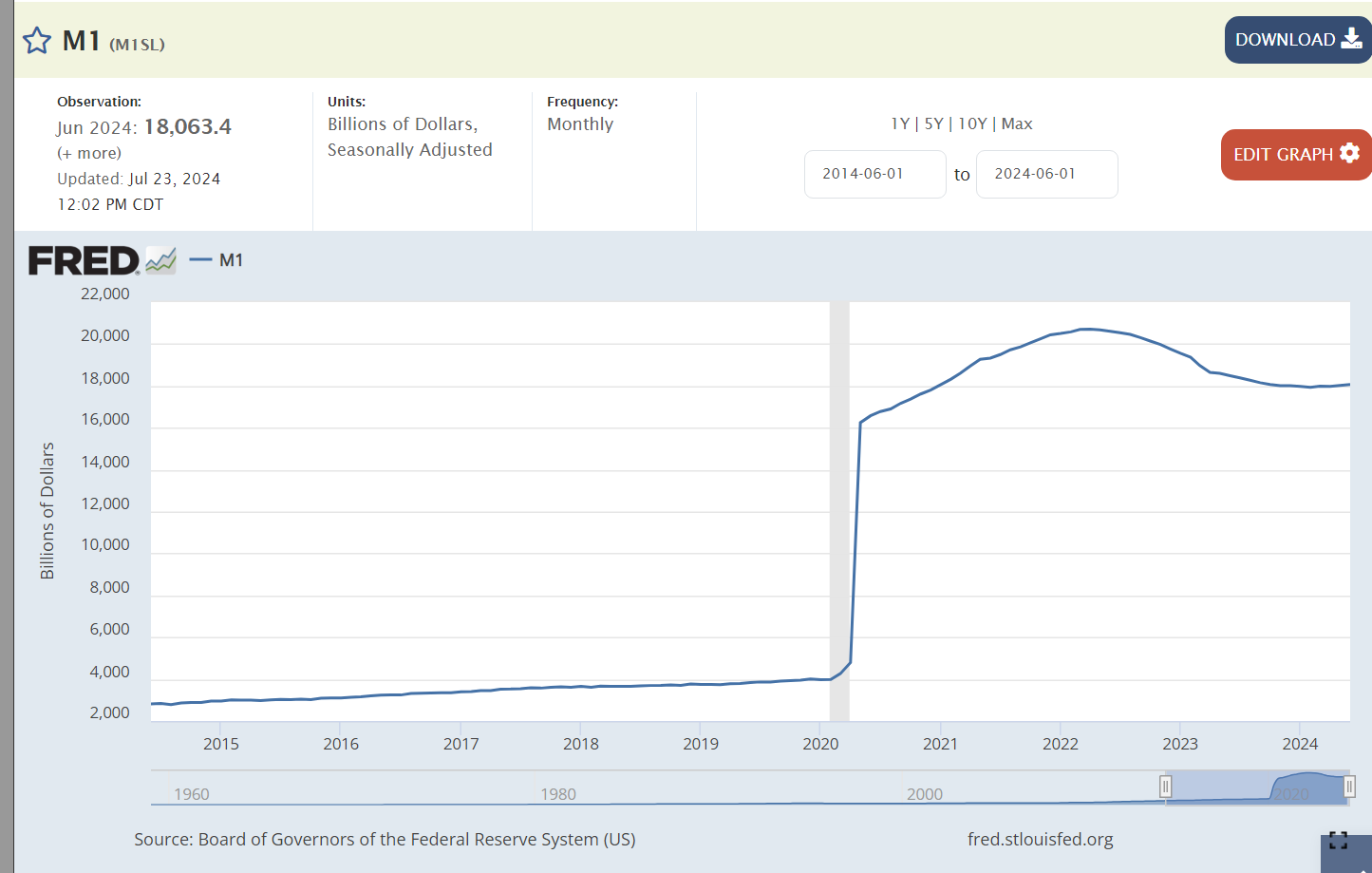

The independent Federal Reserve Board responded to the pandemic by greatly increasing the money supply to ensure that profitable, well-run financial institutions would be able to survive the temporary disruptions in the real economy. The Fed increased the money supply by 4-5 times its prior level to ensure the economy did not collapse! The extra money supply had to end up somewhere. It drove up consumer prices and increased asset values in the stock market and for home prices.

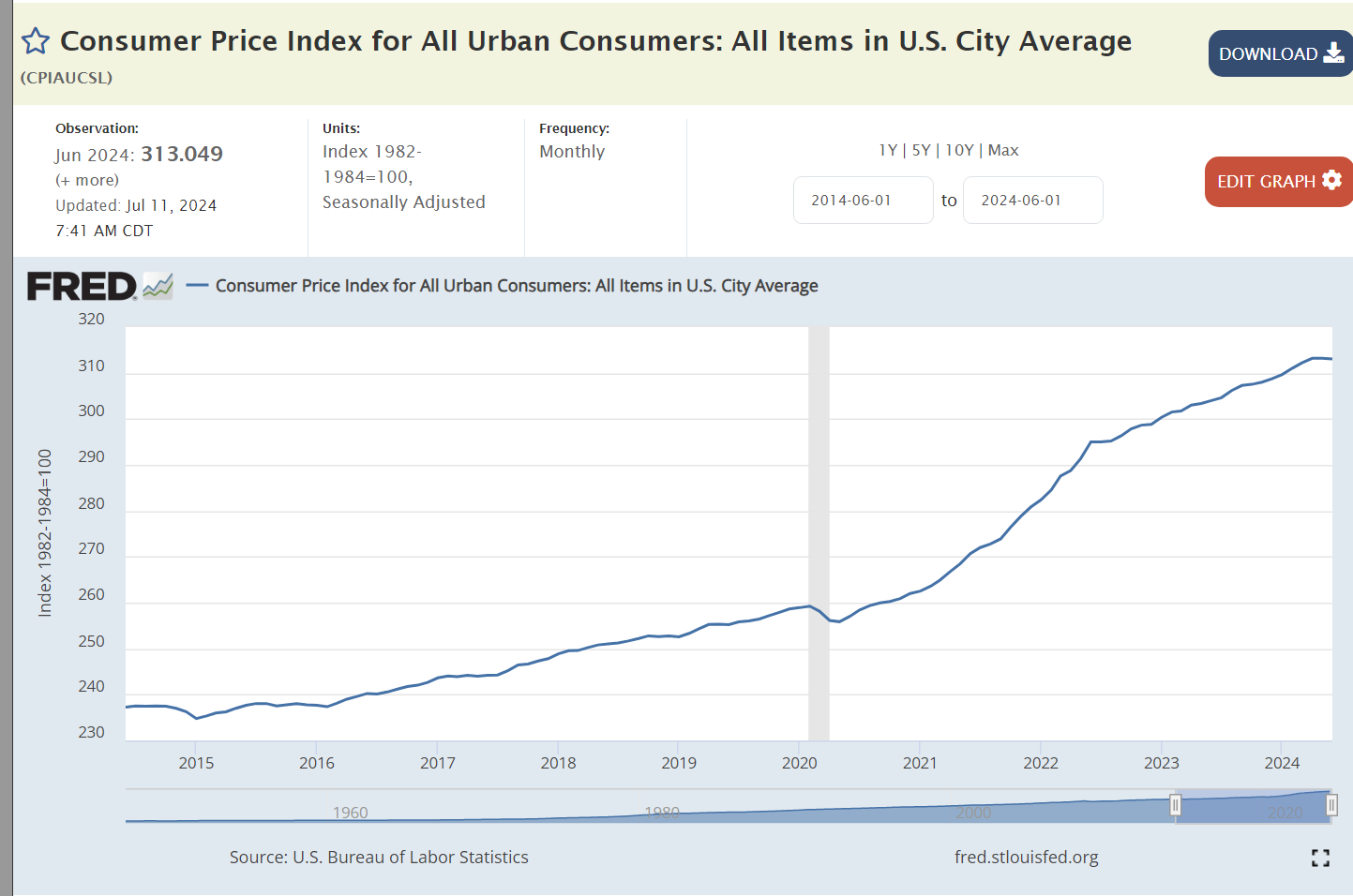

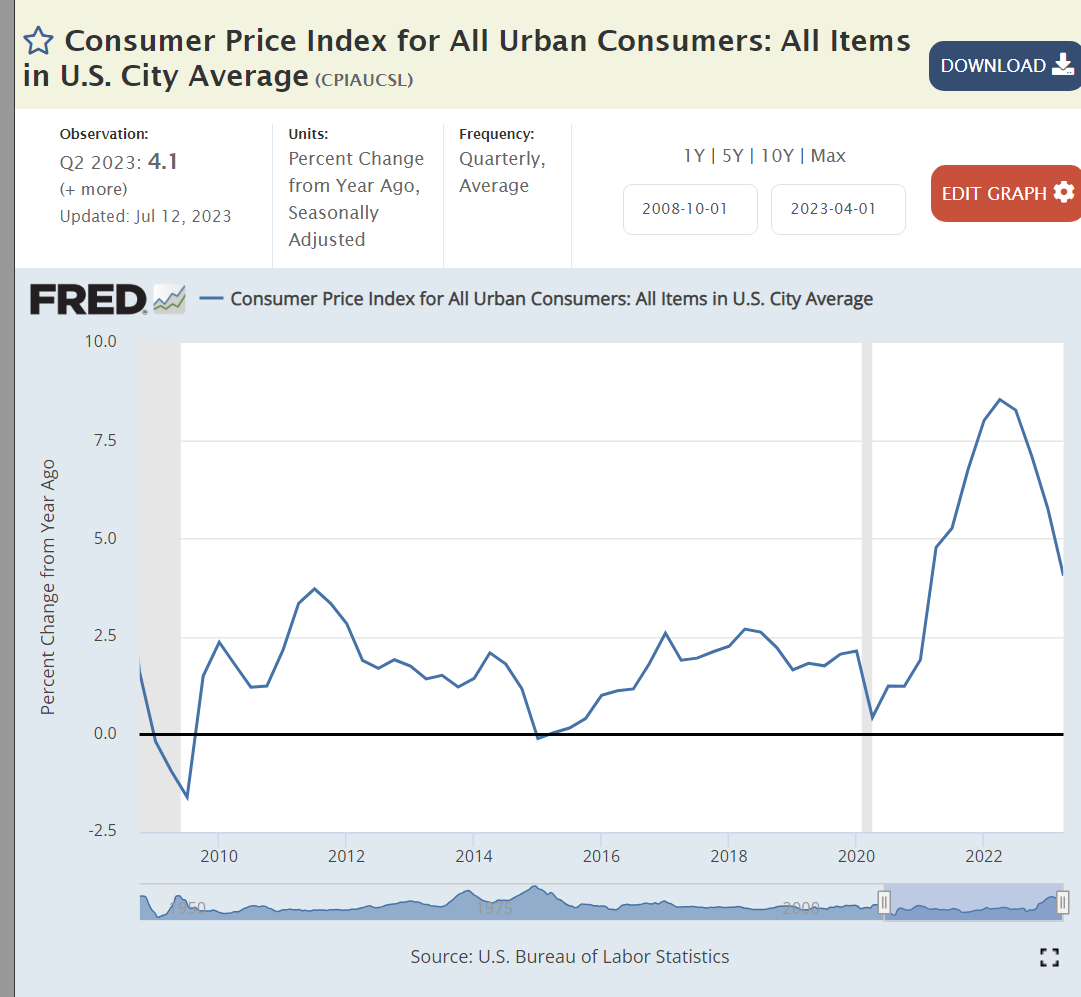

Inflation grew by 2% per year with Trump. It grew by 5% per year, on average, with Biden. Overall prices are 9% higher with Biden. Trump’s economic policies extended the Obama recovery for 3 years without triggering an increase in inflation, despite a low unemployment labor market.

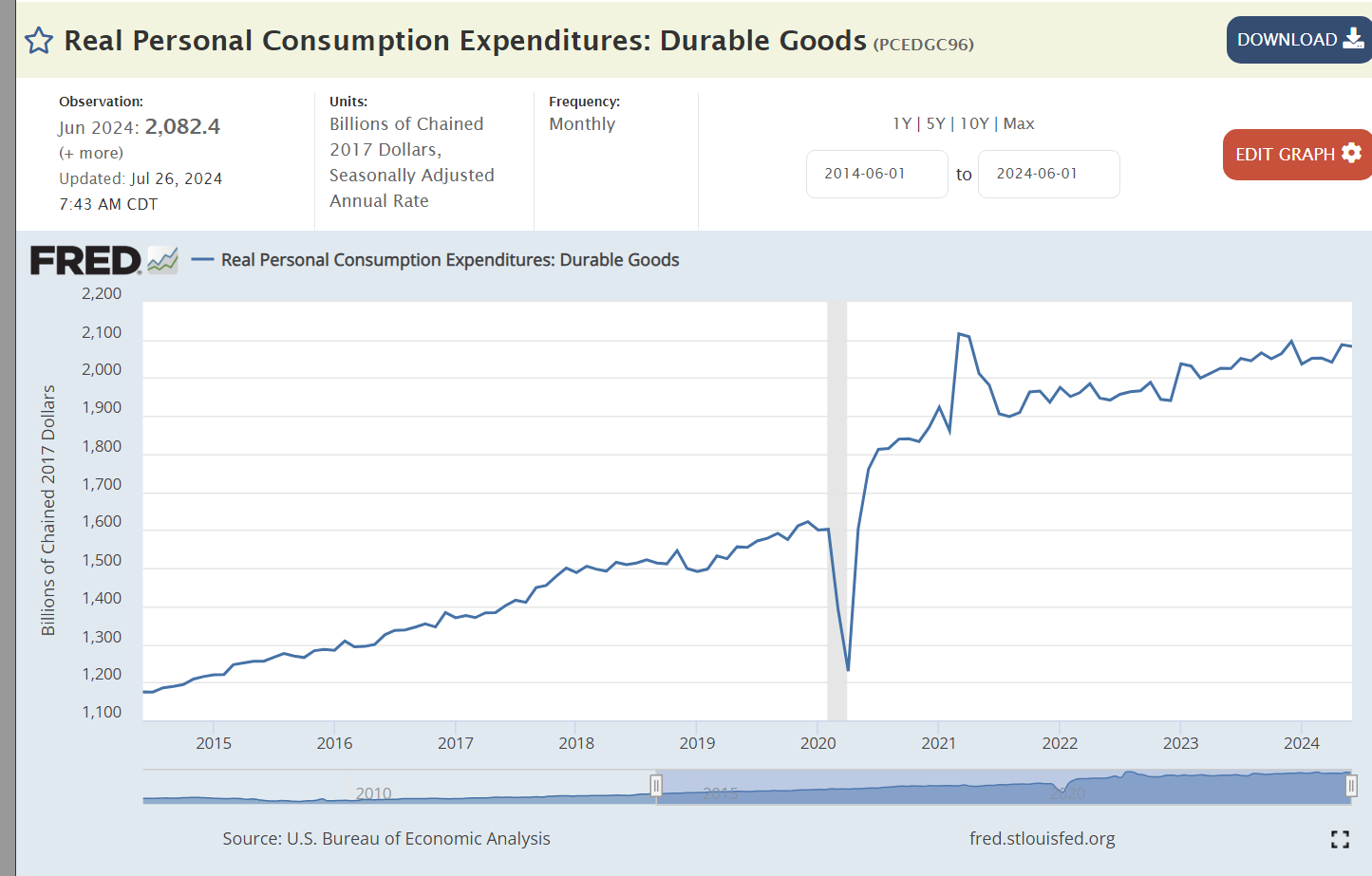

The largest cause of higher than usual inflation in Biden’s term was the 20% spike in US and global demand for durable goods. Factories shut down during the pandemic. Demand rebounded within 6 months as consumers chose to spend money on goods rather than in-person services. Consumer demand at the end of the Biden period is 50% higher than at the start of Trump’s term in office.

Corporations were able to capture and maintain a 50% profit increases due to market disruptions of the pandemic. Experts mostly reject Biden’s claims that corporate profits were the main driver of inflation, but they clearly aggravated the impact of the supply chain disruptions.

Obama was able to reduce federal budget deficits by two-thirds by the end of his presidency. Deficits doubled on Trump’s watch before the pandemic arrived. Biden cut deficits from their record highs during the pandemic, but they have been 50% higher than the pre-pandemic Trump era. Most economists consider the budget deficits to be the main cause of the continued higher than typical rates of inflation, accounting for 3%, 2% and 1% extra inflation in the 3-year Biden time we’re considering.

High profile gas prices remined flat during Trump’s period. Global supply and demand caused prices to increase from $2.50 per gallon to $3.50/gallon where they have remained for the last 3 years.

Trump enjoyed historically low 4% mortgage interest rates, a thin 2% above the inflation rate. The expansion of the money supply drive rates down to 3% during 2020 and 2021. They rose to 7% as inflation rose sharply and has stayed there. Inflation has fallen but markets typically require years of data to reset expectations of long-term inflation which drive mortgage rates. The Federal Reserve Bank has hesitated to cut its benchmark interest rates until inflation is clearly approaching its 2% target.

Labor Market: Advantage Biden

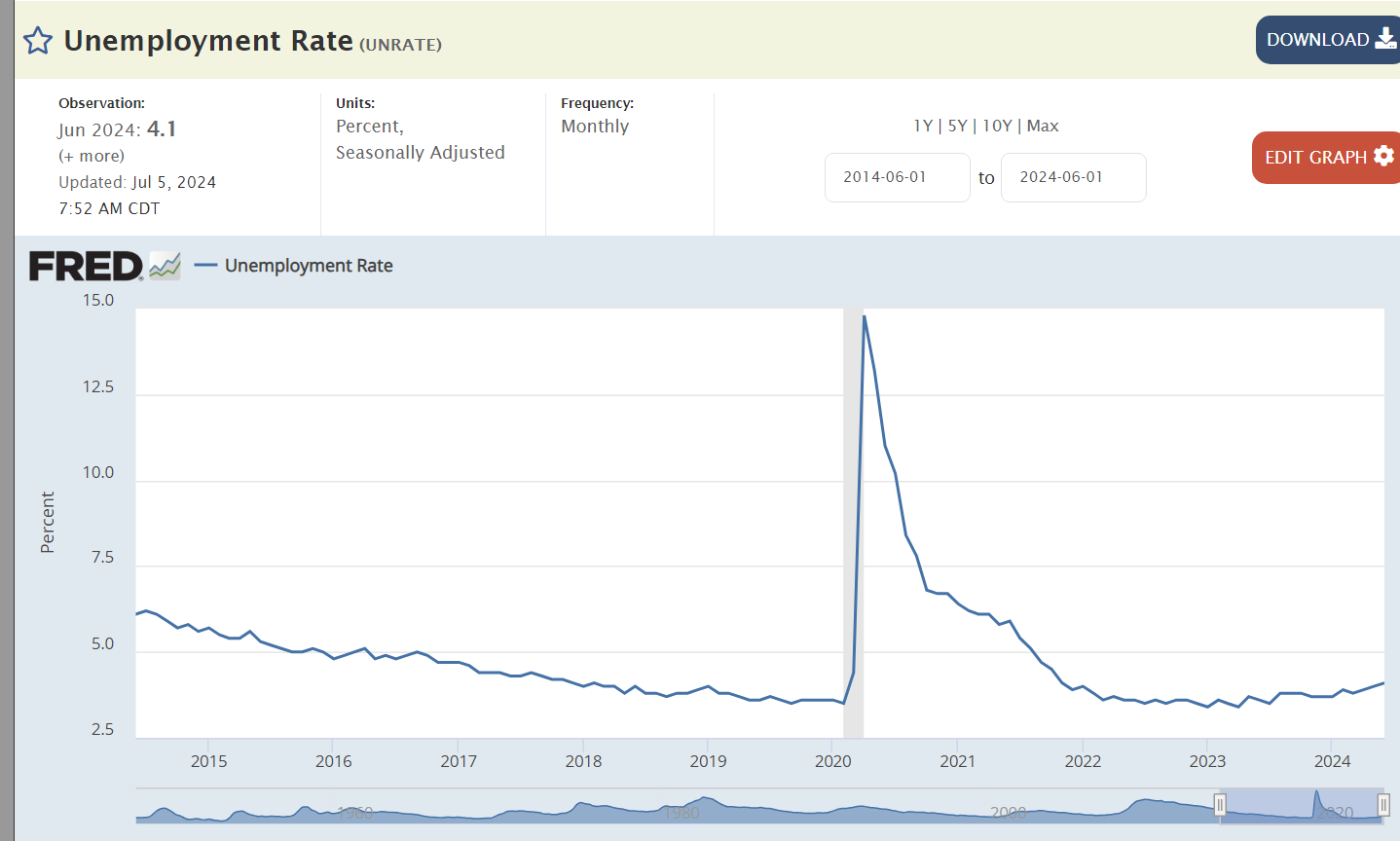

Trump reduced unemployment by 1%. Biden reduced it by 2%. Both presided over best in 50 years overall labor markets.

Layoffs have remained at historic lows, with Biden enjoying slightly lower rates.

Job openings in the Biden market have been 50% higher than the Trump market, reflecting a strong economy with growing labor demand, despite the impact of the pandemic.

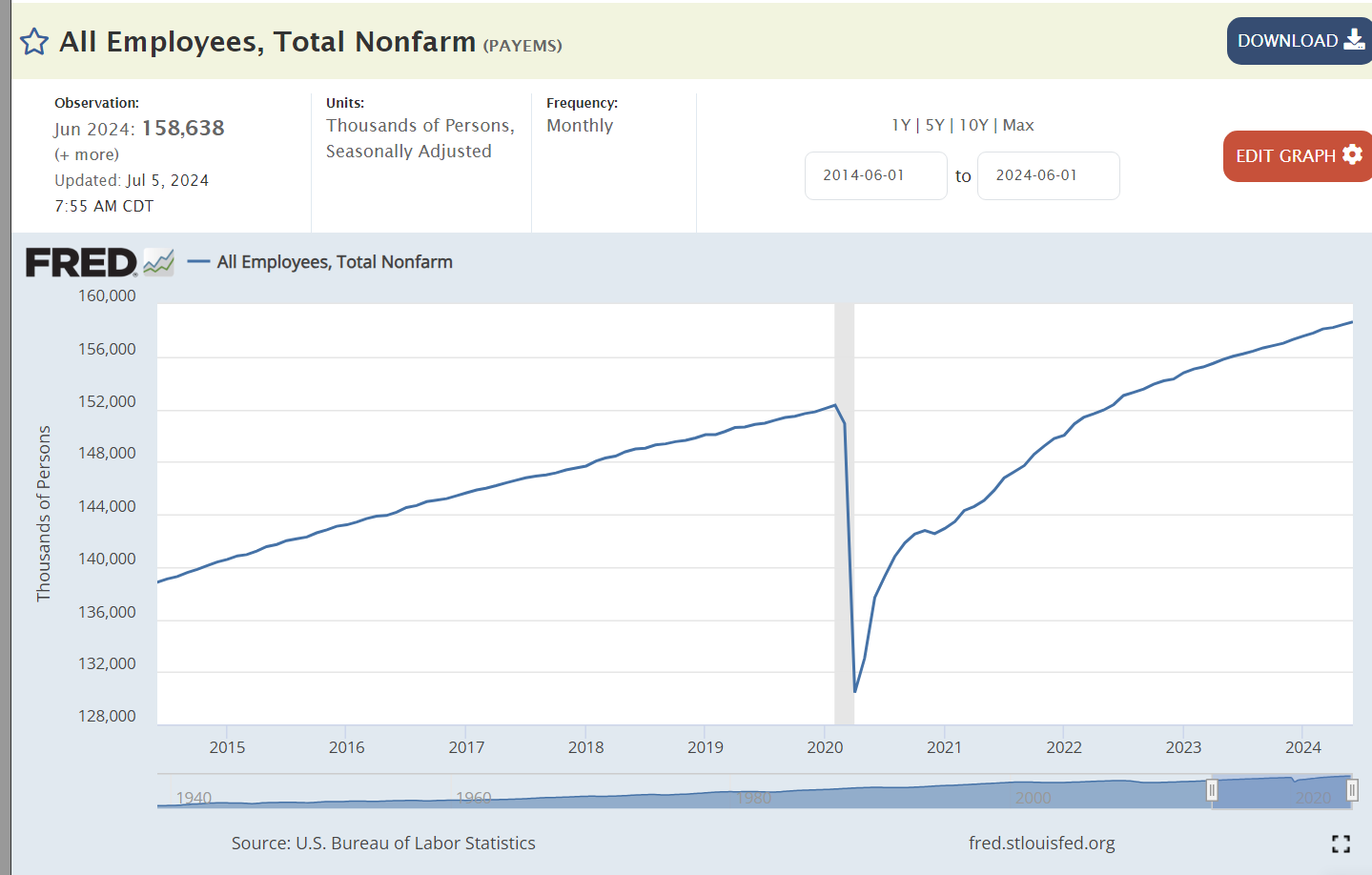

The Biden economy recovered all 20 million jobs lost in the pandemic within 2 years, much faster than expected. Total employment has continued to grow at the trend rate to a record 159 million.

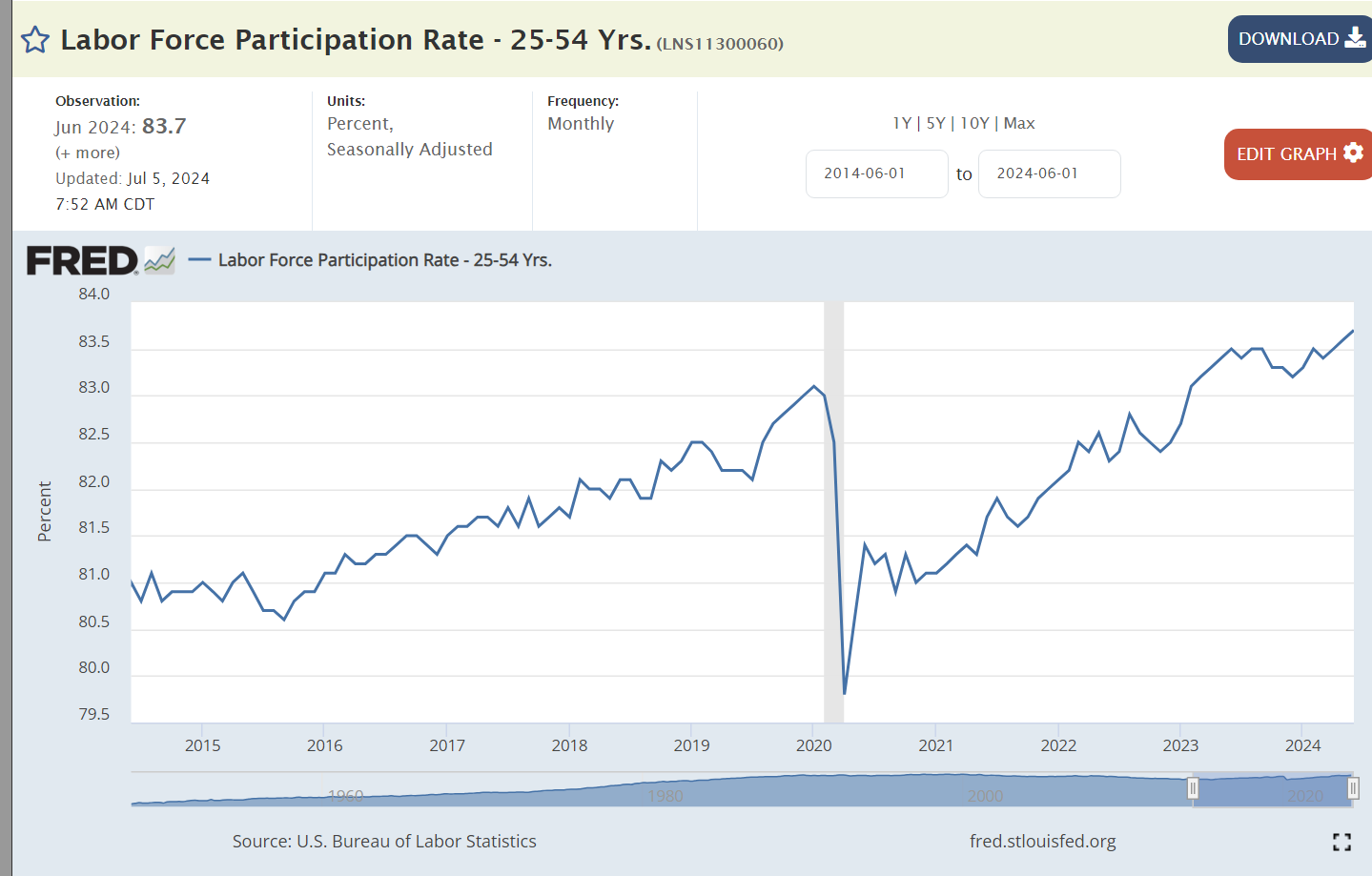

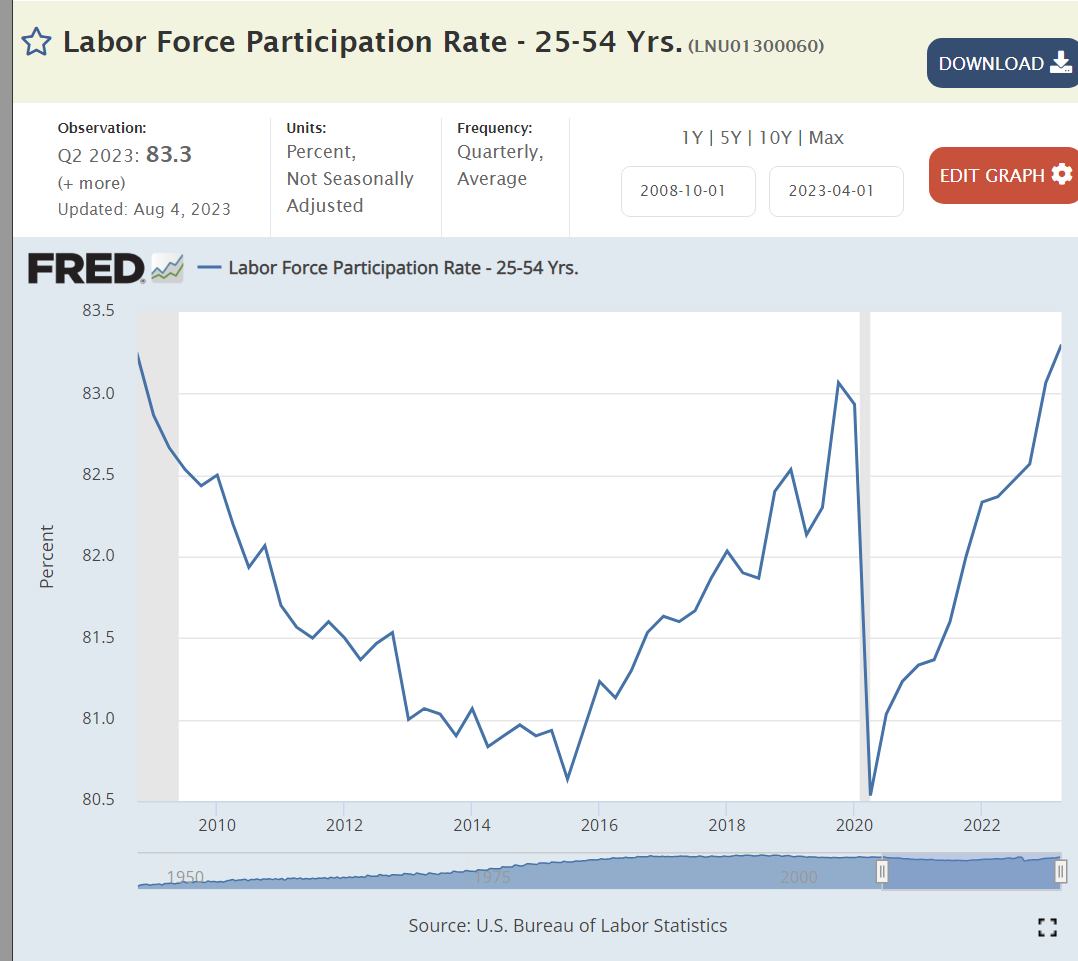

Core labor force participation is 1% higher with Biden than Trump. The current participation rate was last achieved in 2001.

Median real wages have been slightly higher during Biden’s tenure.

Asset Values: Advantage Biden

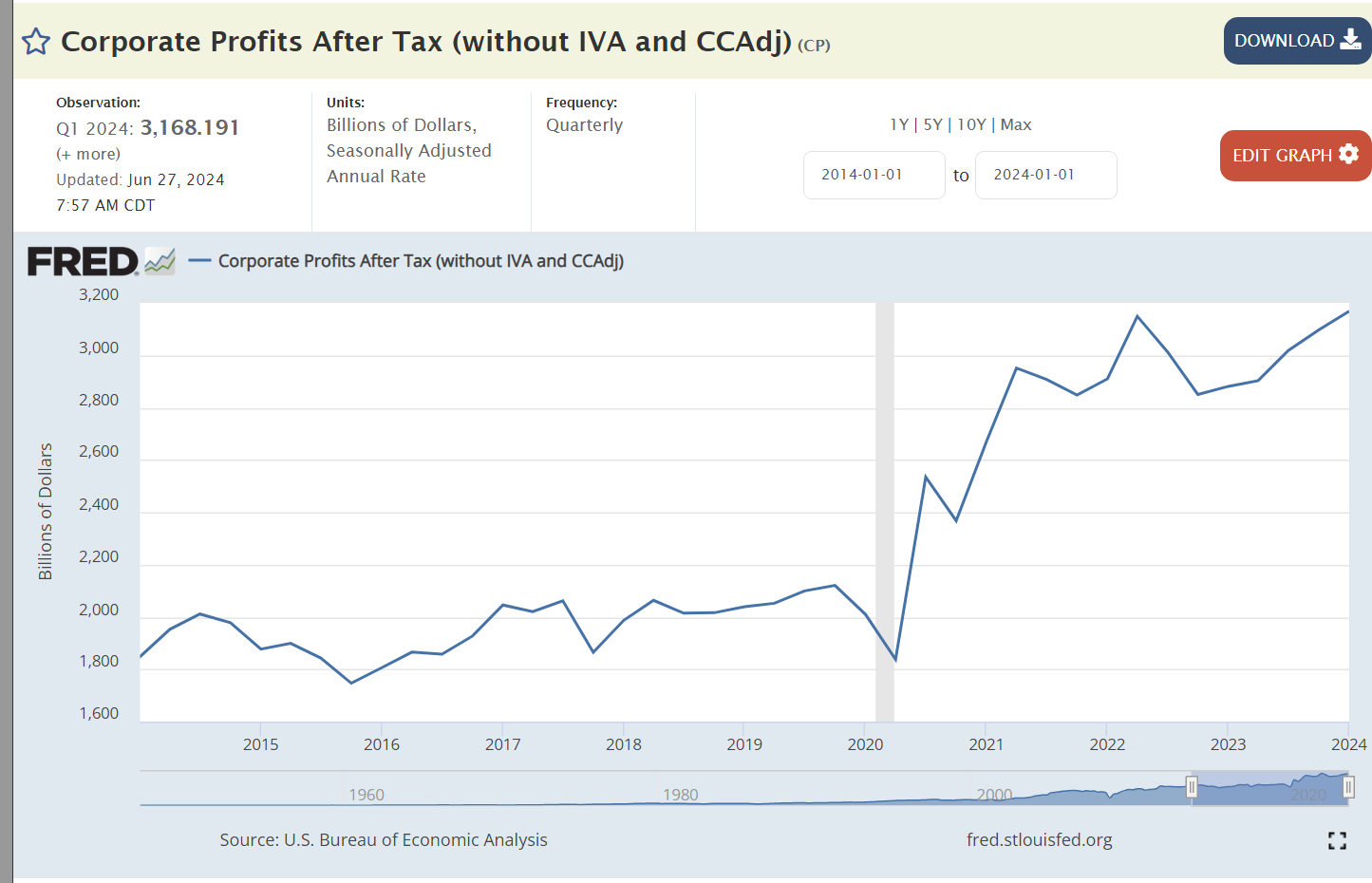

Despite the pandemic disruptions and losses, US firms are worth 70% more today than before the pandemic. This reflects the 50% profits increase and continued positive future prospects.

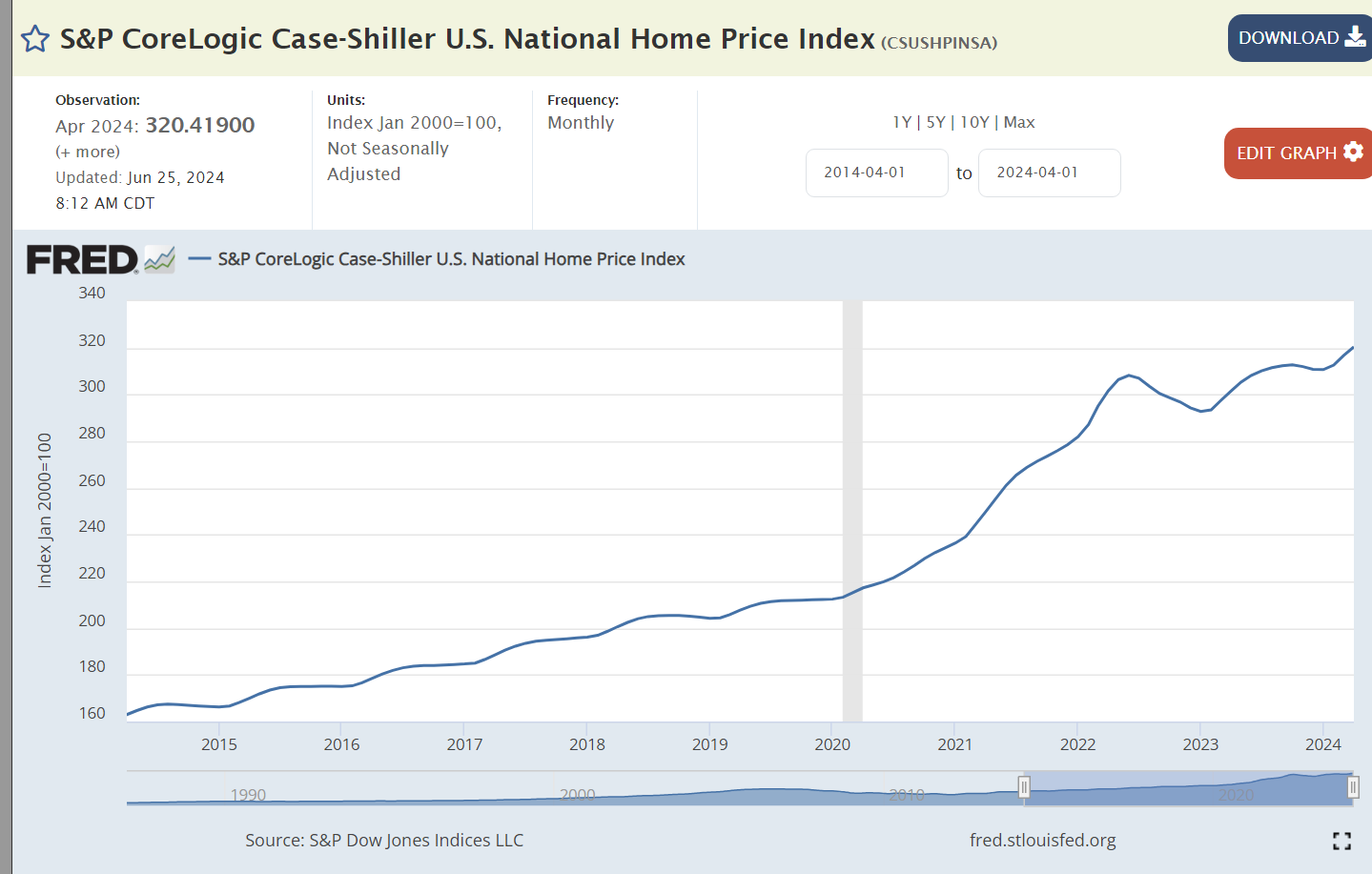

Home prices have nearly doubled since before the pandemic, reflecting the post Great Recession decline in home building, construction issues during the pandemic and general asset inflation caused by the rapid expansion of the money supply.

The US enjoyed a solid 7% savings rate before the pandemic, an extraordinary high 10% after the pandemic, falling to just 4% for the last 3 years.

Human assets increased during Trump’s presidency and resumed growth after the pandemic. As college graduation rates have increased throughout the post WWII years, the cumulative number of college educated individuals continues to rise each year. The growth in masters and professional degrees is noteworthy.

The Economy – Advantage Biden

Population growth has resumed after the pandemic.

The healthy US economy is able to support 3 million more retirees after the pandemic.

Real dollar GDP is 2 trillion dollars larger than before the pandemic disruption. That increase is the same size as the total GDP of Russia, Canada or Mexico. We added the Canada economy during Trump’s time and the Mexican economy during Biden’s time.

Real personal income grew a little bit faster during Trump’s time and more smoothly. Personal incomes jumped up during the pandemic but have been flat since that time with corporations capturing a greater share of the economy’s returns.

Workers have been 8-10% more productive in the Biden economy.

Farm income has doubled in the Biden economy.

Manufacturing employment grew by a surprising 3% in Trump’s term. It is slightly higher in the Biden era.

Real dollar exports increased during the Trump presidency and then again during Biden’s time despite a greatly stronger US dollar which hampers exports.

The world is willing to pay 10% more to hold US dollars in the Biden period, reflecting strong economic realities and prospects despite the risks of higher US inflation and budget deficits.

Summary

The US economy is very strong. Trump was able to extend the Obama recovery for longer than most expected, keeping inflation, interest rates and unemployment at low levels. Biden managed the recovery from the pandemic induced recession better than expected. The economy, asset prices and labor market have recovered very nicely. Inflation has remained the weak part of the Biden economy. It is lower than in comparable global economies and trending towards the 2% target in 2025. Critics point to excess government spending as an avoidable source of high inflation.

The Trump economy built upon the success of his predecessor. The Biden economy overcame the disruption of the pandemic to produce equal or greater results. Both presidents delivered solid results.

Despite doomsayer predictions for the last 20 years, the USA remains the world’s largest economy. China’s population, productivity, property, politics, energy, trade, innovation and middle-income transition challenges have undercut past predictions of its inevitable world economic leadership.

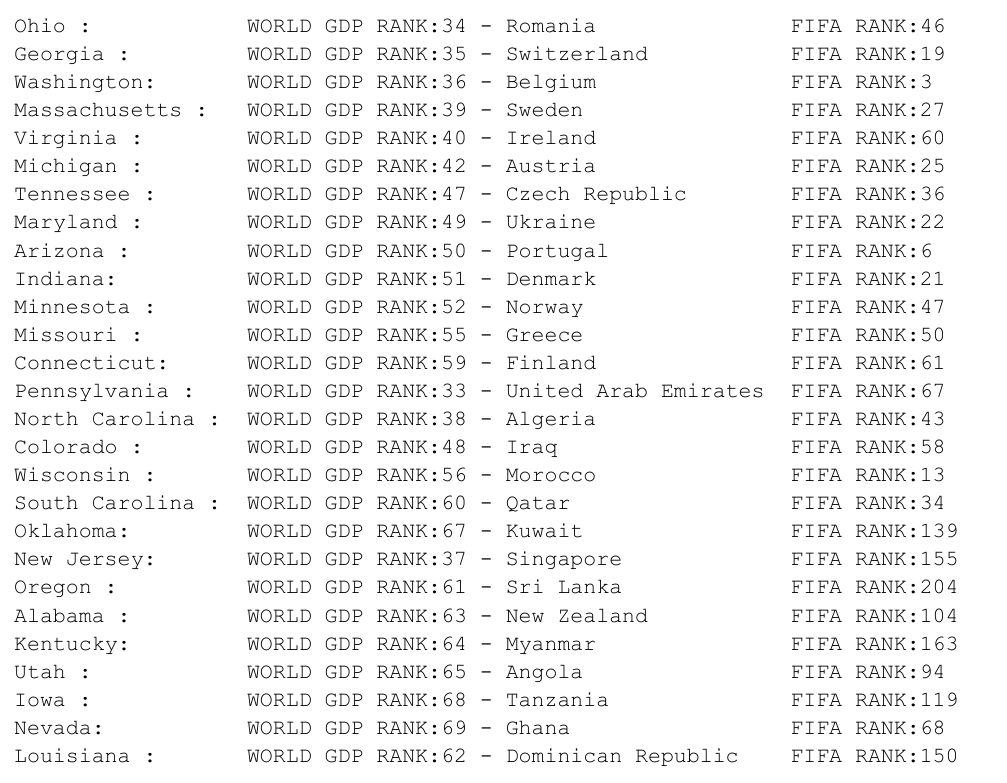

One way to get a tangible sense of the USA’s economic size and dynamism is to compare individual states with other countries. Most of us have read articles highlighting the size of California, Texas, New York, Florida or Illinois as standalone economies. They would currently rank globally as economies numbered 9, 14, 16, 25 and 30, lining up with France, Spain, Saudia Arabia, Vietnam and Argentina in the pecking order. Their men’s soccer teams are ranked 2, 8, 53, 115 and 1 in the world. The US soccer team is ranked 11th and after its recent 5-1 pasting from 12th ranked Colombia it is sure to fall several places.

The real economic strength of the US is shown by the next 27 states. Collectively their GDP is as large as India. These 27 states match up one by one with the next 36 states in the global rankings. The 27 matched countries are each proud nations. There are surprises throughout this listing. UAE 33rd largest country? Romania 34th largest? Morocco 56th largest? Qatar 60th largest? Dominican Republic 62nd largest? New Zealand 63rd largest?

Even bigger surprises arise from the pairing of US states to their global equivalents. Raise your hand if you predicted that these US states are the economic equals of their global nation partners: Georgia and Switzerland, Massachusetts and Sweden, Virginia and Ireland, Maryland and Ukraine, Arizona and Portugal, Indiana and Denmark, Minnesota and Norway, Missouri and Greece, New Jersey and Singapore, Alabama and New Zealand.

The remaining 18 US states are not so large. Their combined GDP is about the same as our neighbor Canada, which ranks 15th overall by GDP, about the same size as Spain or Texas.

On the other hand, the US soccer team was ranked 11th globally. Three of the top 5 matching countries of Argentina, France and Spain deliver 1st, 2nd and 8th FIFA ratings. The middle 27 states matching nations provide another 8 world-class soccer teams in Belgium (3), Portugal (6), Morocco (13), Switzerland (19), Denmark (21), Ukraine (22), Austria (25) and Sweden (27).

The US is an economic colossus that continues to grow faster than the rest of the “developed countries” and maintains its global economic lead. We don’t normally think of Tennessee, Colorado, Michigan, Arizona, Indiana, Minnesota, Maryland and Missouri as global economic powerhouses, but they would EACH rank in the top 55 countries of the world as standalone economies.

Human progress is based on 4 things, IMHO. We are able to abstract and generalize. We accumulate our lessons learned. We innovate. We combine our structured, accumulated knowledge with innovations. Creativity and innovation get most of the attention. Yet, the accumulation of our practical and theoretical experience in language, books, records and equations may be equally important. The ability to switch “back and forth” between a fixed structure, history, religion and culture and new innovations may be the most important aspect of all. We have divergent and convergent thinking abilities. We use inductive and deductive reasoning. We intuitively prefer “either/or” but can manage “both/and” logic. The modern history of mankind’s progress points towards the importance of creativity and “both/and” logic.

Abstraction is a relatively recent phenomenon. Democritus imagined atoms, smaller and smaller particles. Heraclitus imagined all as change. The Greeks imagined earth, water, air, and fire beneath everything. Pythagoras and Euclid provided geometric proofs and ideal figures. Aristotle offered a powerful version of formal logic. Plato defined the “forms” and the ideal realm that stands above our experienced reality. Descartes defined mind versus body and the Cartesian coordinate system. Newton rationalized the universe in terms of algebraically defined laws. Kant defined pure logic and the limits to pure logic. The great appeal of abstract rules and an implicit mechanical universe remains to this day. The “Enlightenment” produced new politics, economics, culture, science and religion based upon these powerful insights.

The accumulation of knowledge has occurred in a surprisingly wide variety of forms. Life in DNA. Sexual reproduction. Man’s biological memory. Human consciousness. Spoken language. Music. Myths. Written language. Culture. Laws. Accounting systems and records. Religious practices. Architecture. Books. Libraries. Scribes. Printing. Histories. Universities. Experimental science. Prophets. Peer-reviewed journals. Scientific societies. Mass media. Recordings. Radio. Video. Internet. Wikipedia. Zoom.

The history of innovation is well known. I want to highlight the general trend away from simple, atomistic, “either/or”, static views to more complex, multi-level, “both/and”, dynamic, organic views that provide much better insights into our real experience.

Physics has moved from statics to dynamics. Classical mechanics has been replaced by complex, probabilistic quantum mechanics. The fixed, static, deterministic perspective has been replaced by Einstein’s relativity. In general, deterministic views are replaced by probabilistic views. The solid atoms have been replaced by waves and fields. Light exhibits both wave and particle behaviors. Heisenberg says we cannot measure everything. The background framework of an “ether” is no longer required. The mathematics required to describe physics has moved from algebra to multi-variate calculus to string theory. Only a handful of people truly understand the frontiers of physics in the last 100 years.

Mathematics has advanced wonderfully in the last 500 years. Newton and Leibniz invented the calculus. Man could now measure, describe, imagine and control changes through time. There is an equation underlying all activities that can, in theory, predict the future and explain the past. Dynamics can be described. Three-dimensional Euclidean geometry was superseded by multiple-dimensional geometry, Riemann curved space and fractals. Probability theory was developed to clearly describe apparently random activities, providing a solid basis for evaluating the results of experiments. Set theory evolved to encompass all of mathematics and logic, including various conceptions of infinities. Goedel’s 1931 “incompleteness theorem” undercut Russel’s attempt to define a single, bottoms-up, certain, powerful mathematics.

Biology evolved from collecting, illustrating and categorizing specimens to Lamarck’s deterministic evolution to Darwin’s evolutionary survival of the fittest perspective. Society increasingly adopted a biological, process, systems theory perspective in place of a physics, mechanical, materialistic perspective. Nature versus nurture became nature and nurture. The details of genetics is better understood as a very complex process involving multiple genes and other structures.

In philosophy, Hegel defined his dynamic thesis, antithesis, synthesis model. History now ruled. Eternal universals were much less likely. Multiple perspectives were elevated. Certainty was less likely. Marx tried to use Hegel’s general framework combined with an economic, materialist determinism but he failed.

In practical technology, we have seen the rapid accumulation of knowledge. We have also witnessed the great importance of “both/and” solutions. For example, ships and automobiles required the invention of a clutch that provided both solid propulsion and slippage. Powered vehicles first required rails but were turned loose as motor carriages. Wheels evolved from steel to rubber to accommodate shocks, turns and rough roads. Vehicles added suspension systems.

In economics, we advanced from mercantilism to comparative advantage and free trade. We left behind land, labor or capital as the only sources of value with the insights of the marginal productivity economists. We moved from static to dynamic perspectives and focused on the determinants of growth in advanced and developing nations. Keynes demonstrated that national economies were more than the sum of individual markets and that self-regulating equilibriums were not inherent in a market system.

Computer systems have evolved from fully defined linear and logical systems to massively parallel systems capable of artificial intelligence and spoken interaction with humans.

Businesses have replaced assembly lines and Taylor’s experiments with a deeper understanding of individual tasks in probability terms and the sequence of events in any process. Firms have embraced Japanese style process management and improvement, delivering constantly improving results. Supply chains span the globe. Project management is now “agile”. Strategic planning is no longer deterministic, but focused on mission, vision, values, strengths, weaknesses, opportunities, threats and culture. Investments are considered within the framework of portfolios of risks and returns. Entrepreneurs and leaders are valued above technical and professional experts.

For many, religion has evolved from a legal, literal, deterministic perspective to one that emphasizes the principles, insights, opportunities, feelings, experiences and possibilities of a given creed, despite the loss of absolute certainty in a “Secular Age”.

As humans we prefer a simpler, more deterministic view of the world. Yet the world shows us that it is more complex and that we will never fully understand it.

Real, after inflation, Gross Domestic Product is up by one-third, despite the pandemic. That’s 2% annually, despite the Great Recession and the pandemic. The US economy is very solid.

A 21% increase in per capita income during this time. Quite solid and constant growth.

Inflation averaged a bit less than 2% before the pandemic, spiked to 8%, and has since declined to 4%. Experts disagree on whether it will return to 2% soon.

Gas prices are the most obvious component of inflation. They are largely driven by global supply and demand. Prices today are the same as in 2011-14, despite the general inflation increase of more than 20% since then.

Despite the pandemic, US unemployment is at a 50 year low!

Job seekers today encounter 3 times as many job openings.

Core age labor force participation has snapped back after the pandemic.

Investment values have doubled.

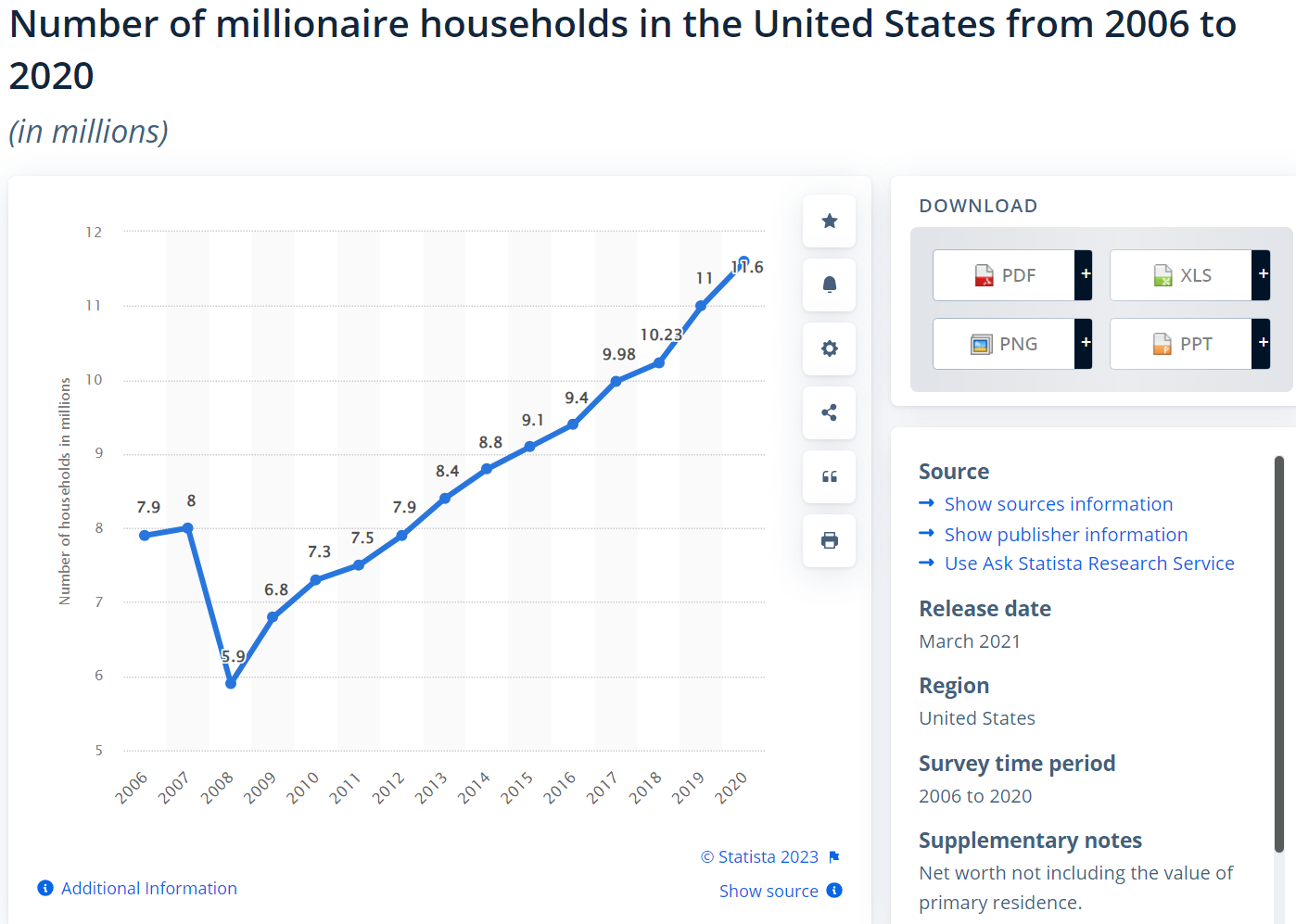

The number of millionaires and billionaires in the US has continued to increase.

Personal savings rates rose from 6% to 9% before the pandemic, shot up and fell back down to just 4% recently.

Housing values have doubled since the Great Recession.

Mortgage rates averaged 4% after the Great Recession, dropped to 3% and then increased to 6%+ as the Federal Reserve raised interest rates.

US exports have nearly doubled in 14 years.

Despite the Trump tariffs, which Biden has maintained, imports have also nearly doubled.

Despite historically slower growth rates, higher budget deficits and looser monetary policies, the US dollar is more highly valued today than in 2008.

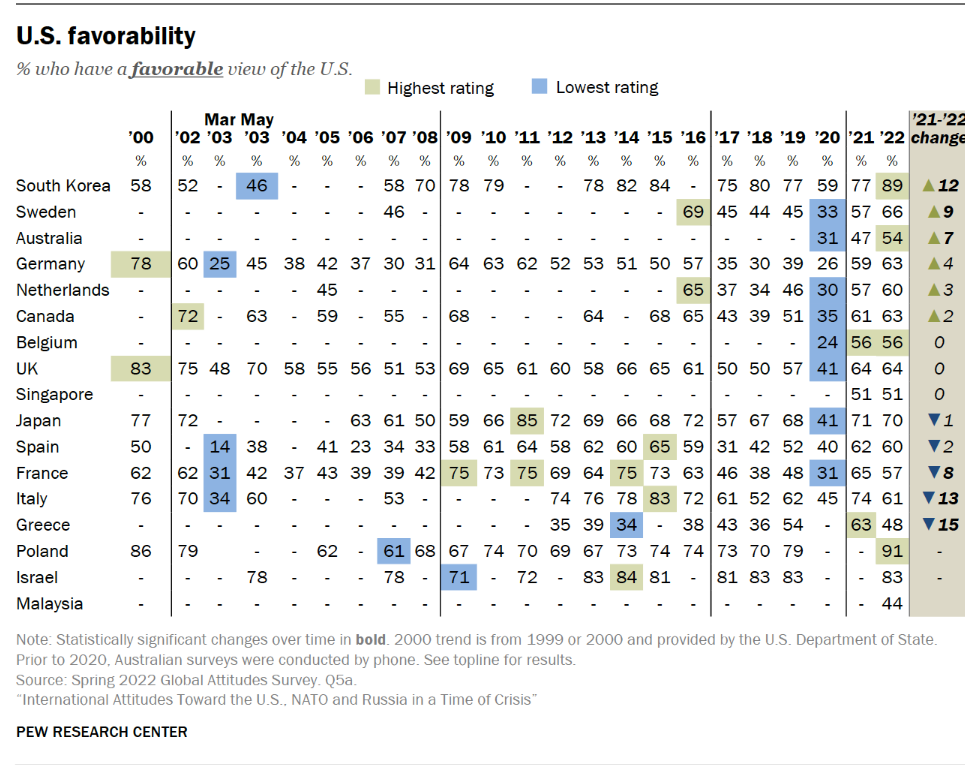

Foreign countries still see the US as a positive ally, despite their concerns during the Trump era.

Obama returned the budget deficit to a “reasonable” 3% by 2016. Trump expanded it to 5% and then 15% as the pandemic struck. Biden drove some recovery to 5% by 2022, but has not driven further reductions.

US coal production is in a long-term decline.

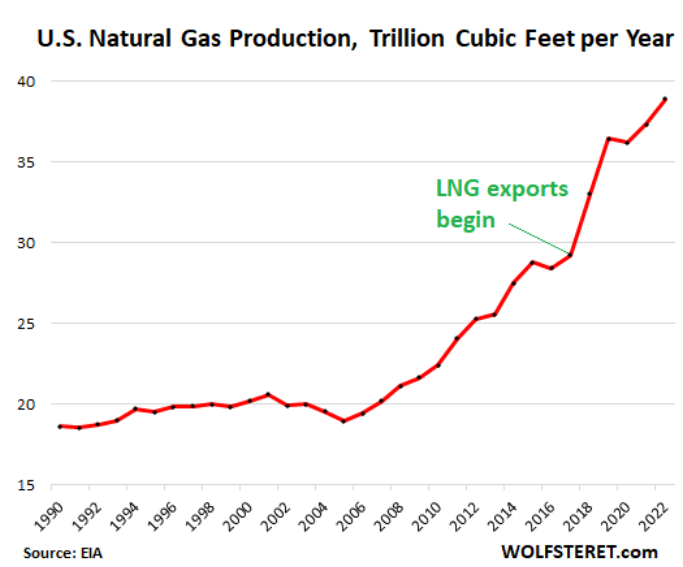

Natural gas production has nearly doubled in 14 years.

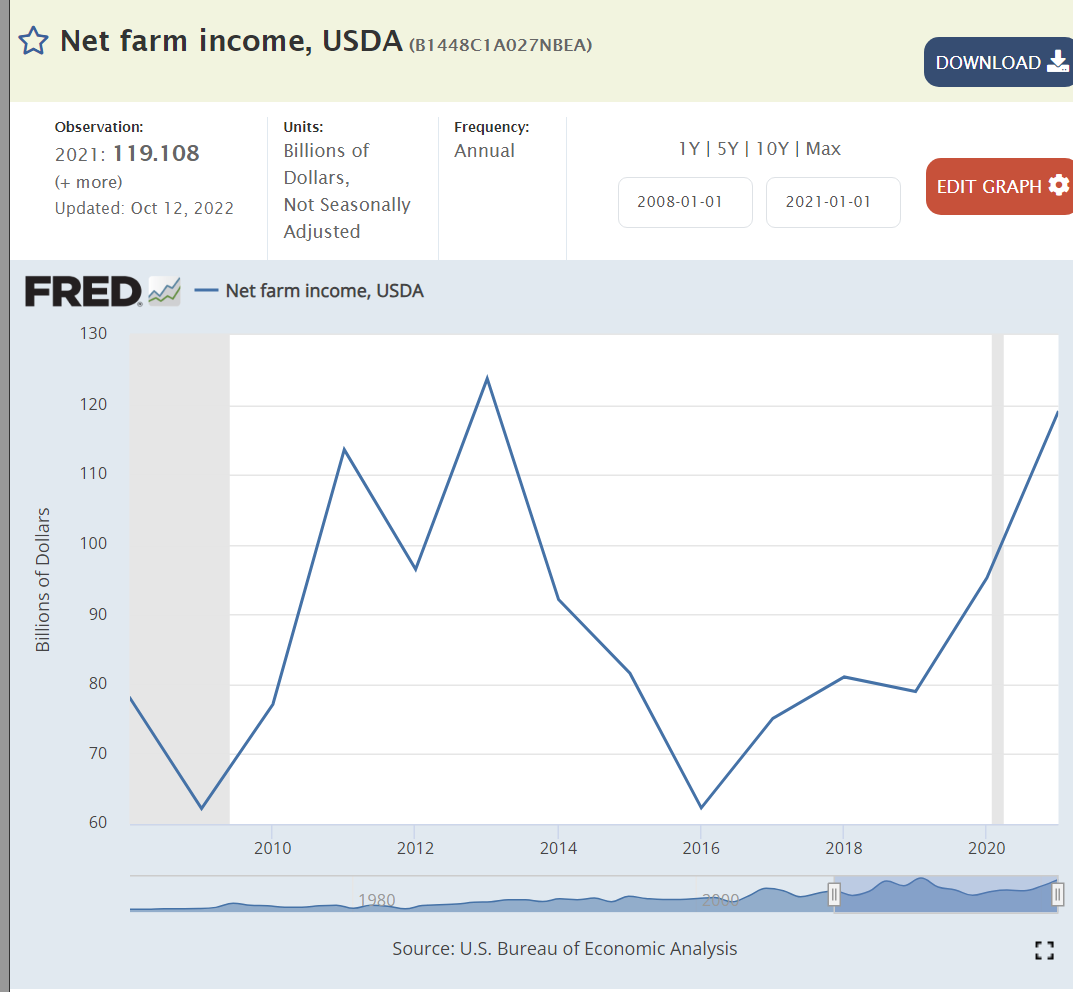

Net farm income has been significantly above the base for 6 of the last 14 years, despite lavish Trump farm subsidies.

Manufacturing employment has continued to rise slowly in the last 14 years against the headwinds of international competition.

It’s difficult to put the pandemic in perspective, but here we see a 2-year reduction in expected lifespans. Opioid deaths and so-called “deaths of despair”, alcohol, drugs, suicide, also play a role.

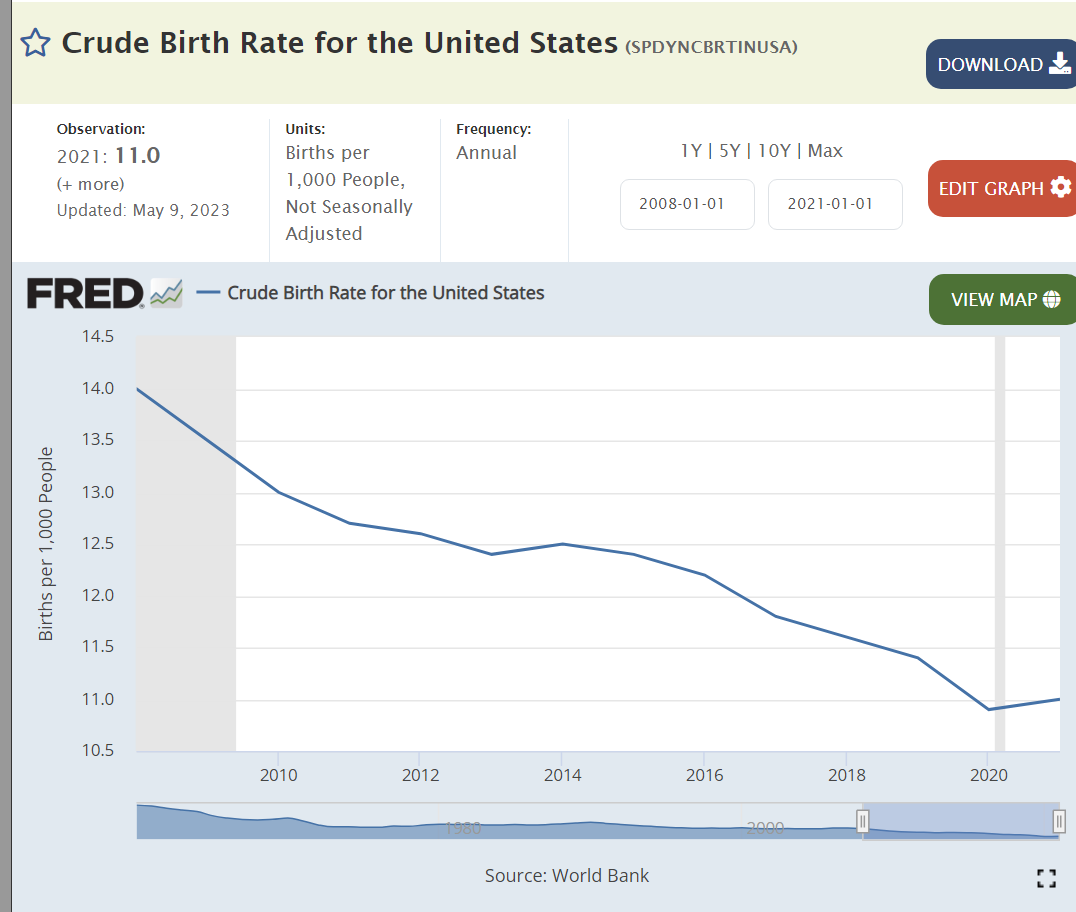

Birth rates continue to drift lower as seen in all regions of the world.

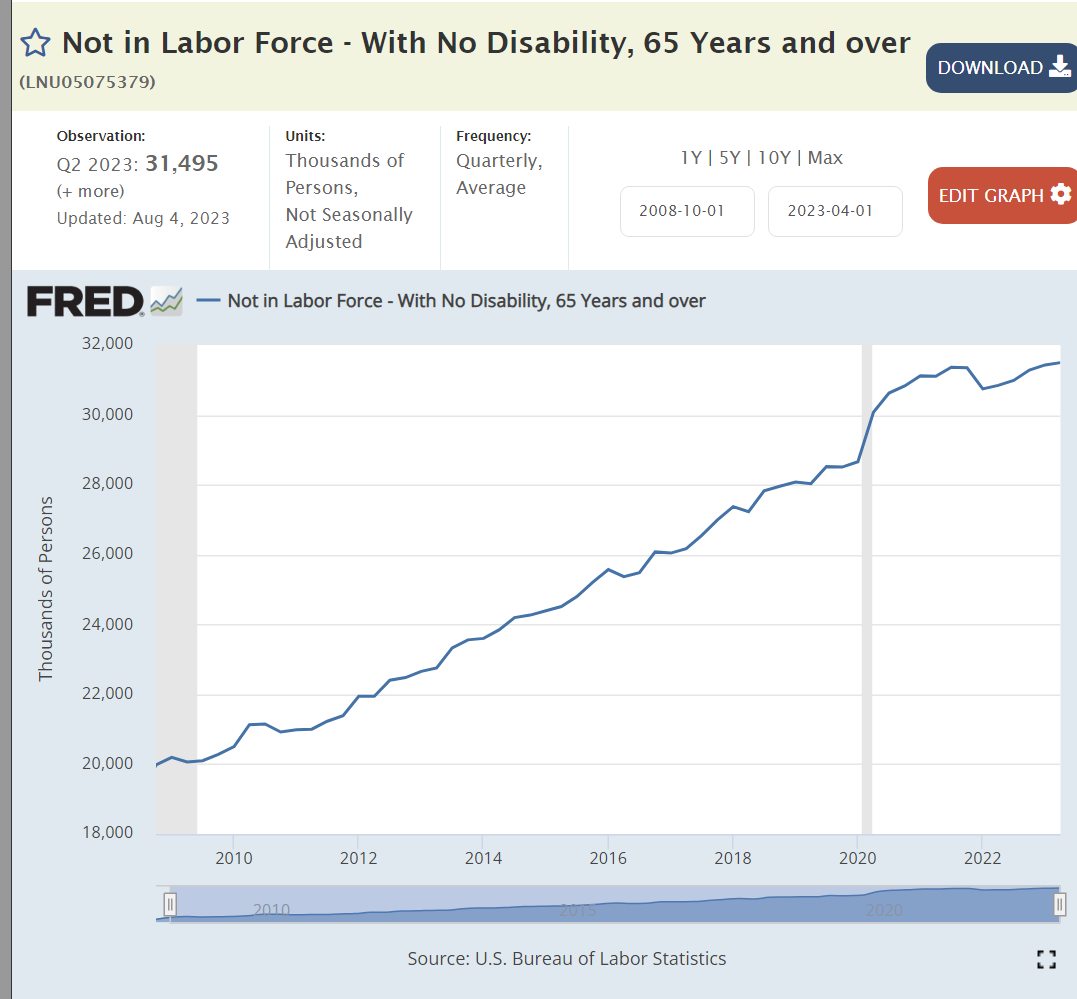

The number of retirees has increased by more than 50%.

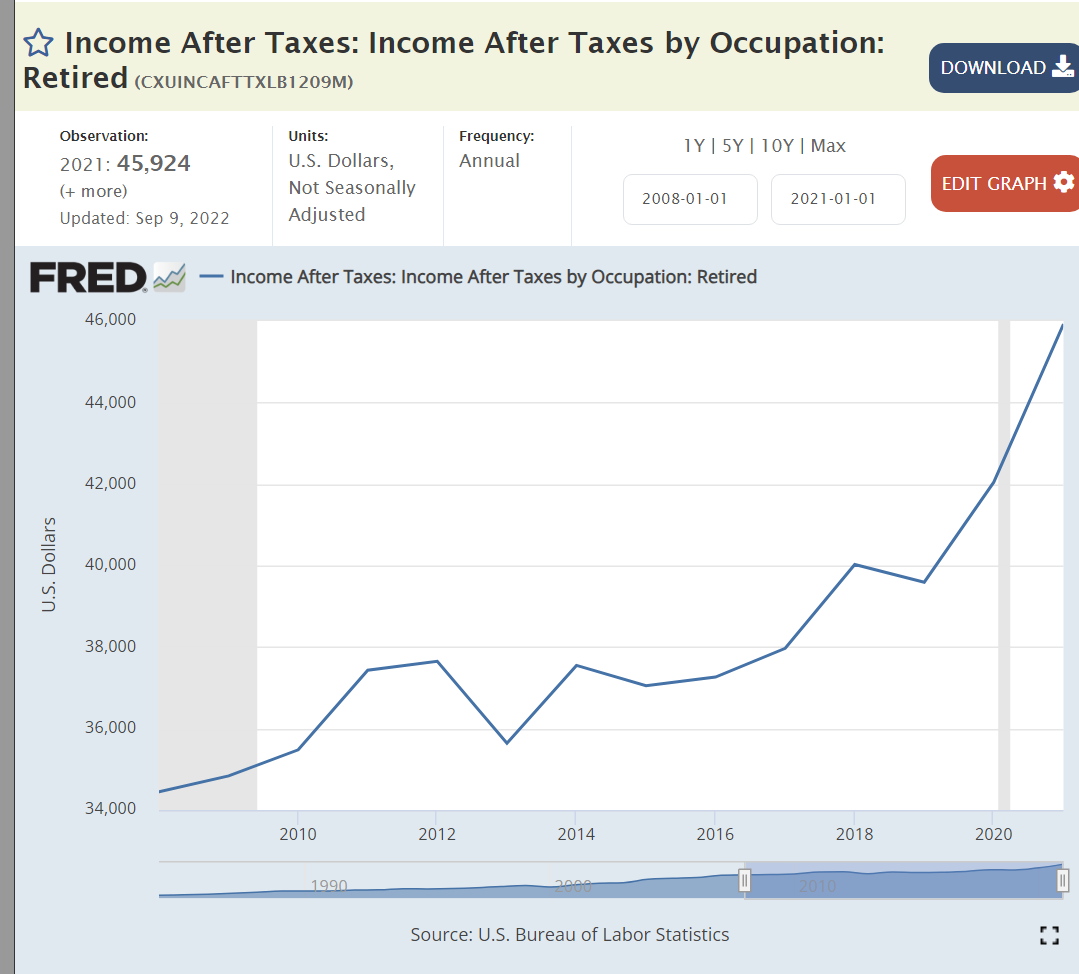

Retiree incomes are up by one-third, matching inflation.

Prospective retirees have doubled their cumulative savings.

The abortion rate has continued to fall in the last 30 years.

Church attendance has dropped from 40% to 30%.

Summary

The US economy recovered slowly after the Great Recession and then very quickly after the pandemic. Real, after inflation, output and per capita output increased. The labor market became very tight. Asset prices (investments and housing) rose for intrinsic and monetary reasons. The US remained a competitive international producer. The federal budget deficit was better at the end of the Obama period but worse for Trump and Biden. The pandemic reduced life expectancy and households had fewer children. Successful retirements grew and will grow. Social trends continue, uninterrupted by political positioning and policies.

Perceptions of the country and the economy are increasingly shaped by partisan political party views. Nonetheless, the US economy continues to grow and thrive.