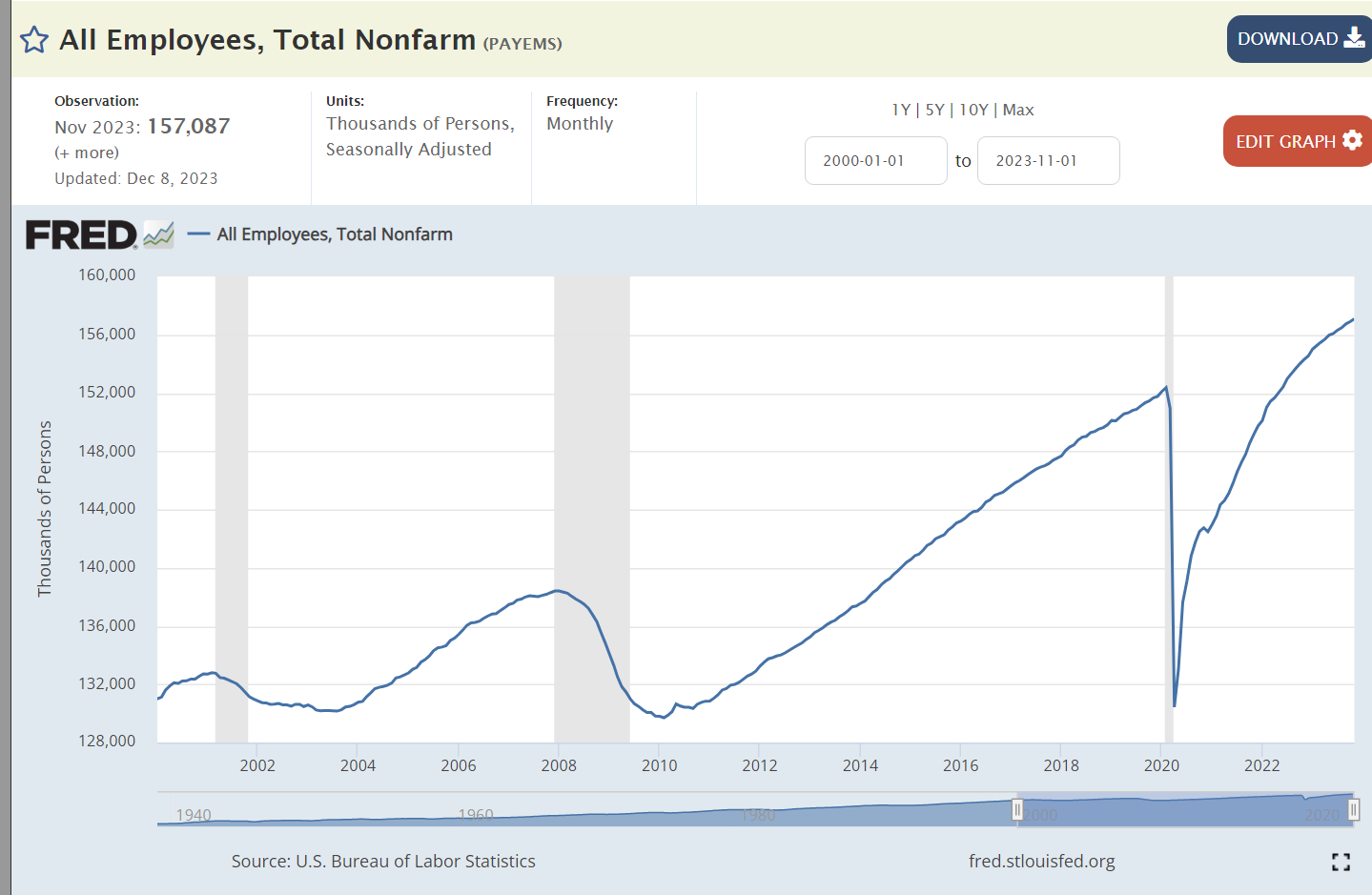

Economists prefer to measure data at business cycle peaks and troughs. After the Millenium Y2K scare, we endured a mini recession. Employment peaked at 132.8 million jobs in March, 2001. Today, in October, 2023, we have 156.9 million jobs, an increase of 24 million jobs in 22 1/2 years, almost 1.1 million new jobs created each year! This is despite the job destroying effects of the Great Recession and the Pandemic.

The longest business expansion in US history ended after 10 years in February, 2020. The pandemic eliminated almost 22 million jobs in 2 months, leaving the economy with just 130.4 million employed, barely above the trough of 129.7 million in February, 2010.

The economy replaced those jobs in just 26 months when the June, 2022 figures were reported! In addition to replacing the first 22 million jobs, the economy has added another 4.5 million jobs in the last 16 months, averaging 280,000 per month or 3.4 million per year! At the same period after the Y2K recession, the economy averaged 2.6 million new jobs per year. At the same period after the Great Recession, the economy averaged 2.8 million new jobs per year. Our economy averages 1 million new jobs per year and can accelerate to 3 million per year when recovering from a recession. The current recovery is stronger than either of the last two.

Another way to gauge progress is to measure jobs added from peak to peak. The economy added 5.6 million net new jobs by December, 2007, or 836K per year. In the 13 years until February, 2020 the economy added 22.7 million jobs, or 1.141M per year. Since then, the economy has added 4.5 million jobs, or 1.240 per year, a very solid result.

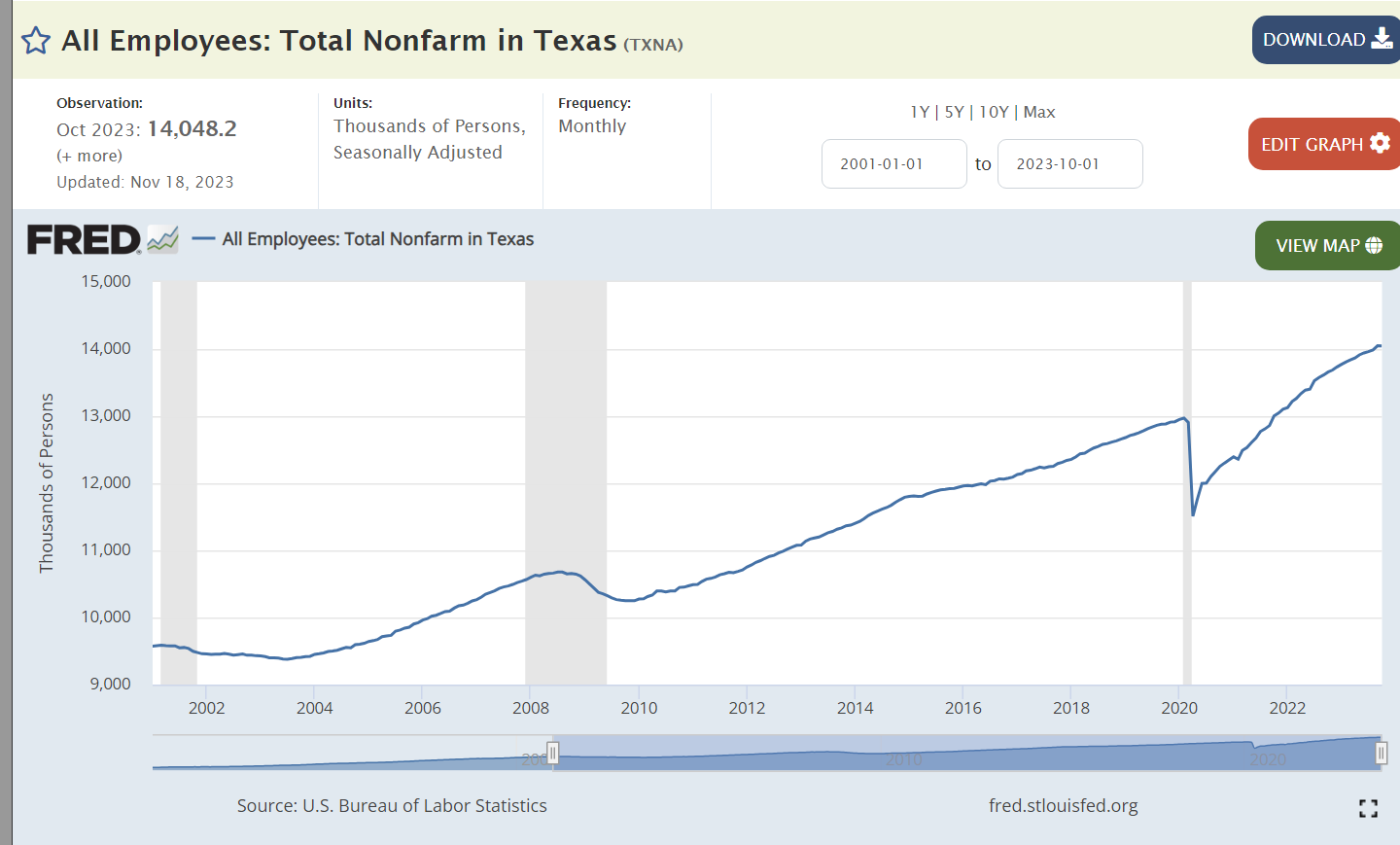

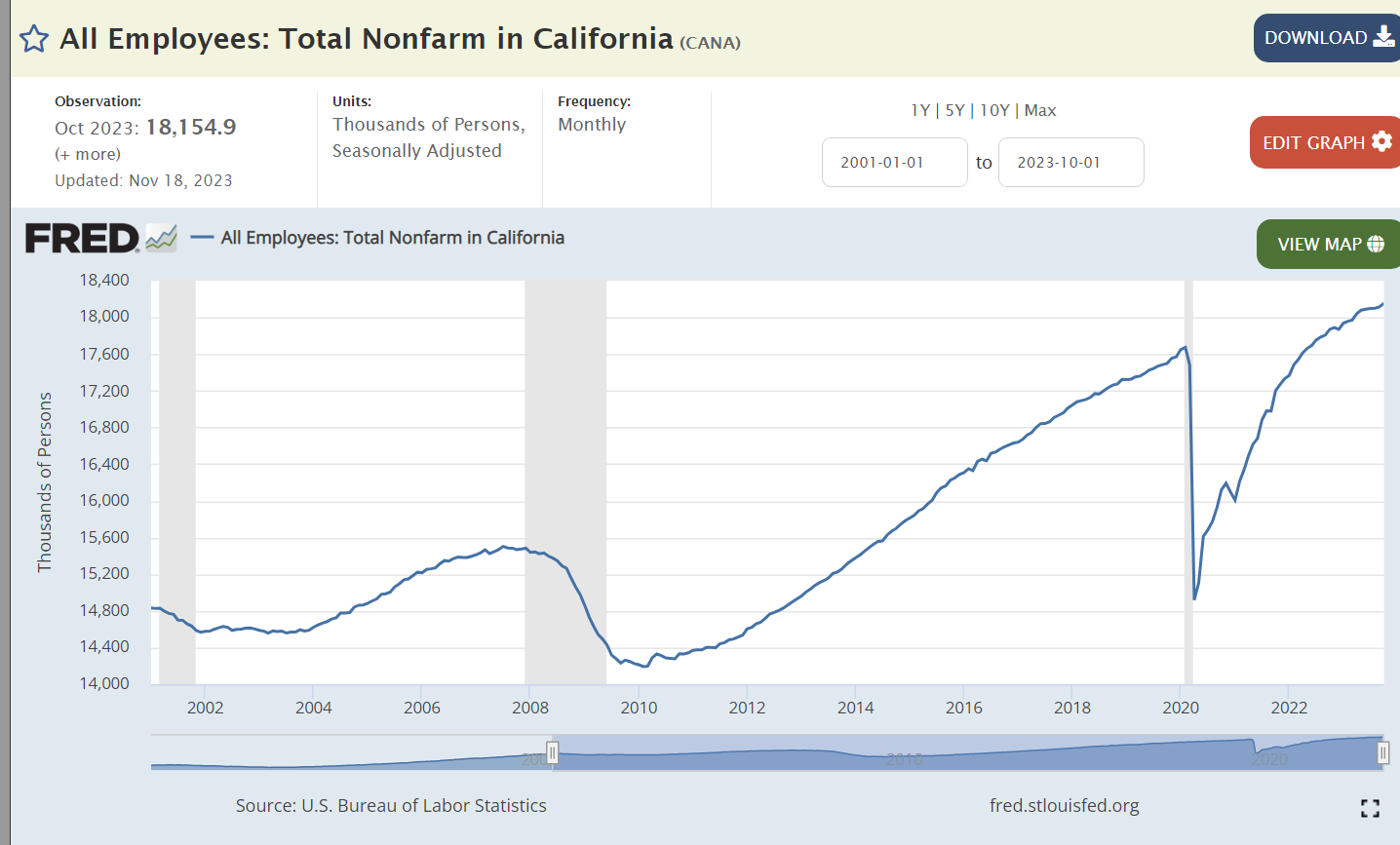

Where are the extra 4.5 million jobs? 38 states exceed their pre-Pandemic totals. Texas (1.1M), Florida (750K), California (500K), North Carolina (300K) and Georgia (250K) lead the way. Arizona, Utah, Tennessee, Nevada, South Carolina, Washington, New Jersey and Indiana each added at least 100K, for a total of 4 million by these 13 states. On the downside, New York remains 125K short and Vermont, DC, Hawaii and Rhode Island are more than 2% below February, 2020.

The post-pandemic economy is creating jobs slightly faster than the post-Great Recession economy. 17 states are growing at least 2% faster than their pre-Pandemic trend rate. Idaho, Nevada, Montana, Utah and Florida are growing at least 4% faster than before. 9 states trail their prior growth rates by at least 2%. North Dakota, Hawaii, New York and DC trail their prior growth rates by 4% or more, for various reasons.

During the full 23 years, Texas (4.5M), California (3.3M), Florida (2.7M), New York (1.1M) and North Carolina (1.0M) added the most jobs. Washington, Nevada, Arizona, Utah, Colorado, Tennessee, Georgia and Virginia each added more than one-half million, for a total of 18 million in the 13 leading states. While the nation added 18% more jobs during this period, 9 states grew by 3% or less: Louisiana, Mississippi, Illinois, Michigan, Ohio, West Virginia, Rhode Island, Connecticut and Vermont. These states accounted for more than one in six citizens in 2001, so their weak performances limited the overall economy.

Summary

The economy started the 21st century slowly with a small recession and weak jobs growth during the Bush years. Obama started his first 2 years with a 9 million job deficit before starting a very strong and long 10-year recovery that added 23 million jobs. Economists did not expect the recovery to last during the Trump administration but almost 9 million net jobs were added on his watch before the pandemic. Biden refilled the 22 million lost jobs in 26 months and has added 4.5 million more in the next 16 months. With the Fed’s higher interest rates, job growth is slowing but is generally expected to exceed 1.25 million in 2024. The US economy continues to outperform.

https://www.bls.gov/web/laus/statewide_otm_oty_change.htm

https://www.cbpp.org/research/economy/tracking-the-recovery-from-the-pandemic-recession

https://www.morningstar.com/markets/why-we-expect-job-market-slow-2024