Since WW II, the US and the world have been on a tear, inventing at a pace never seen before. We have dozens of breakthroughs in basic science/materials, medicine/biotechnology, space, electronics, computers, networks, the internet and artificial intelligence. I’ve set aside advances in business processes and pure science, math, social sciences, philosophy and the humanities. I’m not addressing the potential costs and risks of a more technologically advanced civilization. I just want to briefly outline the major technical innovations of the last 75 years. I have grouped them into 3 buckets: traditional industries, medicine and computers.

The computer advances account for 54 of the 115 items, a little less than one-half. There are 21 hardware and network items, about one-sixth of the total (18%). Software broadly defined to include the internet and artificial intelligence sum to 33 items, a solid 3 out of 10 (29%). The 22 medical innovations represent roughly one-sixth of the total (19%). The 39 traditional, historical areas combine for one-third of the inventions.

I won’t describe the innovations in detail. I’ll append web links at the bottom which provide thumbnail sketches of this history and its importance. I expect that my readers know and use these innovations. I’m attempting to summarize then in order to provide perspective. The dominance of computer and communications advances is the biggest takeaway. I expect to see both incremental advances in each category and innovative combinations of computer software, communications, medicine and basic science in the next 25 years.

Agriculture

The green revolution, high yield varieties of rice and other crops

Electricity generation, turbines, batteries, electric motors.

Steam engine, turbine.

Internal combustion engine, automobile, tractor.

Railroad, locomotive.

Anesthesia.

Distilled oil products, diesel, kerosene and gasoline.

Telephone.

Circa 1900

Airplane

Automobile

Camera; digital camera

Electric light bulb; fluorescent, LCD, LED

Moving pictures

Phonograph

Radio

Refrigeration

Vaccines

Medical diagnostics: X-Ray; MRI, CT scan

Antibiotics, penicillin

Circa 1950

Electronic computer, Turing machine, personal computer; after arithmetical machines, abacus and slide rule.

Contraceptives

Geographical positioning system, (GPS) and mapping.

Vacuum tubes, integrated circuits, semiconductors and microprocessors.

Nuclear fission, fusion, power and bombs.

Television.

Circa 2000

Genetics, gene editing, DNA.

Mobile phone networks, infrastructure and personal devices.

Internet communications network.

World wide web addressing structure.

Artificial intelligence.

Smartphones.

Summary

The greatest technical innovations of humanity cover a broad range of life: food/cooking, construction, travel, transport, household, finance, science, power, medicine, entertainment and calculation.

We have a dozen major inventions in both of the 19th and 20th centuries. Change appears to be accelerating…

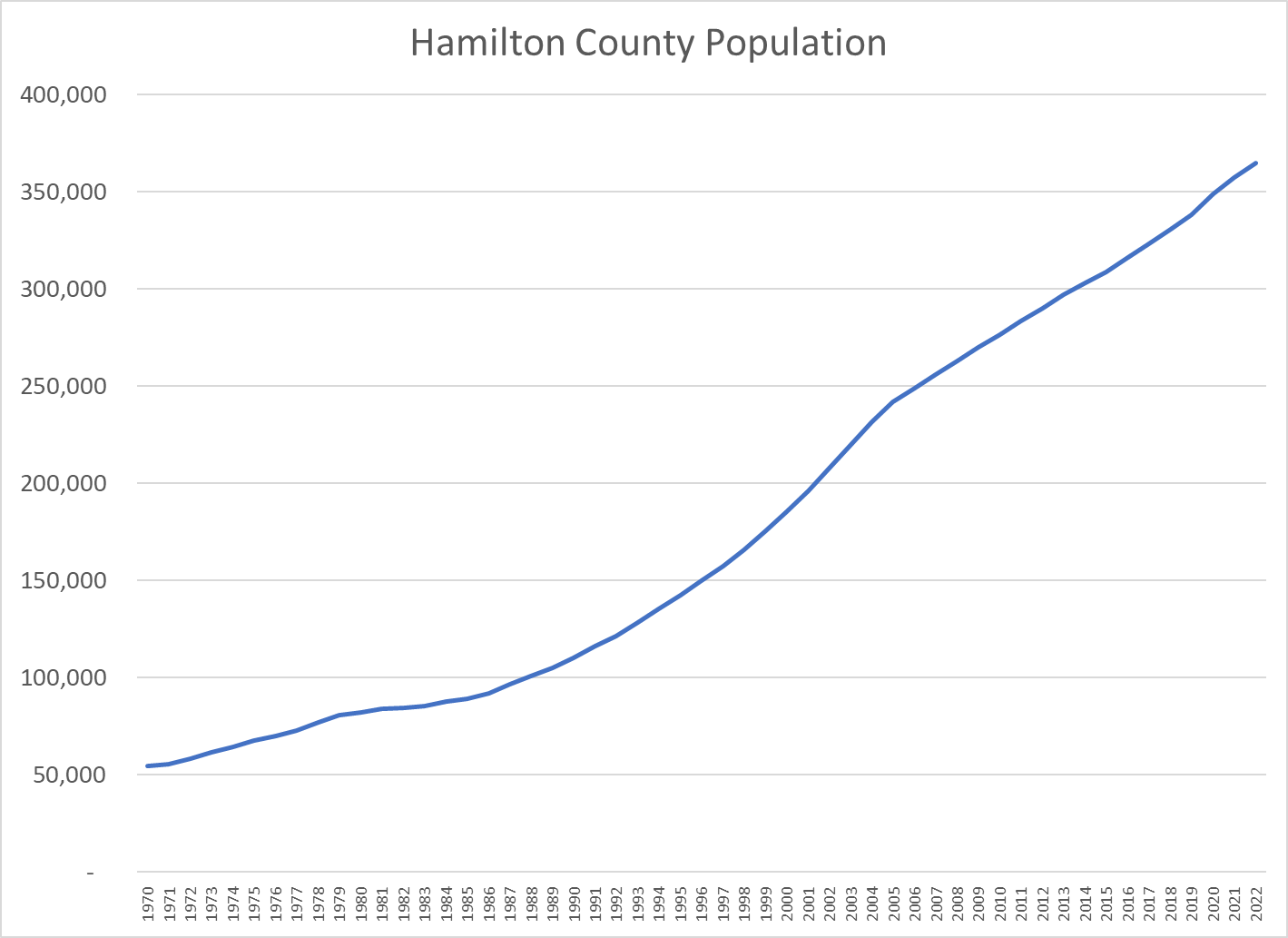

Hamilton County, Indiana is north of Marion County and Indianapolis. It has grown seven-fold since 1970, from 54,000 to more than 365,000 people. It now ranks in the top 7% as the 209th largest county of the 3,142 in the US. It is the fourth largest of Indiana’s 92 counties, trailing Marion (Indianapolis), Chicago’s suburban Lake County and Allen County (Ft. Wayne) which it will surpass for third place in 2029.

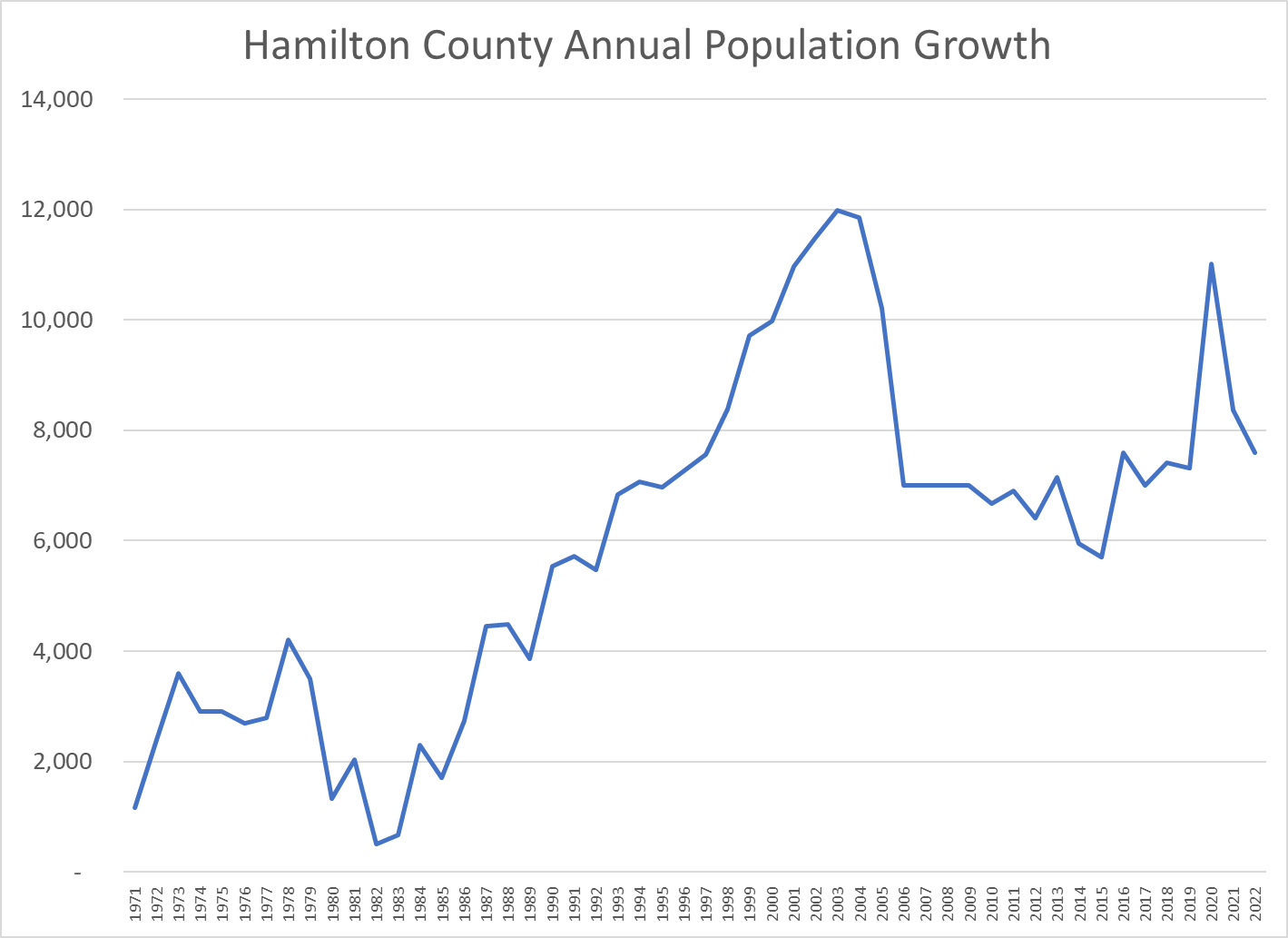

The county has averaged a 7,800 person annual increase since 1990 and has maintained a 7,500-person annual increase in the last decade.

Growth reached a peak of 12,000 per year prior to the Great Recession, dropped back to 7,000 per year and has slowly grown to 8,000 per year.

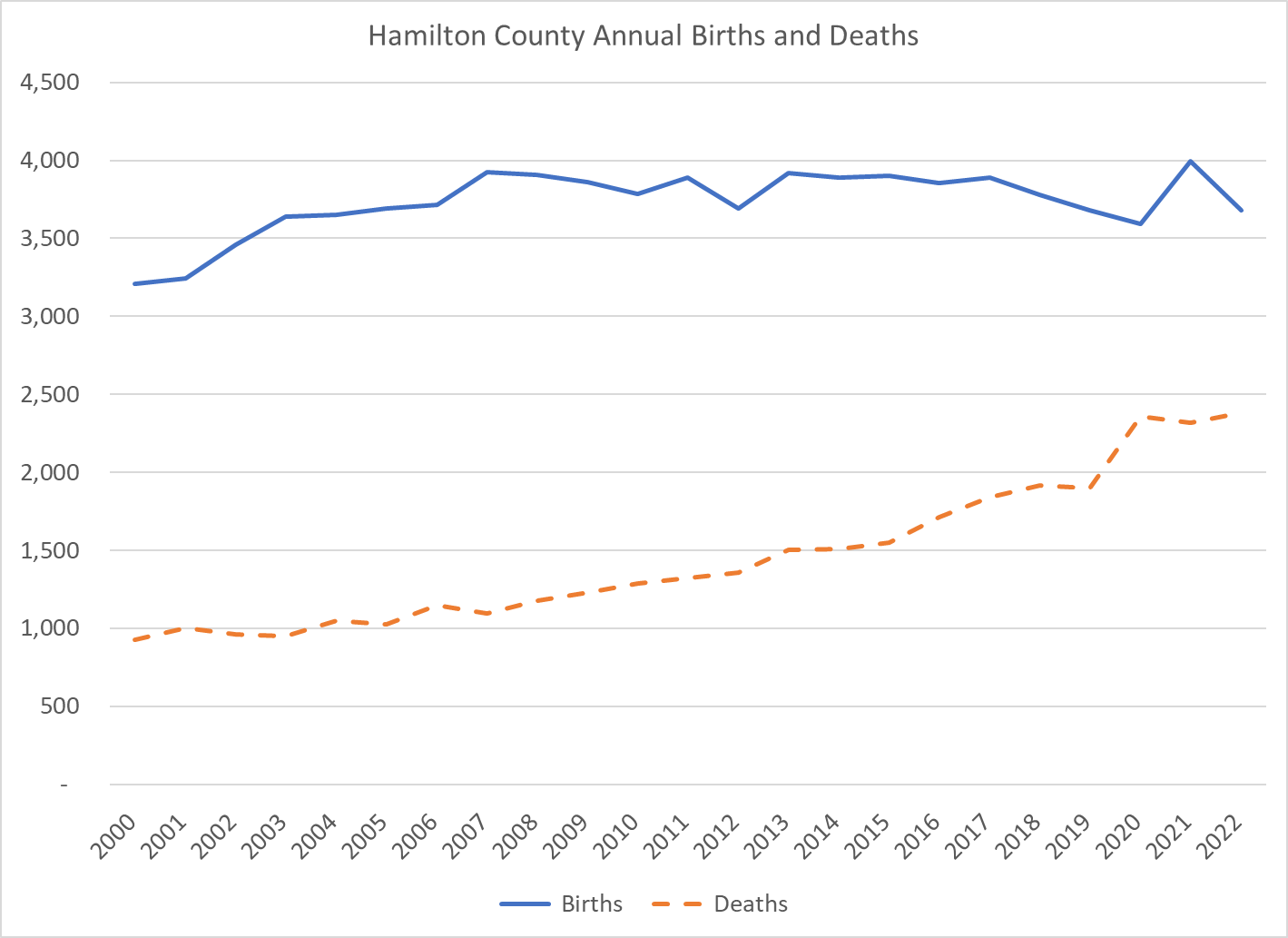

As a growing suburban area, the county has benefitted from a younger population with relatively more births and less deaths. This demographic advantage has decreased through time.

On average, this natural increase advantage has provided 2,000 additional people each year for the last two decades. The net in-migration level was over 8,000 before the Great Recession, dropped in half to 4,000 before recovering to about 6,000 people per year.

The US Census Bureau’s American Community Survey (ACS) attempts to measure the annual migration flows between all 3,142 counties! It’s survey techniques generally require a 3-5 year sampling period to have statistical reliability. The US Census Data and the Indiana Vital Statistics Data (Births and Deaths) show an implicit net in-migration to Hamilton County from 2011-20 of 4,575 annually. The ACS reports just 3,124. The actual increase is 144% of the surveyed increase.

Hamilton County’s population ranged from 283-346,000 between 2011-20, for an average of 314,000. Inbound migration averaged 23,600 per year or 7.6% of the population. Outbound migration averaged 20,400 per year or 6.6% of the population. On average, the county’s population turns over every 15 years. The net in-migration in the ACS survey was 3,100, a little more than two-thirds of the implicit 4,600 net in-migration per year. I compared the 2011-2015 and 2016-2020 data and found that they were generally consistent. I believe that the proportions reported are generally accurate.

International In-Migration

ACS reports an annual average of 1,800 international immigrants. This is 59% of the net 3,100 figure; quite material. On an annual basis, this is just 0.6% of the county population, but for a decade it is 6%. 61% of Hamilton County’s international immigrants report Asia as their home continent.

Total US Migration

Net in-migration to Hamilton County from the US is a positive 1,300 per year in the ACS survey, perhaps 1,900 including the 1.46X factor. Net domestic net in-migration is two-thirds the size of international net in-migration; 0.4% annually or 4% per decade.

48 States Aside from Indiana and Illinois

Net in-migration to Hamilton County from the other 91 counties in Indiana plus Illinois averages 3,004 per year, essentially equal to all of the total net in-migration. Net in-migration to Hamilton County from the other 48 states is a negative 1,700 per year, roughly one-half of the positive overall net in-migration figure. Hamilton County receives minor positive inflows from the adjacent states of Ohio, Michigan and Kentucky. It sends 1,000 residents to Texas each year and receives just 400 in return. Texas accounts for one-third of Hamilton County’s net out-migration aside from Indiana and Illinois. Hamilton County exports 1,200 residents annually to Florida but an equal 1,200 return each year.

Chicago, Illinois

In the last decade 1,500 people annually moved to Hamilton County from Illinois (Chicago) and just 700 returned the favor. Hamilton County received a net 800 residents from Illinois each year in the past decade. This is one-fourth of the net in-migration to Hamilton County. Many Hamilton County college graduates make Illinois their first professional home, so the flow of experienced professionals from Chicago to Hamilton County is probably more than 1,500 per year.

Marion County, Indiana (Indianapolis)

Hamilton County’s Carmel, Fishers, Westfield and Noblesville claim that they are “edge cities” somewhat independent of Indianapolis. In the last decade a net 3,300 migrants from Marion County chose to make Hamilton County their home each year, accounting for more than ALL of the ACS survey’s 3,100 annual increase. Marion County has nearly 1 million people and continues to grow slowly despite this 0.3% annual leakage to Hamilton County.

College Students

Hamilton County school graduates have very high college attendance rates. Hamilton County exports 2,600 students each year to IU, Purdue and Ball State and receives 1,000 back, for a net out-migration of 1,600 per year, about one-half of the net in-migration figure.

Indiana

Hamilton County has a minor net in-migration from sparsely populated Boone County to its west (300/year). It’s net in-migration with the 8 nearby counties, including Boone, is a 500 loss. Hamilton County is an attractive suburban destination, but net net it loses 500 residents annually to nearby counties other than Marion.

Setting aside Marion County and the 3 university counties, Hamilton County attracts 500 new residents annually from the other 87 Indiana counties.

Summary

Hamilton County enjoys a 2,000-person annual natural population increase due to its relatively young age profile. Half of its 6,000-person annual net in-migration is driven by international immigrants attracted to its schools, amenities, services and culture. Most of its remaining growth is driven by nearby Marion County residents who are seeking the same results. Hamilton County is attracting residents from Chicago as retirees, commuting residents or transplants. Hamilton County loses about 2,000 college students each year who migrate into a national labor market. This is an opportunity for further population growth. It also shows that the net 3,100 growth per year figure understates the attractiveness of this county to all potential migrants.

Kindly set Joe Biden aside. As of today, he is clearly most likely to be nominated.

Four others show up on the pundits’ “most likely” lists but will probably not be nominated. New Orleans’ mayor Mitch Landrieu is a career politician from a red state. Kamala Harris has not taken advantage of her VP post. Elizabeth Warren and Alexandria Ocasio-Cortez are too far left.

Like Joe Biden, Bernie Sanders, Michael Bloomberg and Jim Webb may have aged out of contention.

Robert Kennedy, Jr and John bel Edwards are too far right.

Sherrod Brown, Marianne Williamson, Phil Murphy and Tammy Baldwin are too far left.

Terry McAuliffe, Beto O’Rourke and Stacy Abrams have incurred political losses that require them to re-establish their bona fides.

Seven candidates floated “trial balloons” in 2016 or 2020 but failed to gain traction. They each need to define a “compelling reason” to return to the national spotlight. Michael Bennet and Jay Hickenlooper in Colorado. Martin O’Malley, Tom Steyer and Deval Patrick on the east coast. Jay Inslee on the west coast. Julian Castro in Texas.

Four candidates are branded with the liberal “red L” of Chicago or New York. Rahm Emmanuel and JB Pritzker. Kirstin Gillenbrand (perhaps unfairly) and Bill de Blasio. Tom Steyer and Michael Bloomberg are handicapped again.

I don’t see the national case for Gina Raimondo, Andrew Yang or Andy Bashear.

Mark Kelly, Josh Shapiro, Jared Polis and Wes Moore are relative newcomers to the national stage.

I present 4 “sleepers” who don’t have consensus national media support.

Booker, Buttigieg, Cooper, Klobuchar, Newsom and Whitmer are attractive presidential primary candidates for Democratic voters. Warner, Kaine, Hassan and Warnock could also become realistic candidates.

McAuliffe, O’Rourke, Abrams, Bennet, Hickenlooper, O’Malley, Steyer, Patrick, Inslee and Castro have political assets that could be appeal on the national primary stage.

Breaking away from the pack is difficult today. Ironically, the larger-than-life dimensions of Trump and Biden may prepare the way for competitive future primaries between relatively equal candidates.

Real mortage interest rates can be calculated as the difference between nominal mortage interest rates and the 10-year Treasury Bond interest rate. Although nominal interest rates have ranged from 3% to 16%, the real, after expected inflation, interest rates are remarkably consistent, averaging just 1.7% and ranging between 1.3% and 2.1% in 70% of the last 52 years. The peak real rate was 3.0% in 1982 following the unexpectedly high and remaining high nominal rates of the prior 4 years.

Banks, mortgage-backed securities investors and mortgage borrowers all take risks when they complete mortgage transactions. Lenders are betting that their present and future borrowing interest rates are and will be low enough to fund their mortgages at a profit. Each lender locks in funding commitments for a reasonable share of the loan life and counts on the consistency of interest rates over the business cycle to fund the remaining portion. Lenders that experience a mismatch put their stockholders’ equity at risk and face bankruptcy. Investors in mortgage-backed securities are subject to valuation change risks throughout the period in which they are invested. Most such investors hold diversified portfolios of mortgages (region, amount, riskiness, urban vs suburban vs rural) and non-mortgage assets to ensure that any investment decision will not be too damaging.

Fixed-rate mortgage borrowers are betting that inflation will not fall too much lower than the expected inflation rates when they borrowed. If so, they will be paying back the mortgage in higher real value dollars than expected. If inflation and mortgage rates drop by more than 2%, most borrowers will seek to refinance their mortgages at the new, lower market rates, paying another round of closing costs for this privilege. Fixed rate borrowers are also hoping that inflation will be higher than the expected inflation rates at the time they borrowed, allowing them to pay back their debt with cheaper real dollars. Mortgage originators do not generally have the legal right to “call” the debt and require a change in the rates and terms as many commercial lenders and bond issuers do.

The “good news” is that the US mortgage market is very efficient and the real interest rate premium for borrowing to own a home is just 2% more than what the US government pays for borrowing. Borrowers face interest rate change risks, especially being caught with a high interest rate mortgage when inflation rates fall if they are unable to refinance.

The market has been tested through 7 business cycles and held up very well. The “Great Recession” exposed excessive risk taking by mortgage originators and funders. They lost money and many went out of business. Riskier mortgages are rarely issued today, and government regulations provide some added protection against any future overreach.

For higher income households that itemize deduction on their federal tax returns, the nominal interest rate paid is a tax-deductible offset to earned income. These individuals typically pay 22%, 24% or 34% marginal tax rates. A 5% nominal tax rate can provide a 1%, 1.25% or 1.65% reduction in the effective interest rate, thereby making the 2% real mortgage rate less than 1%. Higher income households can benefit greatly from this tax benefit.

Real, after inflation, Gross Domestic Product is up by one-third, despite the pandemic. That’s 2% annually, despite the Great Recession and the pandemic. The US economy is very solid.

A 21% increase in per capita income during this time. Quite solid and constant growth.

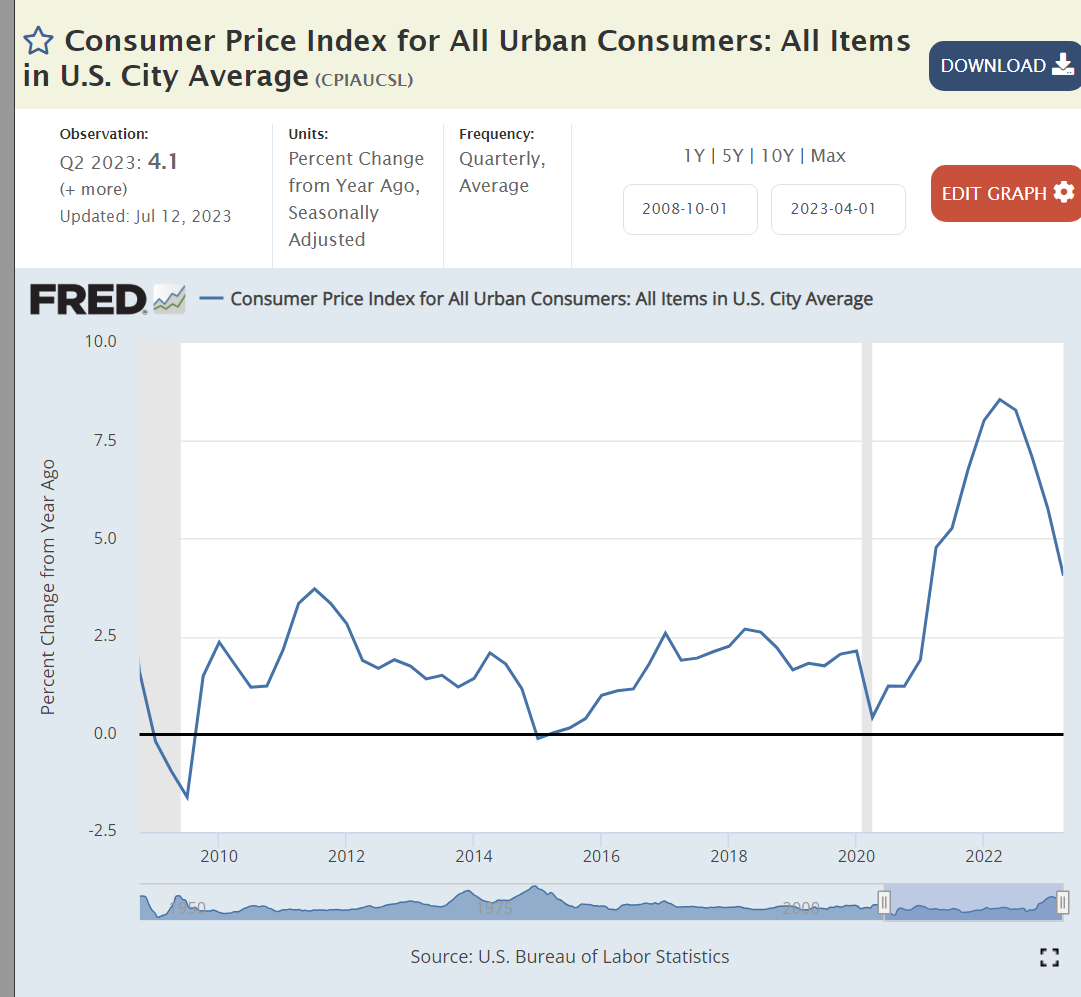

Inflation averaged a bit less than 2% before the pandemic, spiked to 8%, and has since declined to 4%. Experts disagree on whether it will return to 2% soon.

Gas prices are the most obvious component of inflation. They are largely driven by global supply and demand. Prices today are the same as in 2011-14, despite the general inflation increase of more than 20% since then.

Despite the pandemic, US unemployment is at a 50 year low!

Job seekers today encounter 3 times as many job openings.

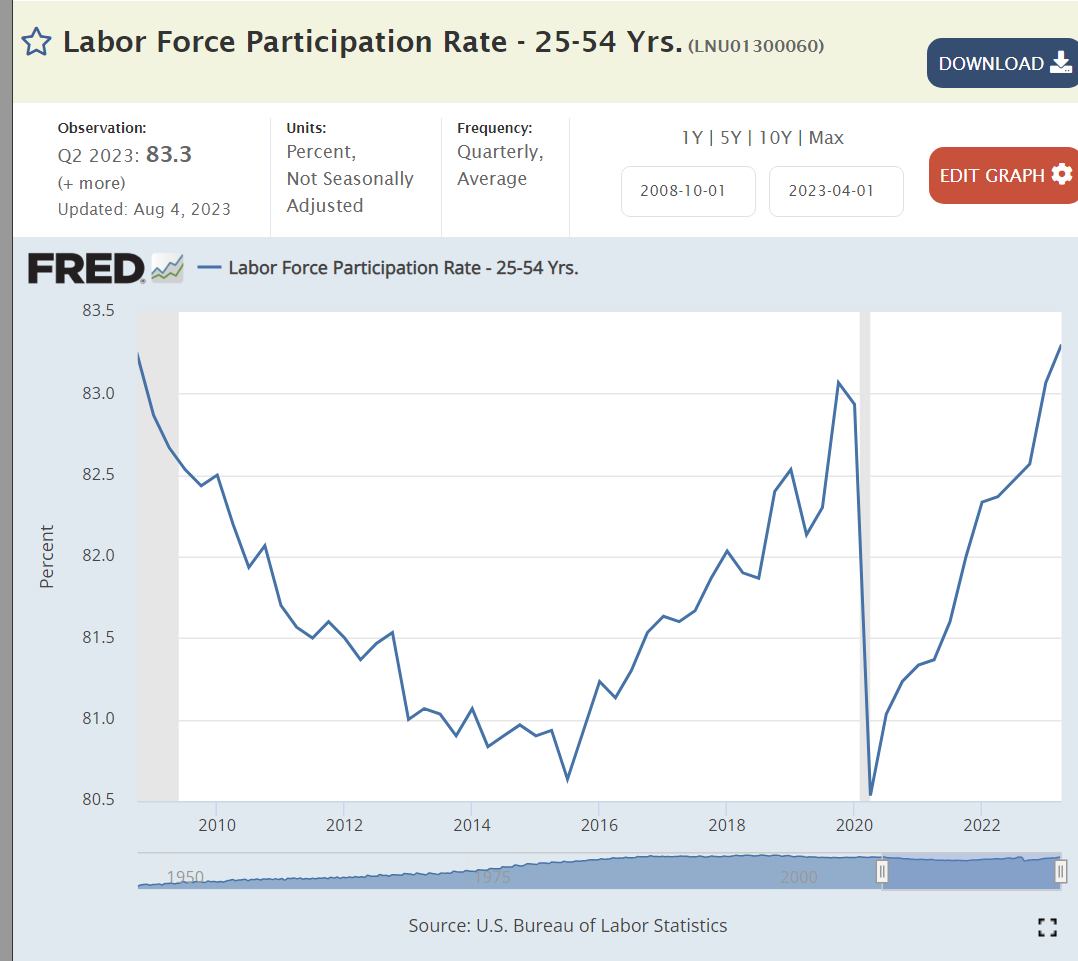

Core age labor force participation has snapped back after the pandemic.

Investment values have doubled.

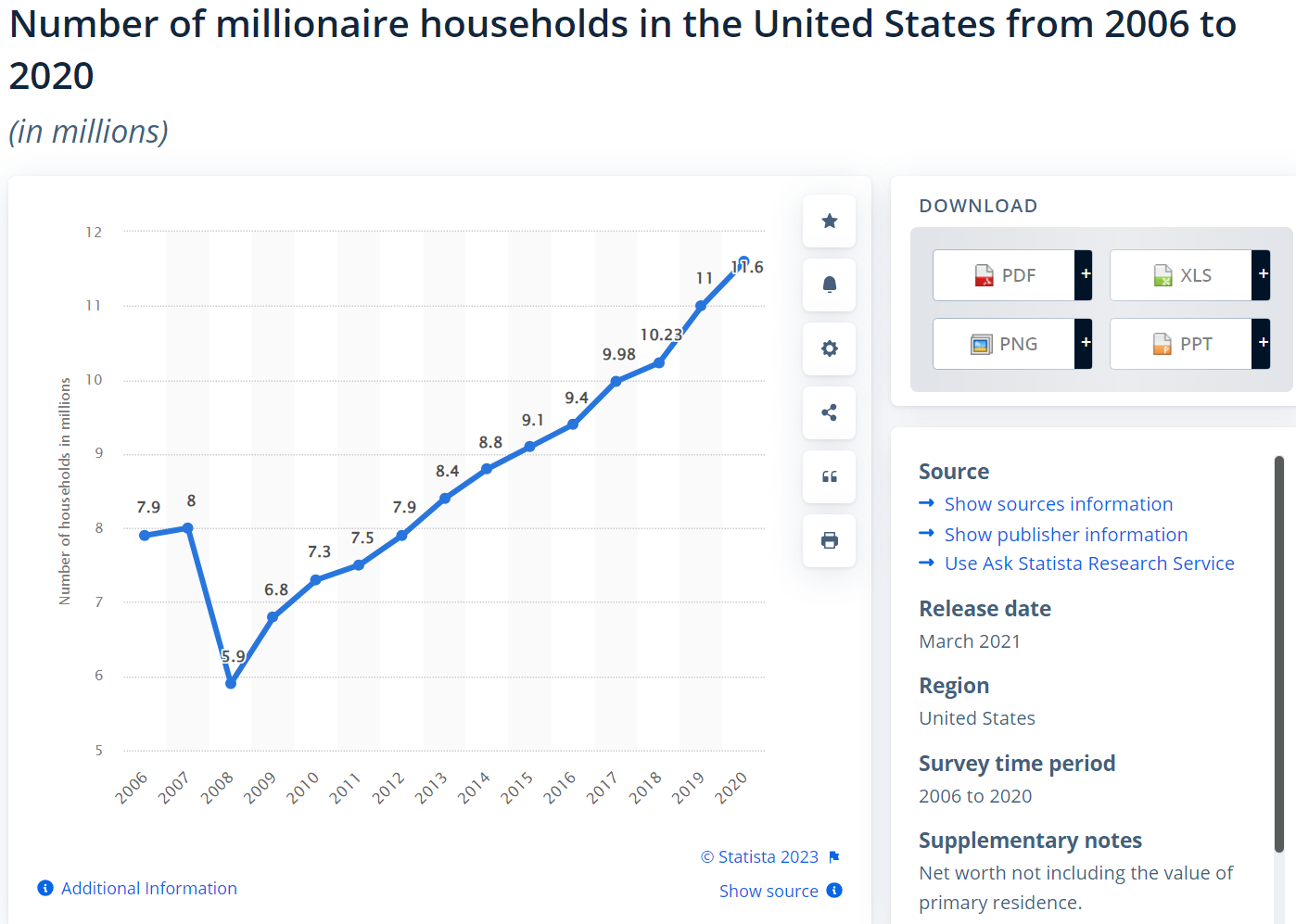

The number of millionaires and billionaires in the US has continued to increase.

Personal savings rates rose from 6% to 9% before the pandemic, shot up and fell back down to just 4% recently.

Housing values have doubled since the Great Recession.

Mortgage rates averaged 4% after the Great Recession, dropped to 3% and then increased to 6%+ as the Federal Reserve raised interest rates.

US exports have nearly doubled in 14 years.

Despite the Trump tariffs, which Biden has maintained, imports have also nearly doubled.

Despite historically slower growth rates, higher budget deficits and looser monetary policies, the US dollar is more highly valued today than in 2008.

Foreign countries still see the US as a positive ally, despite their concerns during the Trump era.

Obama returned the budget deficit to a “reasonable” 3% by 2016. Trump expanded it to 5% and then 15% as the pandemic struck. Biden drove some recovery to 5% by 2022, but has not driven further reductions.

US coal production is in a long-term decline.

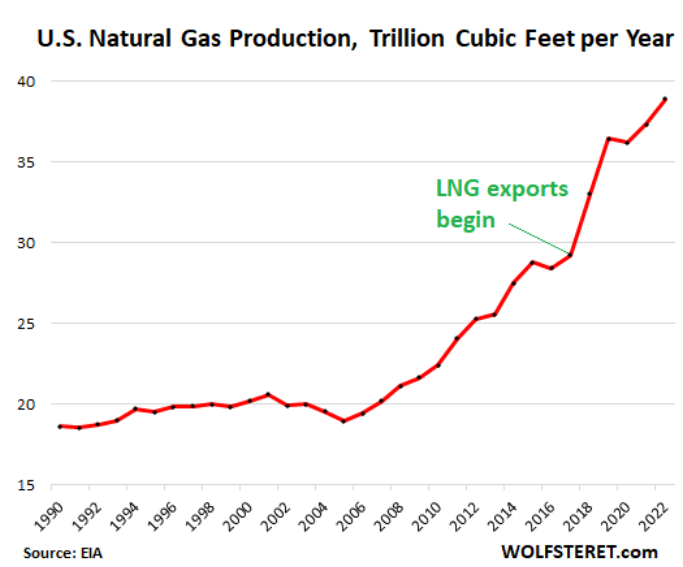

Natural gas production has nearly doubled in 14 years.

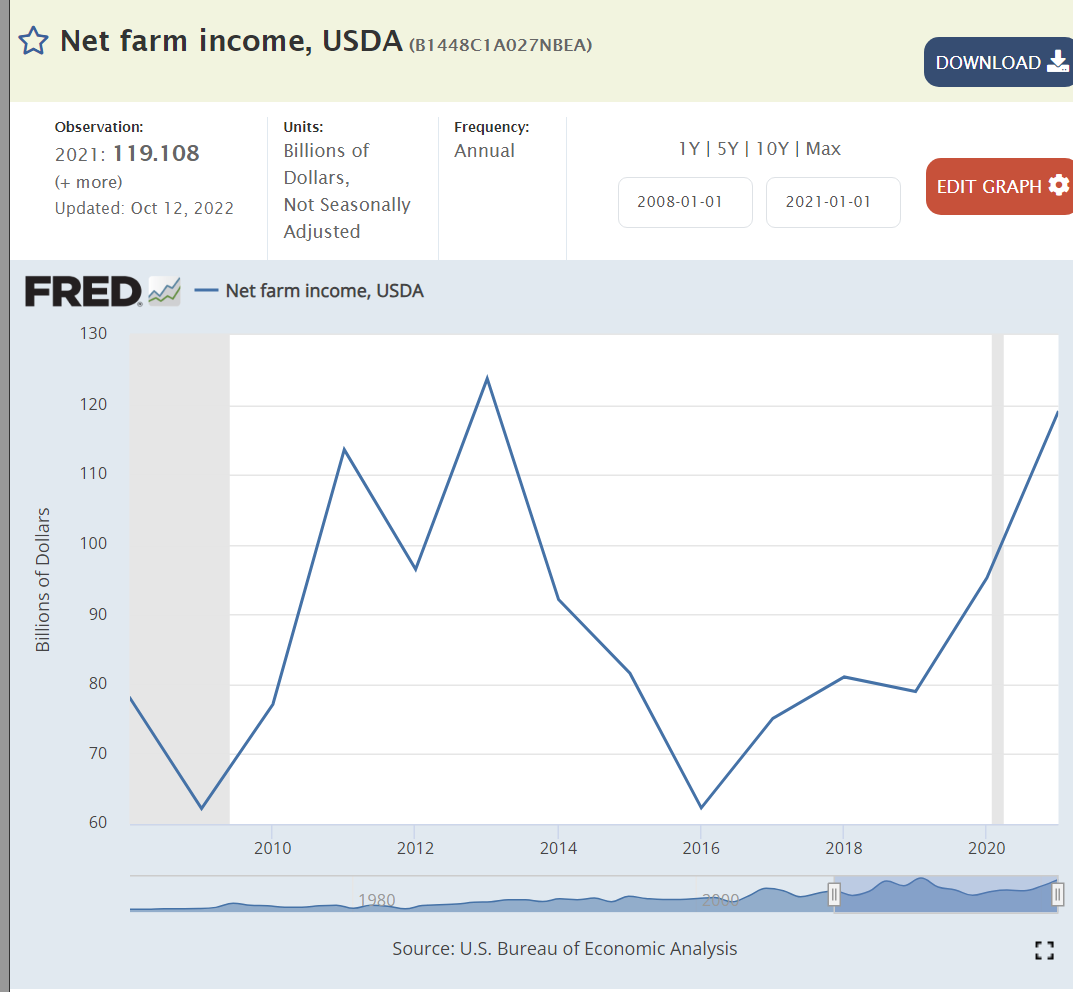

Net farm income has been significantly above the base for 6 of the last 14 years, despite lavish Trump farm subsidies.

Manufacturing employment has continued to rise slowly in the last 14 years against the headwinds of international competition.

It’s difficult to put the pandemic in perspective, but here we see a 2-year reduction in expected lifespans. Opioid deaths and so-called “deaths of despair”, alcohol, drugs, suicide, also play a role.

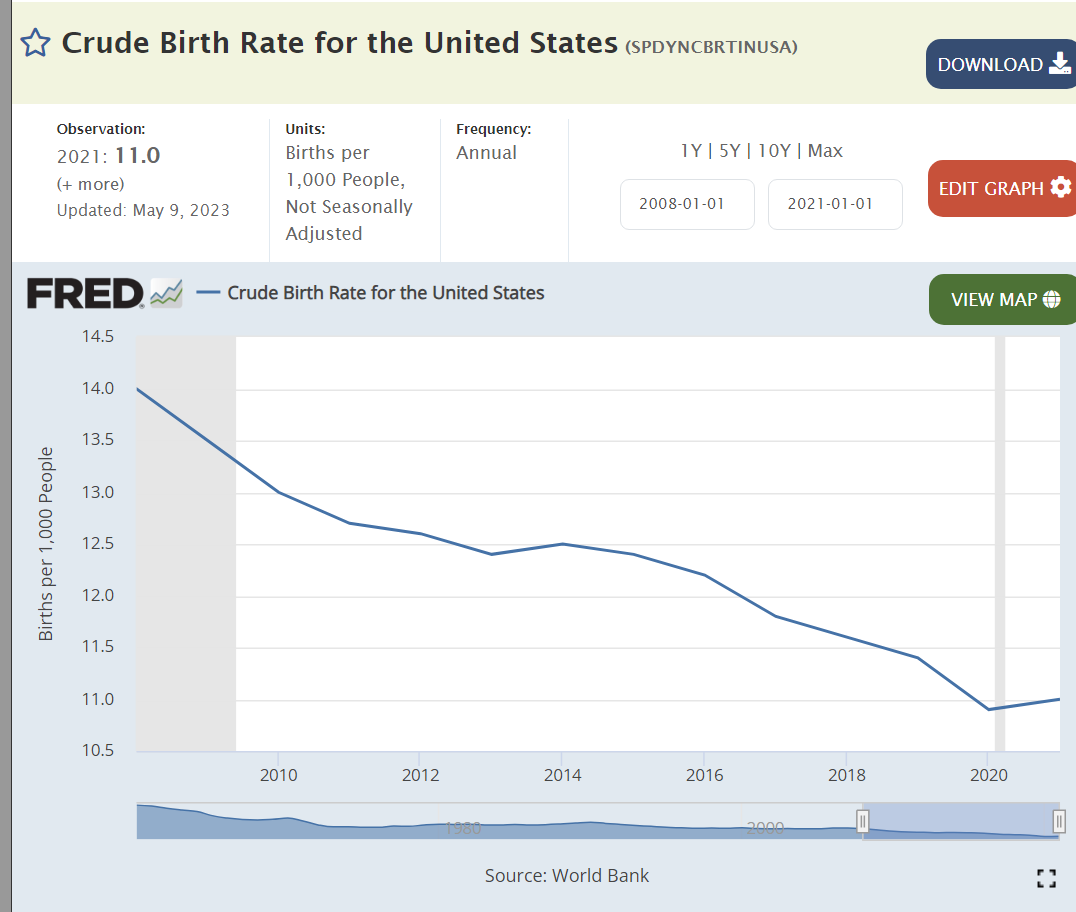

Birth rates continue to drift lower as seen in all regions of the world.

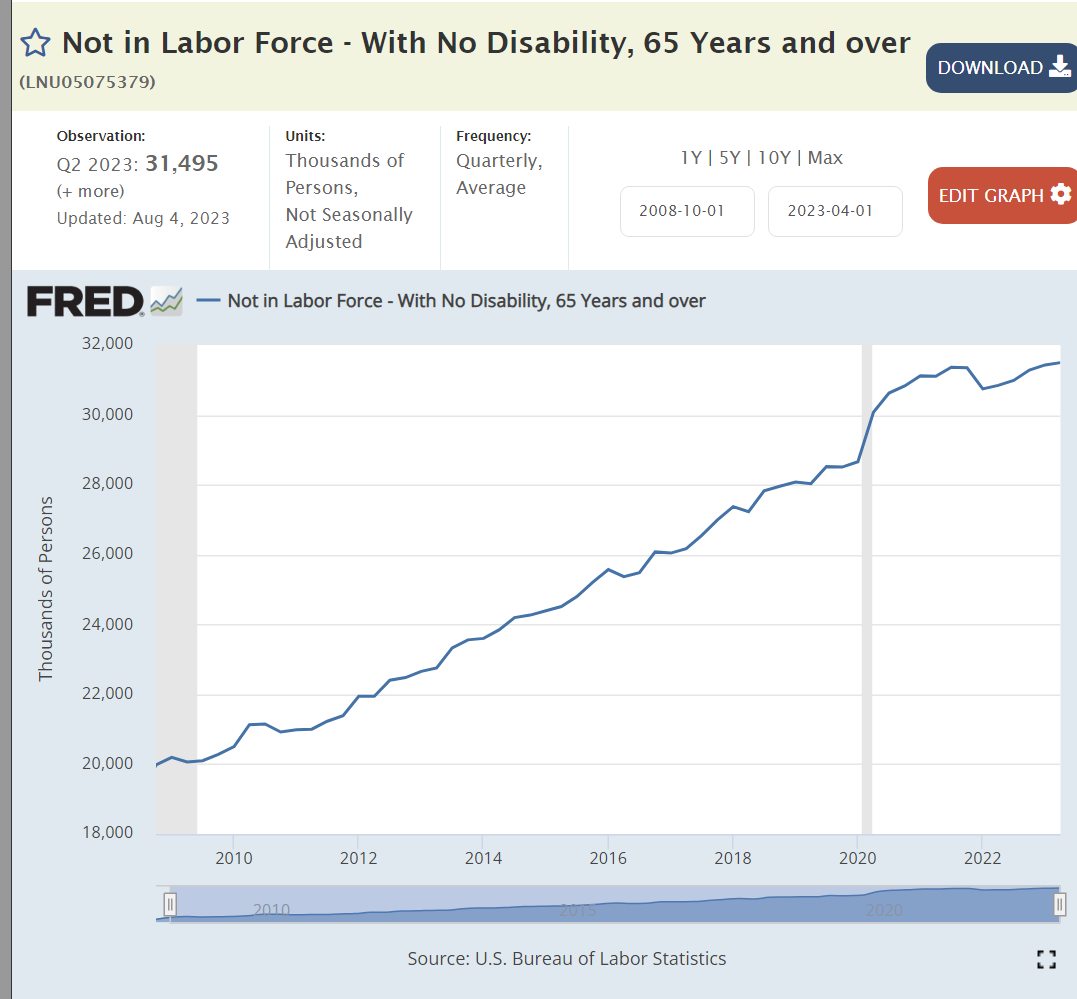

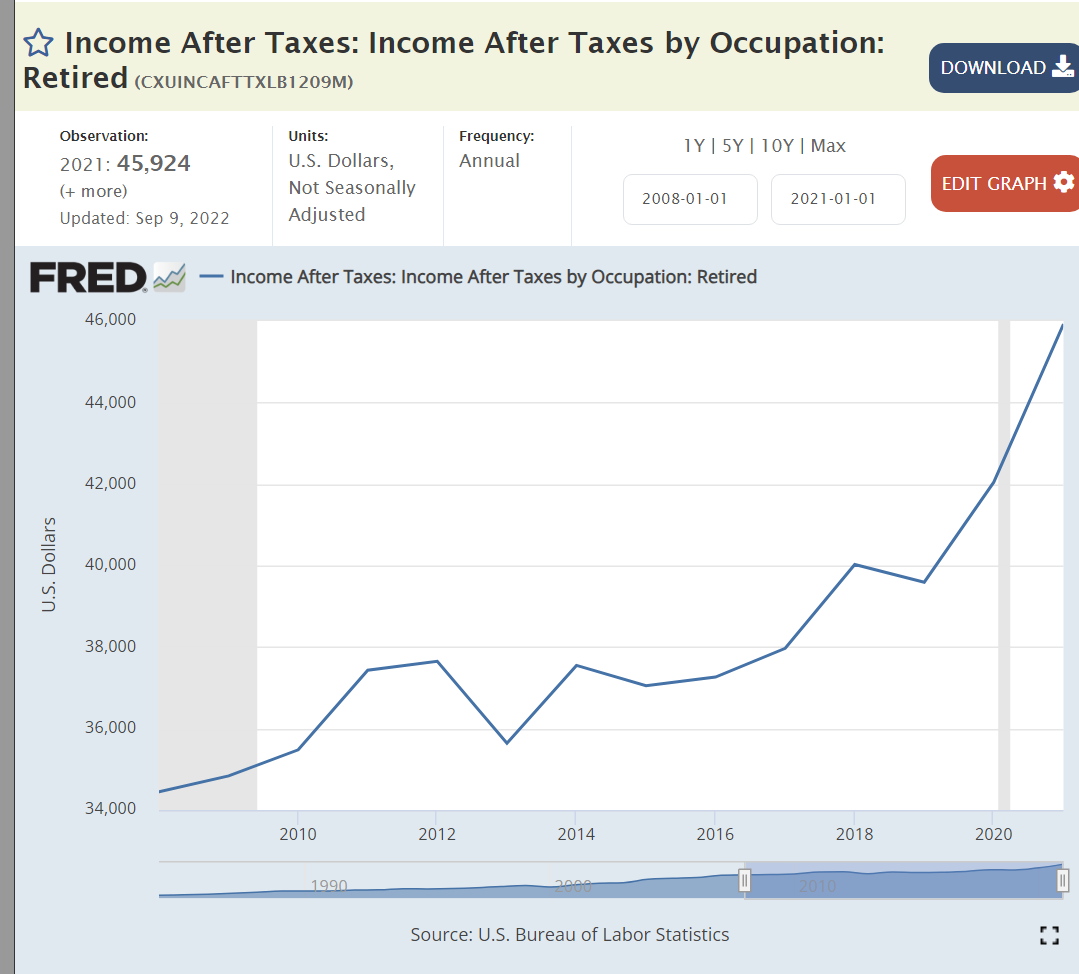

The number of retirees has increased by more than 50%.

Retiree incomes are up by one-third, matching inflation.

Prospective retirees have doubled their cumulative savings.

The abortion rate has continued to fall in the last 30 years.

Church attendance has dropped from 40% to 30%.

Summary

The US economy recovered slowly after the Great Recession and then very quickly after the pandemic. Real, after inflation, output and per capita output increased. The labor market became very tight. Asset prices (investments and housing) rose for intrinsic and monetary reasons. The US remained a competitive international producer. The federal budget deficit was better at the end of the Obama period but worse for Trump and Biden. The pandemic reduced life expectancy and households had fewer children. Successful retirements grew and will grow. Social trends continue, uninterrupted by political positioning and policies.

Perceptions of the country and the economy are increasingly shaped by partisan political party views. Nonetheless, the US economy continues to grow and thrive.