Nice variety of rail trails, state and county parks, nature preserves, a quarry and an arboretum. This is mostly flat walking. St. Joseph County offers many options.

A village, a historic canal, a deep valley and a rail trail provide options in Delphi, along the Wabash. The bridge is under reconstruction, but you can hike up to one end and you can hike beneath it in the valley.

Travelers have come to know and love the outdoor recreational facilities of France Park, with scenic trails, beautiful waterfall, clear swimming lake with picturesque cliffs, quiet fishing areas, and spacious camping facilities.

The Nickel Plate Trail runs from Kokomo to Rochester. There are a dozen trailheads along its 40 mile length. Although mostly flat, this is a surprisingly scenic trail where it crosses 3 major rivers and approaches Lake Manitou south of Rochester.

The prairie and stream trails are enjoyable. The Gabis arboretum resources and gardens are nice. But the highlight is the outdoor model train and landscaping.

Potato Creek is west of South Bend. The trails take advantage of a lake, historical and planted areas. The state is investing in this park for the future.

The Erie Trail is a straight 20 mile rail-trail segment of the American Discovery Trail, starting north of the Tippecanoe River SP and heading WNW to North Judson, IN.

Located out of the way, near the headlands of the Wabash, this state park is more developed than expected, with a dammed lake, pine woods and bison area.

Paris, KY will transform you back in time. The architecture downtown and on the nearby streets is mind boggling for a small town in the middle of nowhere.

40 miles southeast of Cincinnati, the earth is hilly, up and down, like Tuscany. This lake is nestled in this unique area. The 2 hiking trails are “so so”, but the drive to this location and the lake view are strong.

This hike is in the city, just south of Cincinnati high on a hill. It follows a stream. The local cross-country team boasts of their KY championships. It’s easy to see why they win with such a nice trail.

Lexington and the surrounding 30 miles begs for slow car trips and walking. Think James Bond and Goldfinger. The city provides many paved trails. This one to the south, offers gardens, streams and monuments. To the north, the ponies.

The drive to this location up, down and around is amazing. The nature preserve is full of animals and a couple of cedar groves … and an amazing stone fence. Look for it.

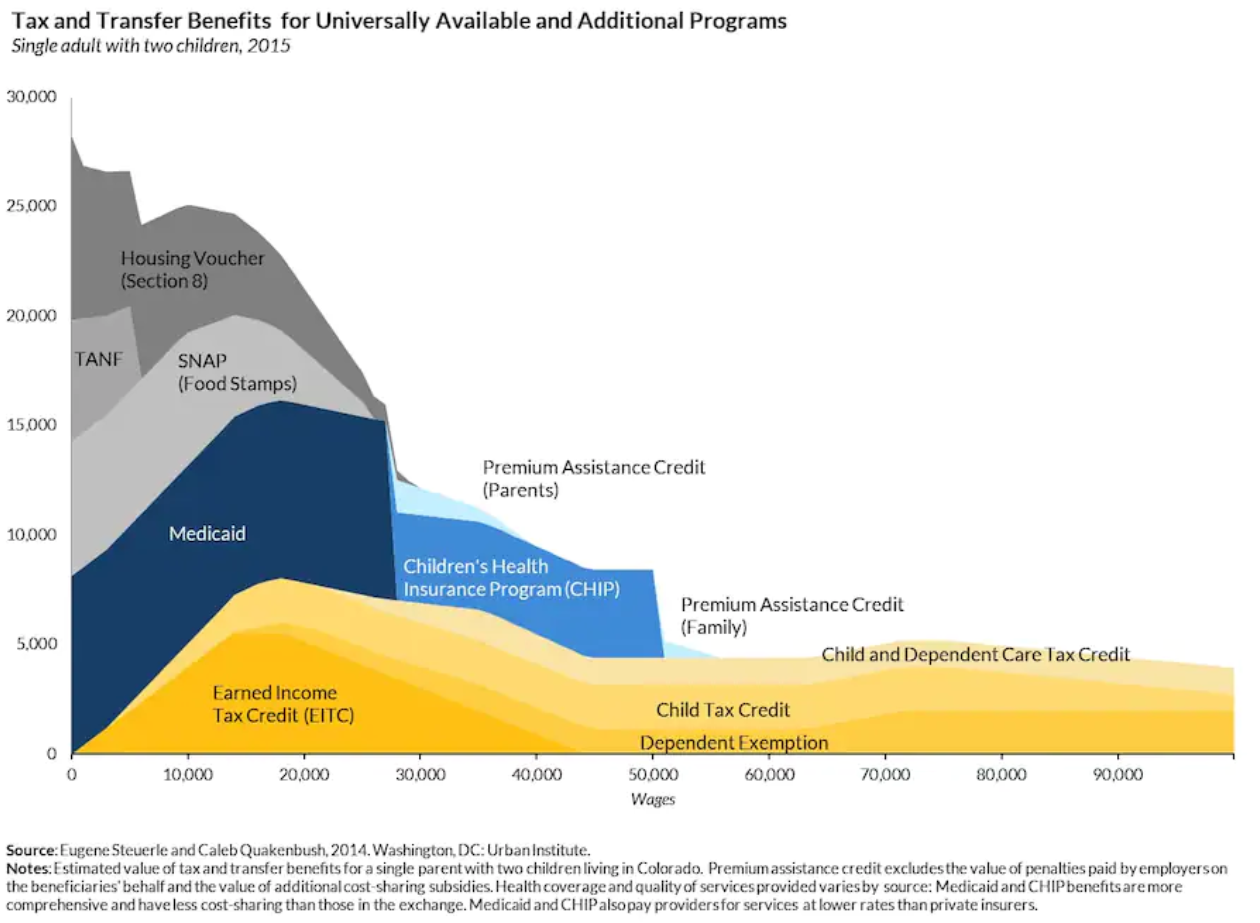

“Typical welfare family”, a single parent and 2 children (cue the video), receives $35,000 of welfare benefits annually claims the Wisconsin congressman in 2014. That number has stuck in our minds, just like the “welfare queen” and escaped prisoner “Willie Horton”.

Fact checkers debunked this claim, but it’s important to work through the details to get back to a reasonable “order of magnitude” estimate of “welfare benefits”.

If a family has ZERO income, they may receive maximum benefits. The Clinton “welfare reforms” limited the primary benefits to a total of 60 months. Families cannot receive benefits “forever”. Most household heads do work and have some income during the year. The maximum benefit number is an inappropriate “anchor”.

Temporary Assistance for Needy Families (TANF) (welfare) participation rates have fallen from 80% of those eligible to less than 25% since “reform” was implemented. The reform has had it’s intended effect. Two-thirds of those previously participating no longer do so. Some have become more productive and income earning members of society. Others “make do”.

Current average TANF benefits in my home state of Indiana are $346/month or $4,152. That’s a long way from $35,000 of cash benefits, which is the “anchor” that needs to be removed. $4,000 per year of cash is the typical Indiana welfare benefit. The maximum is $700/month or $8,400/year, twice as high. More kids, no income, still eligible. This is possible, but it’s not a useful reference point. The normal received benefit is just one-half of the maximum.

Supplemental Nutritional Assistance Program (SNAP of food stamps) is the next welfare program. For an Indiana family of 3, current benefit value is $6,240 per year. A family of 3 can earn up to $25,000 annually before benefits start to decline. The national ratio of SNAP to TANF recipients is 82%. In Indiana, just 75% of those eligible receive ANY SNAP benefits.

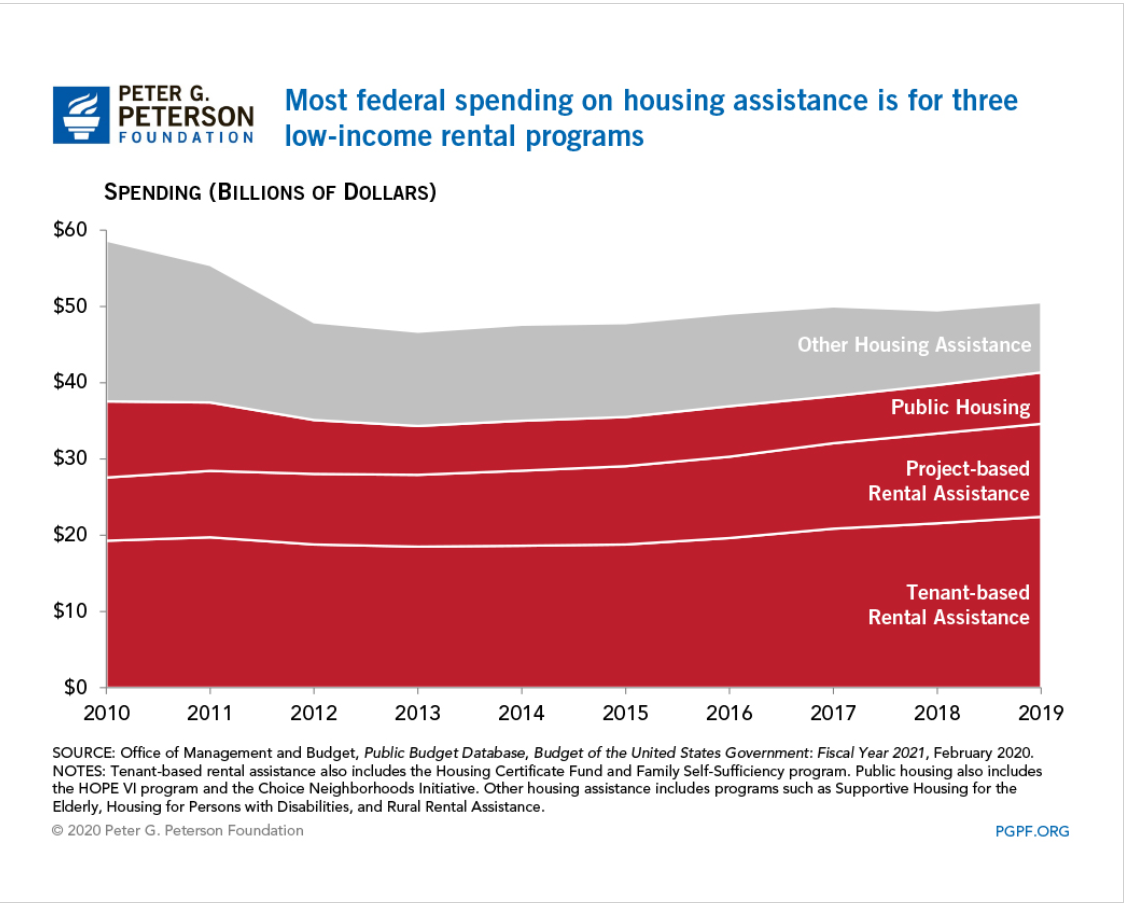

Housing assistance is listed at $9,000. There are various federal and state programs. This is like “winning the lottery” for low income families. In Indiana, 1 in 8 eligible families (12%) receive housing subsidies. These average $736/month or $8,832 per year. On an “expected value” basis, this is only $1,060 per year. From a public policy point of view, this is the relevant number.

In the Wisconsin representative’s model, there is $7,000 of higher education benefits. This is clearly irrelevant to public policy. Individuals do not make ongoing annual work choices based on education benefits.

The Cato Institute started this “conversation” about “welfare versus work” in 1995 and updated their analysis in 2013.

Like the congressman, they note that the “welfare benefits” received are in “after-tax” dollars, so they “should” be translated back into pre-tax dollars to be “fair”. Since the marginal tax rate for low-income wage earners is often just 10%, this is immaterial. More importantly, the emotional, political currency is cash. “how much do THEY receive?” is THE question. This is an after-tax amount. No “grossing up” is required.

The Cato folks also include the full value of Medicaid benefits received by those below the eligible income transition. The value paid per child ($2,145) and per adult ($4,211) yields an $8,501 annual “benefit” currently. Is this a “welfare” benefit or a “citizen” benefit? The US health care system is primarily funded through tax-deductible employer plans. Medical plan subsidies are now available up to 400% of the federal poverty level. From a federal budget perspective, lowest income families receive more value. From an “incentive” perspective, low income families are generally indifferent between federal and employer sponsored plans. This $9,000 does not belong in “the cost of welfare”.

The Cato analysis includes the cost of the “earned income tax credit” (EITC) as a welfare benefit. The EITC was created and enhanced as an incentive for unemployed persons to work and earn some income, thereby providing themselves with short-term and long-term benefits and reducing the cash level welfare benefits. It grows quickly with earned income up to about $18,000 and then falls back down nearly as quickly as income grows to $40,000 per year. This is not what most people think of as a “welfare benefit”.

The Cato analysis also focuses on welfare benefits versus the minimum wage, emphasizing that overly generous welfare benefits provide a disincentive for recipients to seek paid employment (ignoring the 60 month TANF benefits limit). As the effective minimum wage in 2021 approaches $15/hour and $31,200/year, we won’t be hearing this comparison again.

As a professional “cost accountant” since 1978, I was often asked to provide the “exact cost” of various products or services. College courses, residence hall rooms, food service meals, buildings for rent, account managers, computer hardware, installed cables, telephone services, computer maintenance, software development, dresses, tops, retail stores, extension cords, surge protectors, imported goods, cell phones, returned cell phones, etc. The answer is always “it depends”. This is never a popular answer. It depends on what decision you are making. Short-term, medium-term or long-term timeframe. Do we include opportunity costs? Which externalities should we consider, if any? Do we include strategic, brand or cultural consistency as factors?

For the “welfare benefits” question, I think that the relevant public policy/budget and personal incentive numbers are largely the same. Welfare/TANF and food stamps/SNAP matter. EITC, medicaid, education benefits, housing assistance, and income taxes don’t matter.

Welfare/TANF for an Indiana family of 3 is worth $4,152 annually. The complementary food stamp/SNAP benefits are worth $6,240. The total quasi-cash welfare payment is $10,392 per year of eligibility. Maximum of 5 years. This is the right “anchoring” number: $10,000 per year for a family of 3. They will be going to the local food pantry every week. They will be seeking family and private charity. They will be leaning on friends, relatives and neighbors for “subsidized” child care. They will be working and seeking to advance themselves.

There are disincentive challenges remaining in our current systems.

But, these technical, marginal, incremental, opportunity rates are not the heart of the matter. Lower income families are not “optimizing” their benefits. I volunteered to provide low income/elderly federal income tax services for several years. The benefit and tax rules are complex beyond comprehension.

The core public policy question is “Is $10,000 of annual benefits a reasonable amount for our state to pay to a family of 3 with no income?”. I would argue that it is too low, half what it ought to be.

Support for a universal basic income (UBI) has grown in recent years, as the economy, productivity and equity returns have grown by 3% annually but wages have remained flat for 40-50 years in the US.

Lots of press on the topic of a “new” labor market. Some of the experience seems to be genuinely new, some of the situation seems to be our old favorites, supply and demand.

Derek Thomson’s recent Atlantic article is a good one,

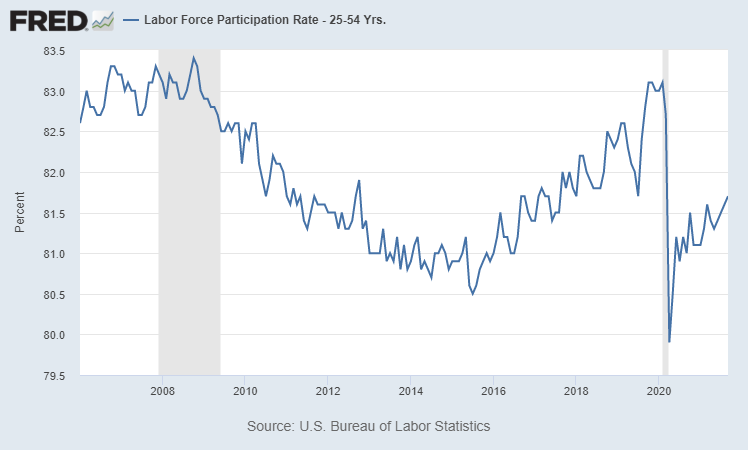

On the supply side, labor force participation is the big driver.

Focus on the core 25-54 age group to avoid the impact of various “mix variances” with changing enrollment rates and different retirement patterns. HUGE increase from 1950 to 1990, 65% to 84%, as women joined the US workforce across 4 decades. The rate stayed roughly constant for 2 more decades, through 2010, falling back a little to 83% in the late 2010’s.

Since 2006, we’ve had some modest changes. The rate fell from the relatively stable 83% rate through 2009 down to 81% in 2012. The recession knocked 2% of the population out of the workforce. For the next 4 years, through 2016, the participation rate remained at 81%. This is a variable that does not change quickly. People make long-term decisions, knowing that re-entering the work force requires very significant “effort”, investments, networking and accepting lower wages versus history. By the middle of 2016, almost 8 years after the decline that started in early 2009, the participation rate started to increase again. Note the many articles about the “jobless recovery” during W Bush’s time and Obama’s first term. The labor markets are not quite as responsive as desired. In the next 4 years, the participation rate returned to its prior level. That’s an increase of 0.5% per year during a prolonged economic boom period. Again, this measure of available supply does not change rapidly in normal times.

The pandemic dropped participation back to 81% in a short few months! In the last year, the participation rate has risen by a little more than 0.5% to 81.7%. We can expect to see this same kind of improvement for each of the next 3 years based upon recent history. But, even with all of the measures of underemployment and open positions, it is unlikely that the labor market will attract new employees faster than this rate.

The number of nonfarm workers employed reflects the results of labor markets. This is another measure that typically changes slowly.

The number of US employees stayed relatively flat from 2000-2004. The W Bush (jobless) recovery DID add 6 million workers. The “Great Recession” dropped the headcount by 8 million, back down to the 130 million level of the prior recession. Note that we had 11 years with essentially ZERO net job growth.

The economy found its footing in 2010 and we had 9 years or growth, adding 22 million employees, a truly remarkable period of prosperity. This recovery is remarkable for the steady pace of job growth, a constant 2.4 million per year.

By the end of the 2020 pandemic year, employment was down to 143 million, a decline of 9 million. This is similar in size to the “Great Recession’s” 8 million job loss. In the last year, the economy has added 5 million jobs, a pace TWICE the level of the prior recovery. We may be slowing down, or the job adds may continue between the 2.4 – 5 million annual rate. This is VERY GOOD news.

In the long-run, the US economy struggles to reduce and hold unemployment below 5%.

In the post-WW II boom times, 4% was reached several times, but thereafter quickly increased back above 5%. The “stagflation” era of the 1970’s indicated that “full employment” might be as high as 6%. The boom periods of the late 1990’s and 2000’s drove actual unemployment below the presumed 5% unemployment rate, but always just briefly. The long and smooth 2010’s recovery broke the rules. Unemployment rates fell and fell down to an unexpected 3.5%.

By the end of 2020, the unemployment rate had dropped to a more reasonable 6.7% from the measured peak of 15%.

It has recovered by a very strong and quick 2% in the last year, reaching 4.8%. This is near the long-term level of “full employment”, where demanders must provide increasingly attractive offers to entice supply.

This recent disconnect between supply and demand is seen in the unusually high job openings rate.

From 2000-2014, the economy averaged a 3% rate of job openings to labor market participants. About 1 in 30 or 33 jobs were “open”. The “Great Recession” drove this ratio as low as 2%, with just 1/50 jobs open. Following the “Great Recession” this ratio of job market demand increased for a full decade, from 2% to 4.5%, where only 1 in 22 jobs were open. Note that this is more than twice as many as in the depths of the “Great Recession”.

The job openings rate snapped back to the recent 4.5% level in the second half of 2020. It has since grown to a record 7%, or 1 in 14 positions unfilled. This is a “loose” labor market of historic proportions. Demand is clearly exceeding the slow response of supply in the labor force participation rate.

The “quits” rate has attracted the most media attention as it is even more extreme.

The voluntary quits rate averaged 2% from 2001-2008, 1 in 50 workers. It dropped to just 1.5% (1/66) during the Great Recession. It slowly increased with the recovery to 2.3% in the heady days of 2018-19 (1/44). The quit rate returned to its recent level very quickly by July, 2020. It has since increased to 2.8% or 1 in 36 workers each month. On an annual basis, this is 1 in 3 workers voluntarily leaving their employment!

As we’ve seen with the supply chain bottlenecks, the labor market is currently unable to recover quickly enough.

The economy did employ 152 million workers before the pandemic. We need 4 million more to reach that level. Based on recent history, this is an achievable level, but it will require 18 months or more to achieve.

In the mean time, employers will raise wages and provide more flexible terms to attract marginal workers back into employment.

As the “great resignation” pundits say, the pandemic experience changed the expectations of potential employees. They have found that they can “survive” rather than accept low wage positions with poor work conditions. This will change their behavior for years to come.

In 1970, GM owned a 39% market share in the US with its 6 brands. It now sells less than one-half at 19%. Ford sold 28% and now sells about one-half as much at 15%. Chrysler-Lincoln-Mercury-Jeep has done better, selling 12% in 2020 versus 15% in 1970.

In 1970 there were only 6 firms with 1% or greater market share. Today, there are 16 firms.

In 1970, the top 4 cornered the market with 88% market share. That has declined to 62%.

In the last 50 years, 11 new firms have earned 1% or greater market share. Consumer options are 3 times as great as in 1970!

A similar change has taken place for most manufactured goods. Legacy high cost American and European manufacturers have lost market share. Asian manufacturers have gained significantly (Japan, Korea, China, Taiwan, SE Asia, India). Latin American and African manufacturers have recently started to provide a fourth option.

For consumers, this is great news. More choices. More competitors. Lower prices. Improved products.

Compare the 2021 Honda Accord LX sedan with the 1970 Chevy Impala option to get a sense of the improved features available on a standard “family sedan” today versus 50 years ago.

State parks contain another 14 million acres. State parks had 807 million visitors in 2017, more than two and one-half times the national parks, despite their smaller areas. In total, that’s 1.1 million annual visits or 3.4 for each of the 330 million U.S. citizens. Between 1984 and 2017 attendance has increased by 30%.

My experience in Indiana, Ohio and Illinois indicates that the total “local” parks acreage is at least twice as great as this indicator. For example, 42 of Ohio’s 88 counties have a parks district.

There are an additional 56 million acres in voluntary land trust conservation areas. While these areas often have limited access and improvements, they served another 6 million visitors in 2015.

The total federal, state, local and private “parks” areas equals 161 million acres, nearly 7% of the total U.S. land area.

Federally managed forests contain 238 million acres and state forests contain 83 million acres. Most of these lands provide significant access for hiking, hunting and riding. At 321 million acres, they represent 13% of the total U.S. land area.