Hotel capacity increased by 50% from 1995 to 2019.

Demand grew at the same 50% rate, although not always in lockstep.

Occupancy averaged a healthy 63% (almost two-thirds) through this period, with significant differences due to changes in construction and the economy.

The price per room averaged about $125 per night in real 2020 dollars, again varying based on supply and demand, but overall, relatively constant.

Total hotel industry real revenue ($2020) for the 21 years from 1998 through 2019 increased by a little less than 50% according to Bureau of Economic Analysis (BEA) figures.

Real consumer only (leisure) sales increased by nearly 100% during this period.

Real consumer sales per person increased by about two-thirds.

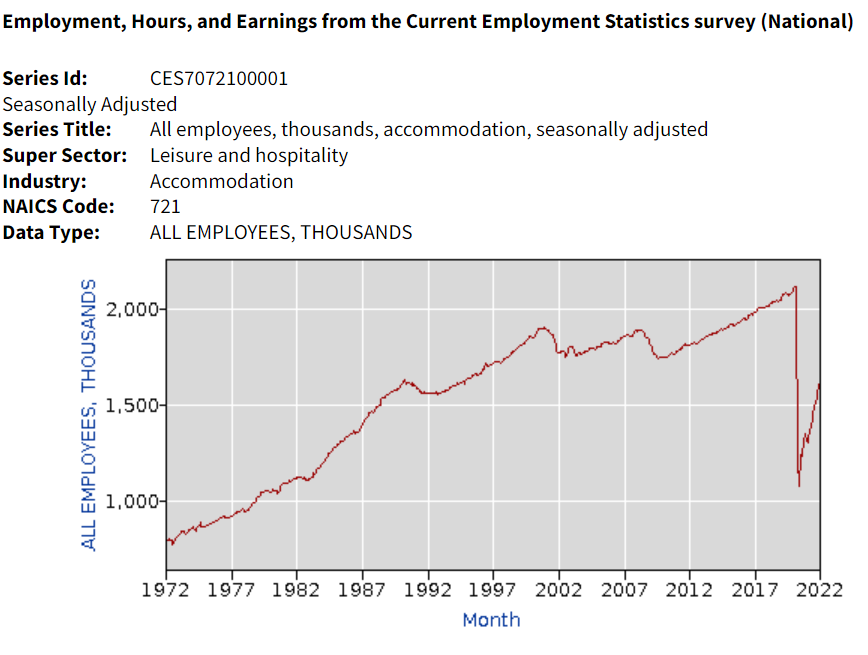

Hotel industry operating statistics before 1995 are not readily available. The tremendous growth of the industry in the last 30 years of the twentieth century is illustrated by the more than three-fold growth in industry employment, from one-half million to 1.8 million. Note that employment did not follow the growth of rooms during the first 20 years of the next century.

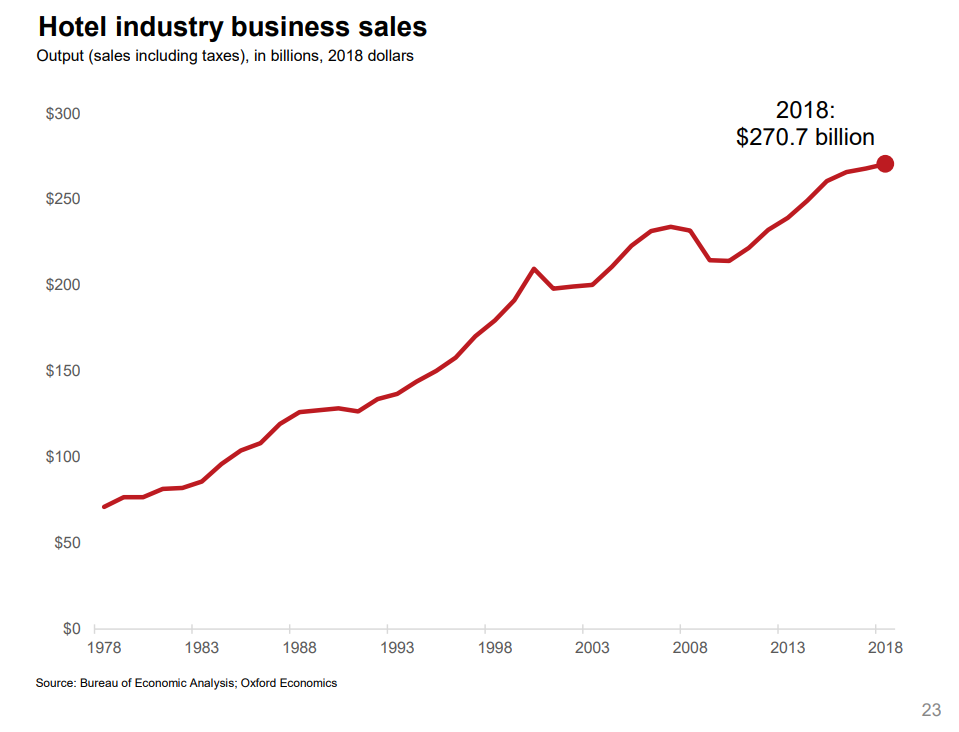

Oxford Economics developed an industry promotion brochure in 2019 that has some longer-term data. Total real (inflation adjusted) revenue is up more than 4 times in 40 years. Our 1995-2018 data shows relatively small changes in average hotel prices. I suspect that there were “real” increases from 1978 – 1995 as the industry was growing quickly in response to consumer demand.

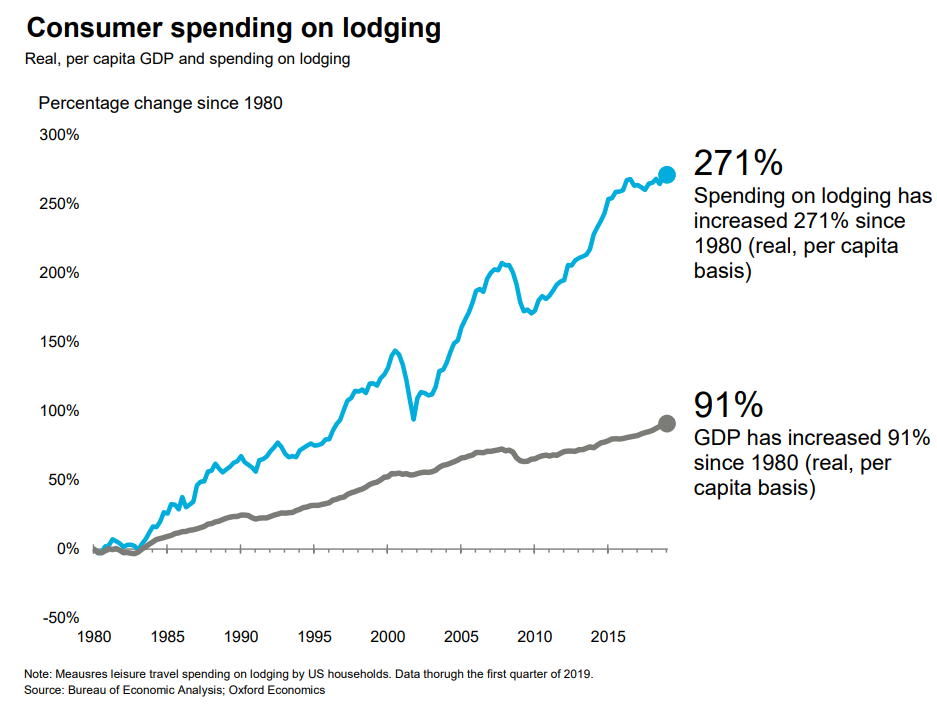

A similar measure, gross domestic product (GDP), or production value added, net of the cost of inputs, increased 3-fold in 40 years.

Consumer spending on accommodations has increased about 3 times as fast as GDP overall in the last 40 years.

Hotel purchases as a share of total consumer spending has increased by more than 80% in these 40 years.

Overall demand for hotel rooms per citizen for all uses (personal, business, government and foreign travelers) has increased by 20% across 30 years. Personal and foreign travel have grown at a faster rate.

The short-term rental market (personal vacation rentals, Airbnb) has grown from zero to 10% of the hotel room volume and appears to have years of growth ahead of it. This growth is not included in the industry summary figures.

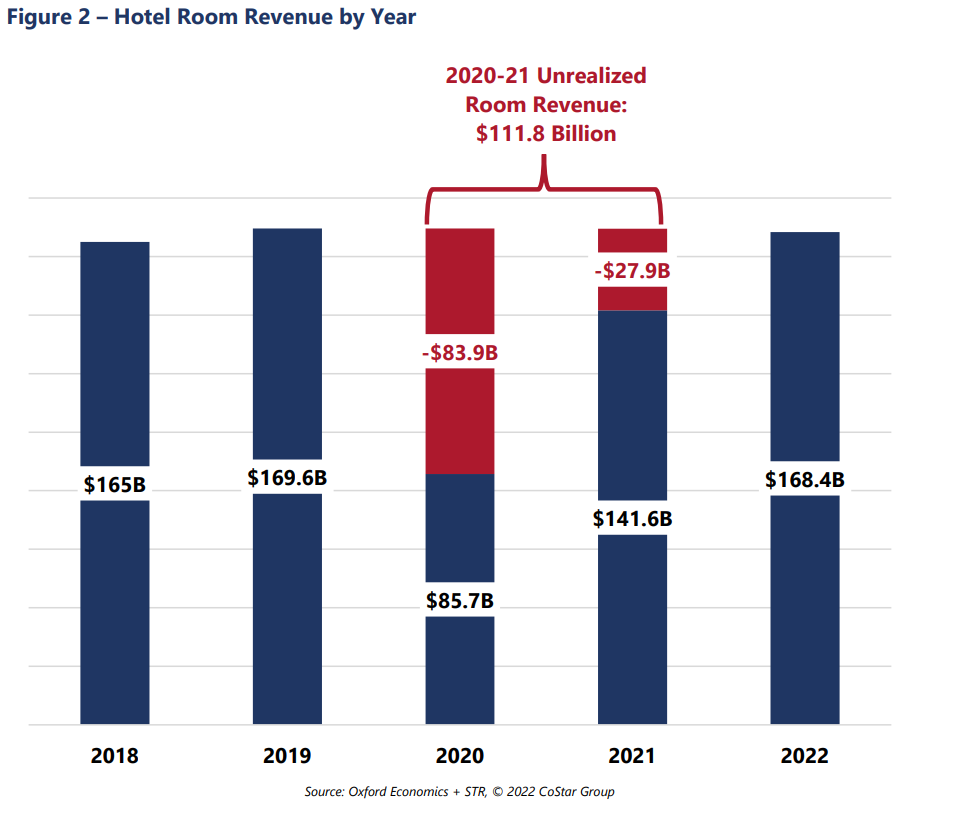

Occupancy is forecast to return to the historical average of 63% for 2022 and increase further in the following years. The industry “lost” more than $100B of revenues due to the pandemic, so analysts estimate that the industry will return to “normal” employment, prices, profitability and reserves by 2025.

Consumer access to hotels and private rentals has increased by 3 or 4 times in the last 50 years, at a faster rate in the first 25 years, and somewhat slower in the last 25 years. Hotel business models at 63% occupancy seem to justify continued capital investments in new supply. Prices have been relatively flat for 25 years. Competition between brands, pricing segments, corporations and private owners seem to be effective at providing adequate capacity and service options at competitive prices.

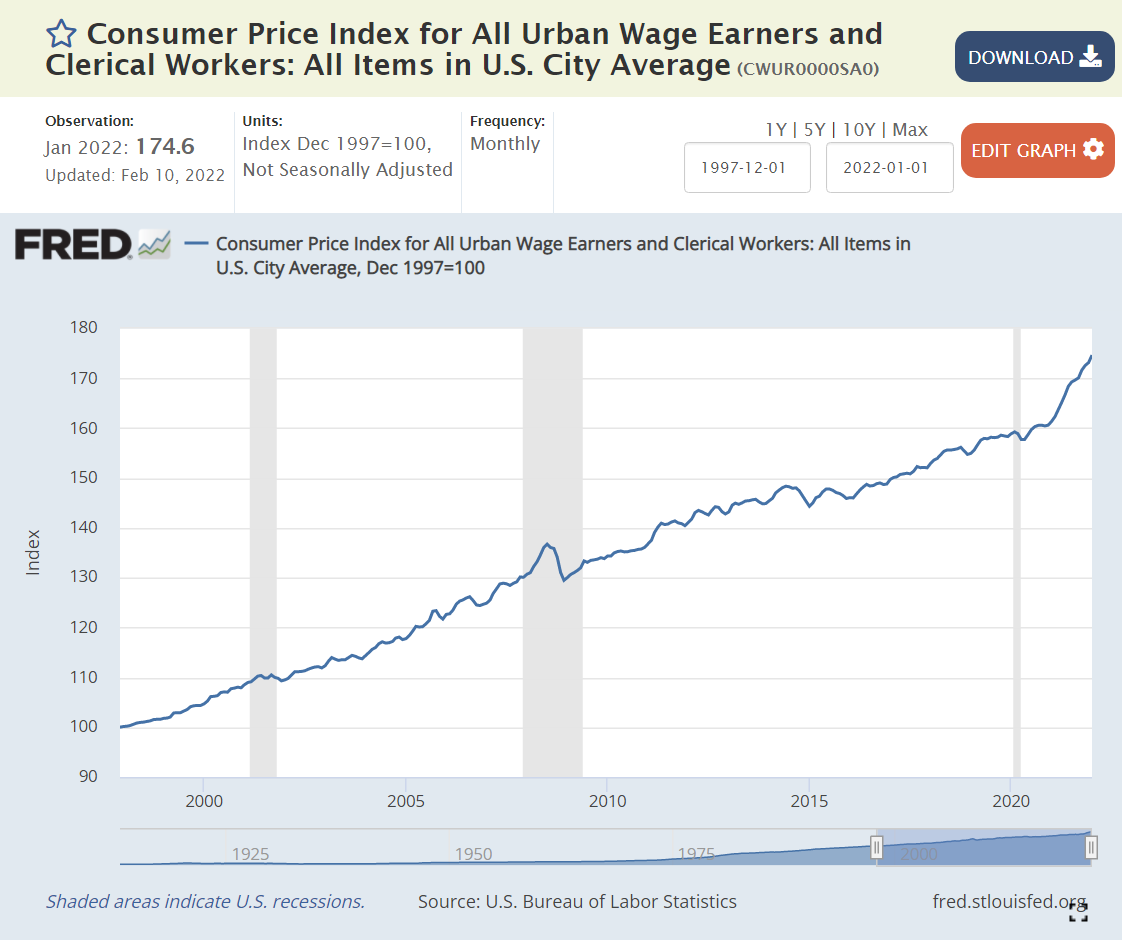

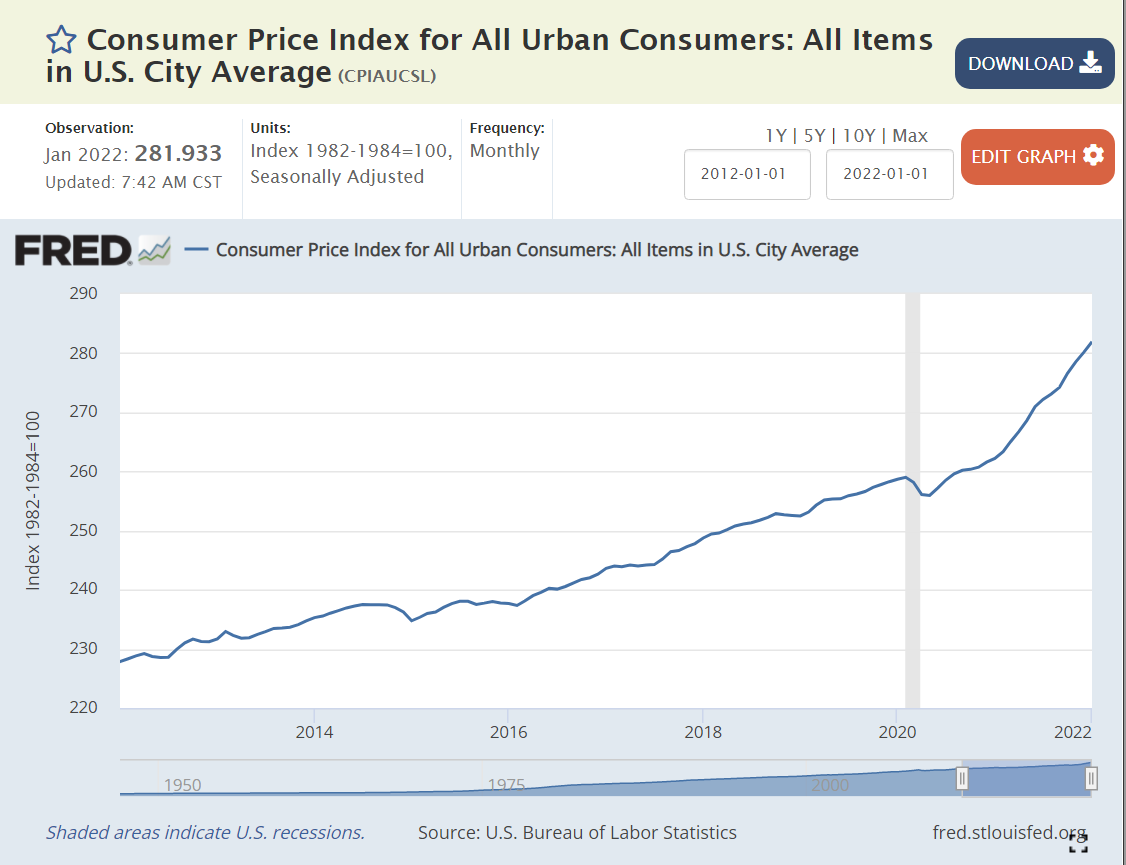

Inflation is back in the news after several quiet decades. The components of the All Urban Wage Earners and Clerical Workers are listed above, comparing Feb 2020 with a 1997 base of 100, and then Jan 2022 with the same base. The most recent weighting of categories is in the rightmost column.

Overall, consumer prices have risen by a modest 2-2.5% annually, just 59% through Feb 2020 and 75% through Jan 2022. Yes, that is a 10% price increase in the last 2 years: 175/159.

The 3 largest components have shown price rises close to the overall average. The biggest sector, Housing (39%), displays slightly higher inflation, at 72% and 85%, closer to 3% annually, with a possibility of higher rises for the next few years. Transportation (22%) reveals lower than 2% annual inflation with a 45% increase across the full period. Food and Beverage (15%) is close to the average with 64% and 82% growth.

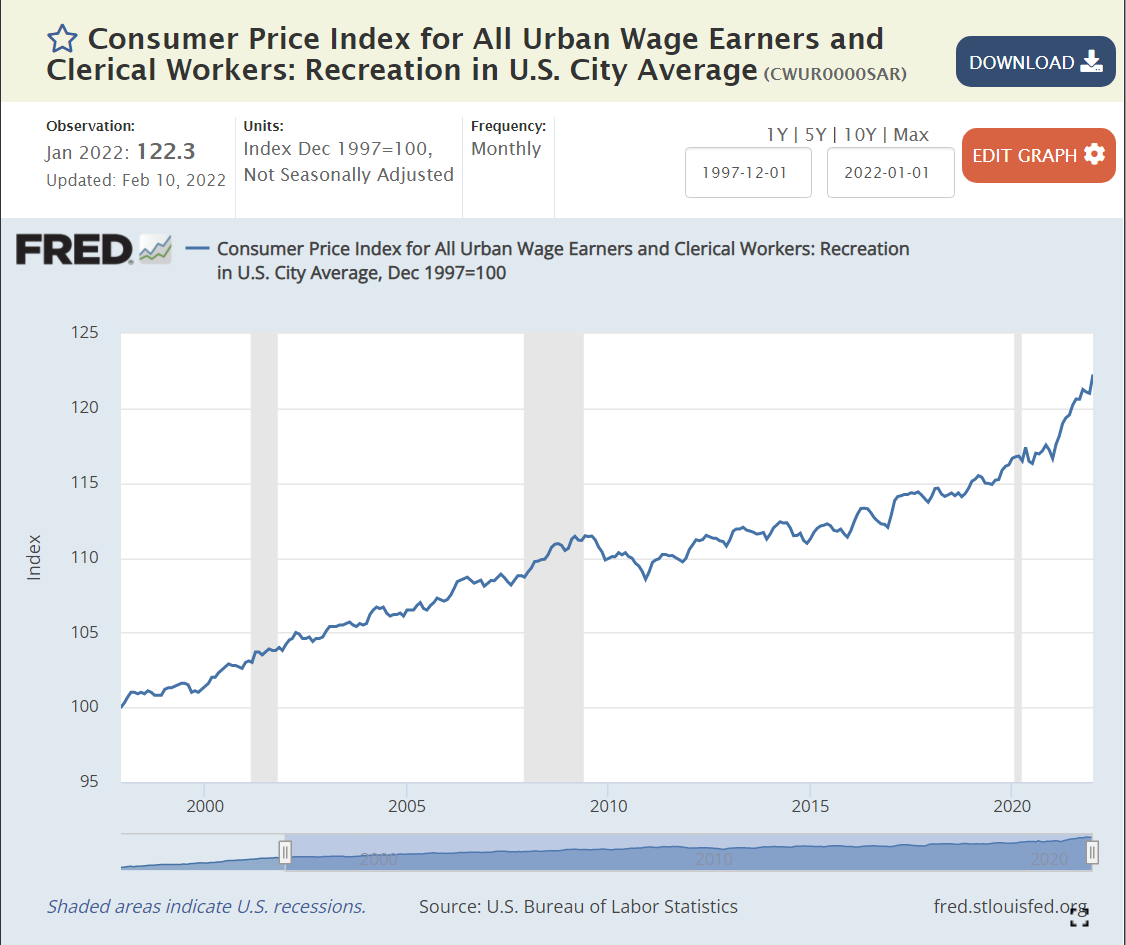

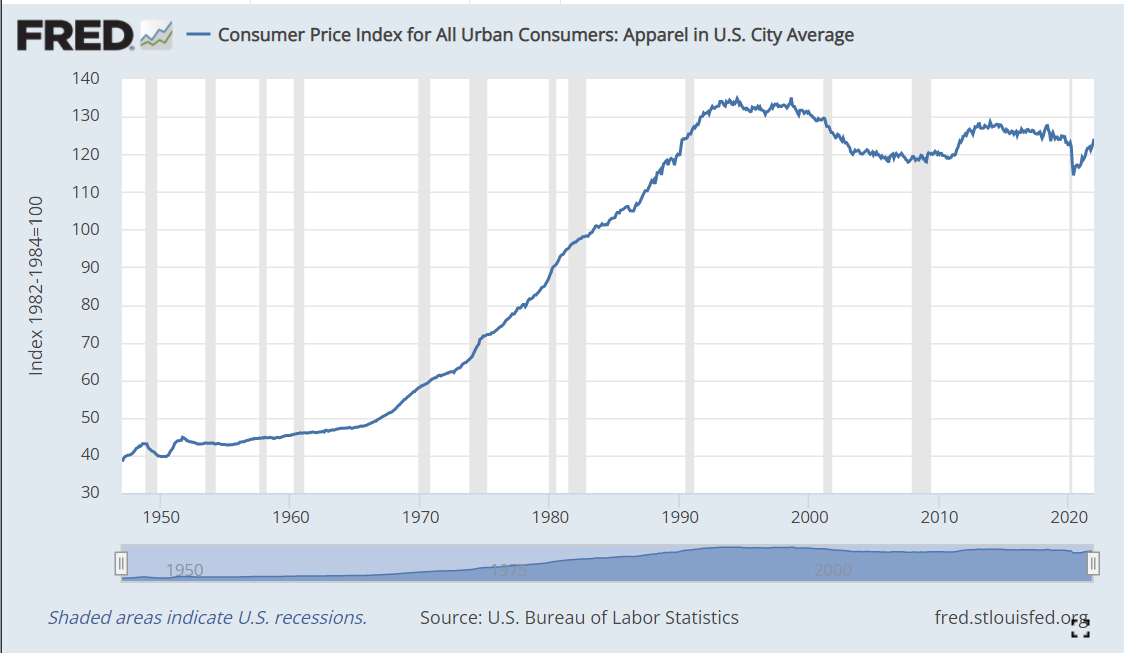

Some smaller areas have seen slow price growth. Apparel (3%) has declined in actual prices during this period. Recreation prices (4%) have grown by less than 1% annually.

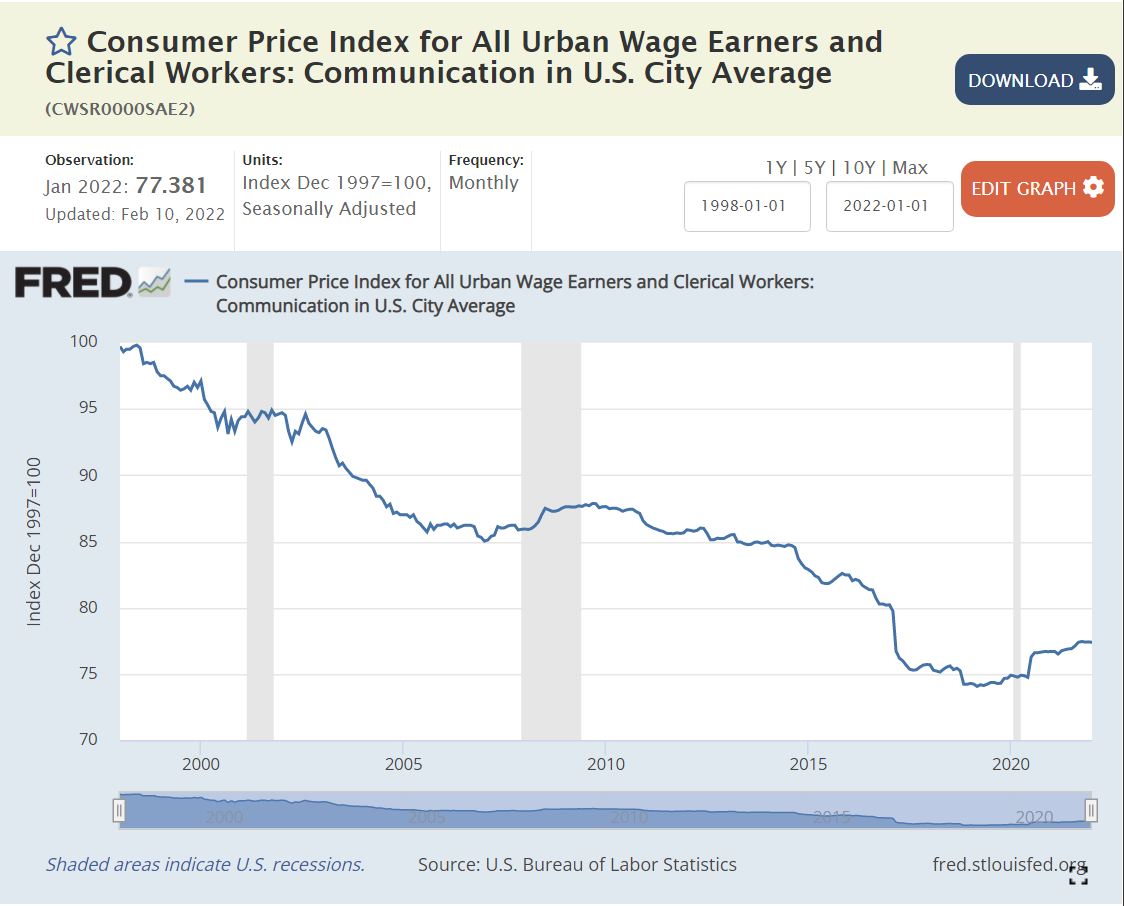

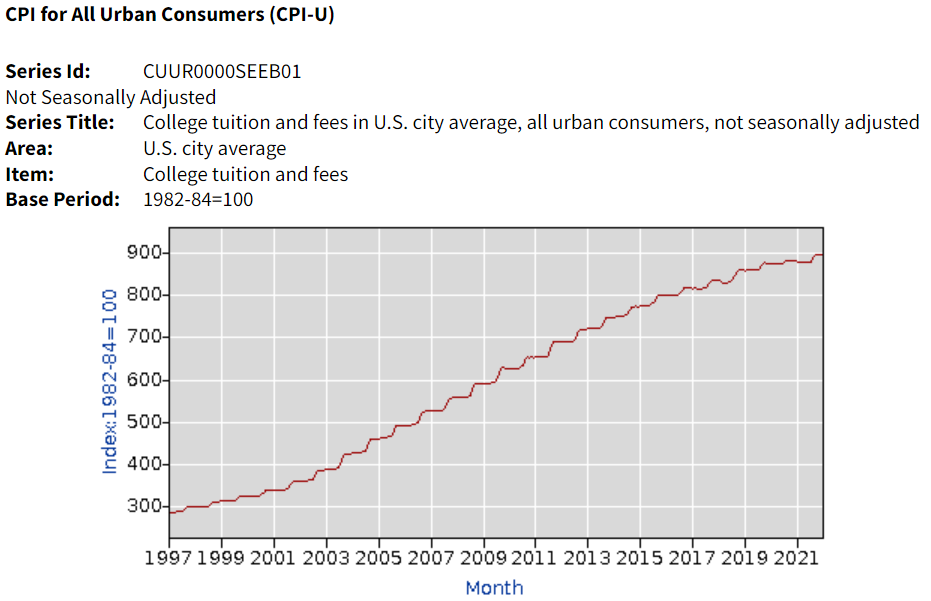

Education and Information (6%) prices have grown by 1% annually, but this category includes 3 very different subsectors. Information Technology prices have declined throughout the period. No simple 25- year summary is available. Communications prices have dropped by an average of 1% annually. Education prices have grown much faster, more than offsetting the decline in IT and communications prices. The Tuition, Fees and Child Care measure of prices increased by 165% and 171%, more than twice as fast as overall inflation, roughly 4% annually. College tuition (data not in Fred database) increased by 191% and 196%, about 4.5% per year.

The Other Goods and Services (3%) category mostly contains miscellaneous items that don’t fit cleanly in Housing or Food/Beverage. The category displays faster price increases (3.5%) on average due to the very sharp increase in Tobacco prices (taxes) which have grown 4-fold in 25 years (7%/year). Note that alcoholic beverage prices increased by a little more than 2% annually

Finally, Medical Care (7%) has grown by 116% – 125% during these 25 years, about 3.5% annually.

Overall goods prices have grown slowly and service prices more rapidly. Medical care and college prices stand out for their increases, while the price of housing/rentals is flashing warning signs.

Democritus in 300 BCE outlined a view of the world that has strongly shaped perceptions of reality to this day. All physical things can be reduced to smaller particles (atoms) that are irreducible. Everything can be “explained” by these particles.

The progress of science since 1500 has been shaped by a principle, called Occam’s Razor, which asserts that a simpler explanation is better than a more complex explanation. This is an untestable assertion, let alone a “law”, but the general progress of “science” and the “scientific method” since that time has reinforced this bias toward simple, rational, linear, logical explanations.

The progress of modern science was accelerated by Rene Descarte’s 3-dimensional right-angle coordinate system of space. It led to the belief that all space was composed of a substance called “the ether”. Physics experiments showed that this “materialist” view of space was inaccurate.

However, the progress of science reinforced the atomist, determinist, materialist concept of the universe through the end of the 19th century (1800-1899).

Early Modern Physics was Not Atomistic, Deterministic, Materialistic.

Newton defined concepts and equations for gravity and calculus. These were true breakthroughs, but perhaps misinterpreted as purely mechanical breakthroughs.

To this day, we can describe gravity, but we have no idea how it works through space and time and matter. Gravity does not reinforce atomistic concepts, it challenges them with the notion of force at a distance, affecting those atoms.

The next major progress in physics was in describing “waves”, as they flowed between atoms. Curvilinear, not linear. Waves have a role to play in mechanics, but they are more important in electromagnetic waves.

The equivalence of electricity and magnetism was one of the first true innovative discoveries in modern physics. Counterintuitive. Not atomistic. Not easy to understand. Not understood by most.

The role of heat or thermodynamics in physics and chemistry was one that allowed atomistic views to continue into the 20th century. With a plausible description of probablistic Brownian motion, the atomistic view remained ascendant through 1900.

Research into the “nature” of the atom eventually revealed that atoms were comprised of “particles”: protons, neutrons and electrons. However, the tiny electrons did not stand still. They rotated about the core of protons and neutrons. They also rotated at specific fixed distances away from the center of electrons. Or, they “tended” to appear at these 4 distances (SPDF) away from the center, based on a very complicated probability function. Atomistic, deterministic, materialistic concepts did not apply. This did not destroy the atomistic world view, I know not why.

Einstein did not like the new “quantum theory” of the universe that was described in his time. The inherently probabilistic nature did not resonate with him, even though the physics community adopted it.

Einstein was a “determinist” at heart and devoted his later life to finding a way to reconcile the very different “forces” of gravity, electro-magnetism and atomic forces. He failed to find a simple, deterministic explanation of the universe.

All of reality is based on probability. Quantum theory of physics says that particles are connected/entangled at a distance. We don’t know which reality is real until we observe it.

The very best modern physics theory that attempts to integrate gravity, electromagnetic forces and atoms is “string theory”. It has no experimental evidence, only logic to support it. A world of “many dimensions” is far removed from an atomistic world.

Unfortunately for those who longed for a solid, formal structure, Kurt Goedel proved in 1931 that any logical system worthy of the name of mathematics could not be proven from a finite set of obvious first assumptions. Mathematicians, physicists and other scientists had long looked at classical logic and geometry as a model for their work. Goedel showed that this was impossible. Again, the world should have digested the implications of this HUGE change, but due to the complexity of the arguments it was, and has been, largely ignored.

All modern scientists conduct experiments trading off alpha and beta risks. The hypothesis may be right, but stats say it is wrong. The hypothesis may be wrong. but the stats say it is right. This is an unavoidable conflict. No deterministic system can solve this.

Atomism, determinism, materialism is an attractive view of our universe. However, we have much evidence to reject this world view. Our world is based on multiple levels of reality and probability. Most of it is “logical” and consistent, but it cannot be simply reduced to a mechanistic base.

The British Invasion had not started. R&B dominated the charts (17). Leading men (10) and women (4) were still featured. A few foreign/novelty hits (4). Blues (2) and folk (4) songs were revived. A few rock (3) and C&W (5) songs. The Beach Boys’ sound was brand new (4).

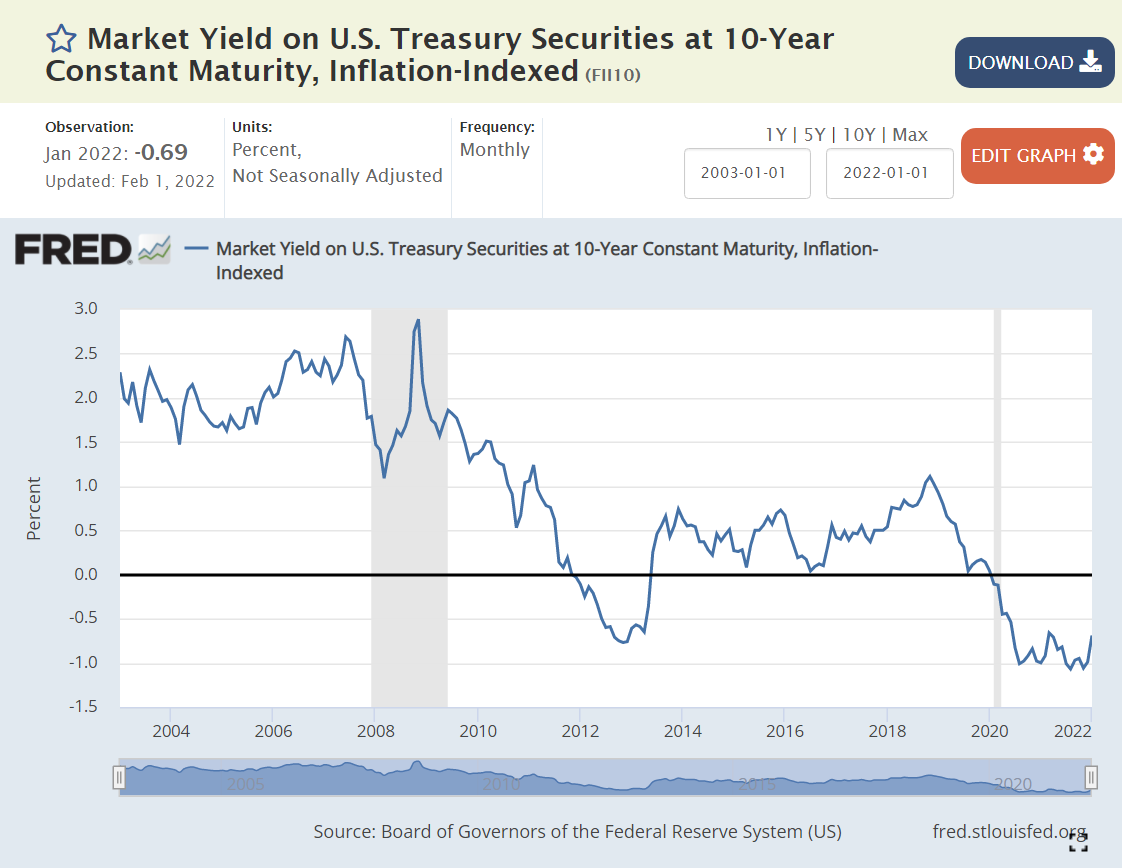

The “real” interest rate is the nominal interest rate minus the inflation rate. It reflects the “real” cost of borrowing. Prior to the “Great Recession”, 2% was a typical “real cost” of borrowing money. To entice lenders to lend, borrowers had to pay some “real” amount extra per year, 2%.

The Federal Reserve did what it could to “ease” monetary conditions and lower interest rates to offset the negative impact of the Great Recession in 2008-9.

By the end of 2011, real rates were ZERO or negative. In other words, the Fed went too far. By June, 2013, rates returned to positive territory, but only reached 0.5%, where they remained through the end of 2017, despite president Trump’s complaints that the Fed was constraining the Trump economy. Monetary policies were “easy” for a very long 7-year period.

By May, 2019, real interest rates were back to just 0.5%, having reached a peak of just 1% for 3 months at the end of 2018. With further “easy” money policy, real rates dropped back to ZERO percent by August, 2019. The economy was now 9 years into recovery. Interest rates should have been higher.

The Fed found new ways to “ease” monetary policy as the pandemic struck in 2020. Real interest rates dropped to -1% and stayed there. Monetary policy has been “easy” for more than a decade. Time for inflation. “Too much money chasing too few goods”. “Inflation is always and everywhere a monetary phenomenon”.

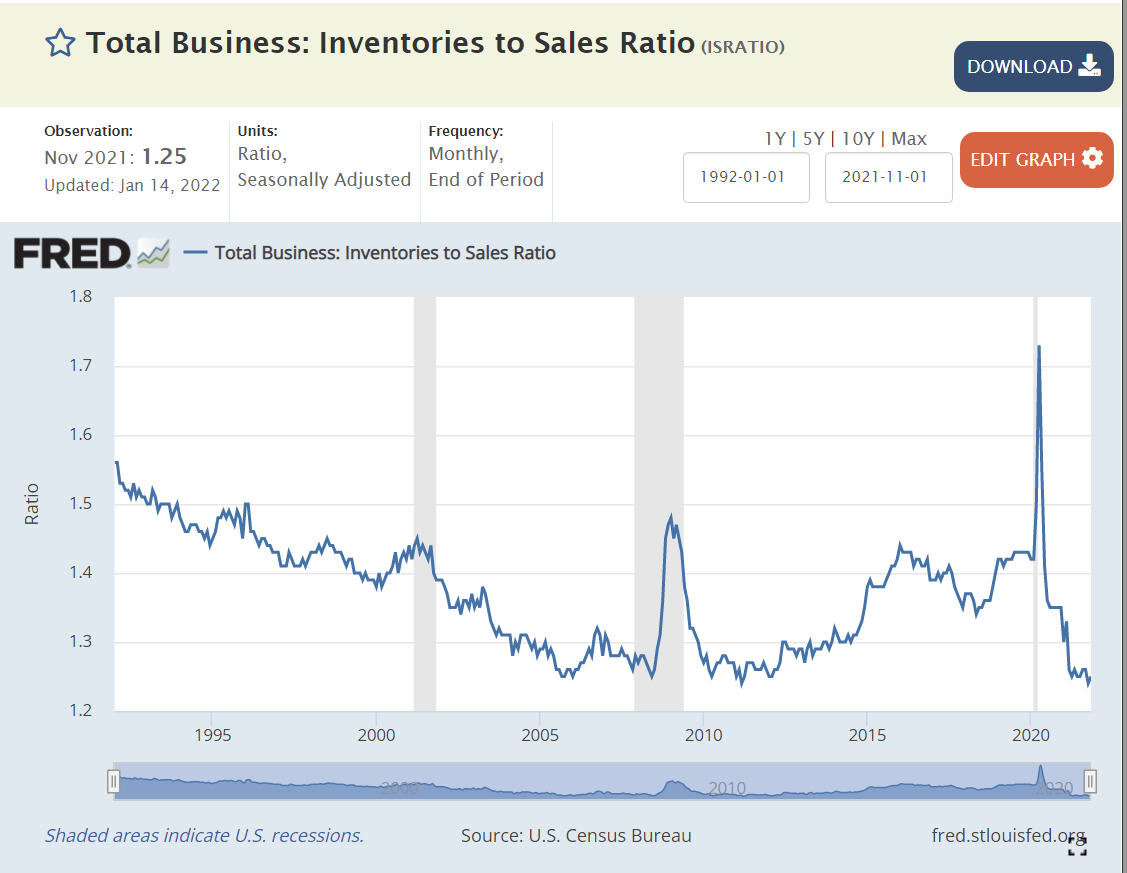

Supply Chain Disruption

The recovery has been faster than anyone expected, but most critically, with consumers less eager to buy “in-person” services, they have greatly increased their purchases of goods. The modern US economy relies on imports and modern manufacturers and retailers hold lower inventories to buffer changes.

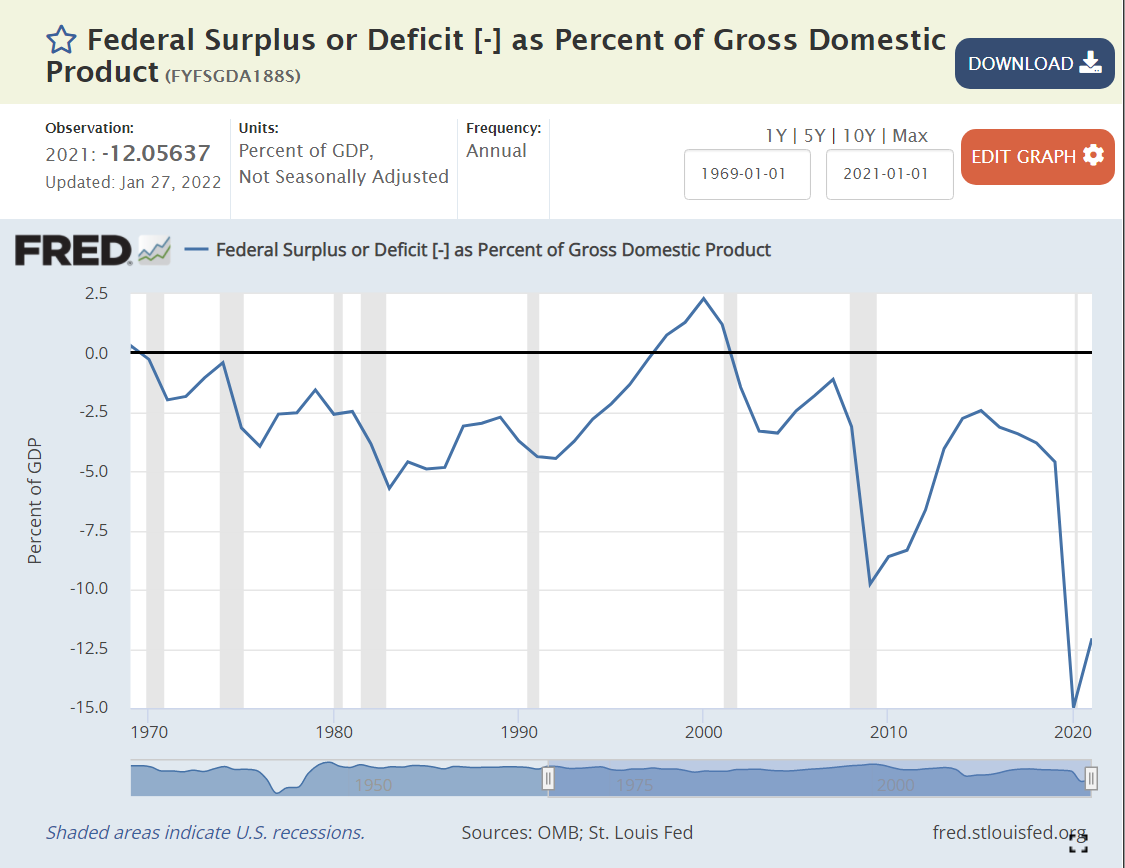

Standard macroeconomic theory focuses on aggregate demand versus aggregate supply as the key driver of output, unemployment and inflation. When total demand grows faster than remaining excess capacity of total supply, inflation results. The biggest driver of changes in aggregate demand is the level of government spending (demand) minus government taxation (reduces demand).

Historically, various pressures have kept the federal budget deficit between -3% and +3% of GDP, allowing the government to buffer change in private demand through the business cycle. The large drop from -2.5% to -5% in 1979-82 was a factor that contributed to the last major round of US inflation. A similar decline from -2.5% to -4% in 1989-91 increased inflation, but not on such a large scale. It also served to convince President Clinton and congress to reduce the deficit to ZERO by 1997 and run a surplus for a few years.

The 2001 recession caused a 2.5% decrease in this ratio, from a surplus to a deficit. Bush tax cuts, foreign wars and congressional agreement lead to deeper deficits at 3.3% in 2003-4, before some recovery to -1% in 2007, prior to the Great Recession.

Bush, Obama and congress agreed to spend more to fight the Great Recession, pushing the deficit to a worryingly low -9.8% in 2009. There was no agreement on a second major round of spending, so the deficit improved a bit to -6.6% by 2012 and then to a more reasonable -2.5% in 2014-15. Instead of continuing to improve with the economic recovery, it fell a little, to 3.1% in the last year of the Obama economy.

President Trump’s first order of business was to enact “job creating” tax cuts. Unfortunately, the desired boost to economic growth to fund these tax cuts did not occur. The budget deficit increased from 3.1% to 4.6% of GDP, as the economy reached a record long recovery period of a full decade.

To address the pandemic, congress and Trump agreed to spend money to protect the economy and workers, leading to very large budget deficits of 15% and 12% in 2020 and 2021, respectively. Too much aggregate demand for the level of aggregate supply, so we have major inflation.

Summary

Easy money, easy fiscal policy and a 20% increase in demand for goods leads to major inflation. Like a frog getting boiled as a pot slowly warms up, we became complacent based on the apparently “just right” conditions of the late teens (2012-19). The federal budget deficit needs to get back above -5%, real interest rates need to become positive and consumers need to rebalance to consume more services and less goods. I don’t think we’ll see 7% inflation for 2022, but it looks like 4-5% is a good bet. Hold on.

Politics

Biden deserves a good share of responsibility for the government spending budget deficit, as he was seeking to make it even larger. I give him a “pass” on consumer demand for durable goods since it mostly occurred before he started. I also give him a “pass” for the loose Fed monetary policy which has been going on for a decade or so. He was wise to reappoint the Fed chairman, who I believe will raise interest rates as needed to get the real interest rate back to a proper level. In the meantime, Biden will pay politically for higher inflation, which has a “real” impact on the wallets of voters.

The nominal/actual average price of clothing today in the USA is 3% LOWER than it was 30 years ago, in 1991!!! Meanwhile, the overall consumer price index (CPI), has more than doubled (+106%). So, the price of clothing, relative to overall prices, has dropped by a mind-boggling 53% in the last 3 decades!

This is on top of the 37% real reduction in prices from 1970 to 1991.

From 1960 to 2021, the real reduction in clothing prices is a full 71%. More than two-thirds.

Ronald Reagan taunted Jimmy Carter with this question to voters in the 1980 debates. It helped him win.

Twelve years later, James Carville helped Democrats return from the political wilderness in 1992 with his advice to Bill Clinton that “it’s the economy, stupid”.

Politicians have used various measures, from unemployment to inflation to the “misery index” to jobs created to productivity to the stock market, to promote their success and detract from their opponents.

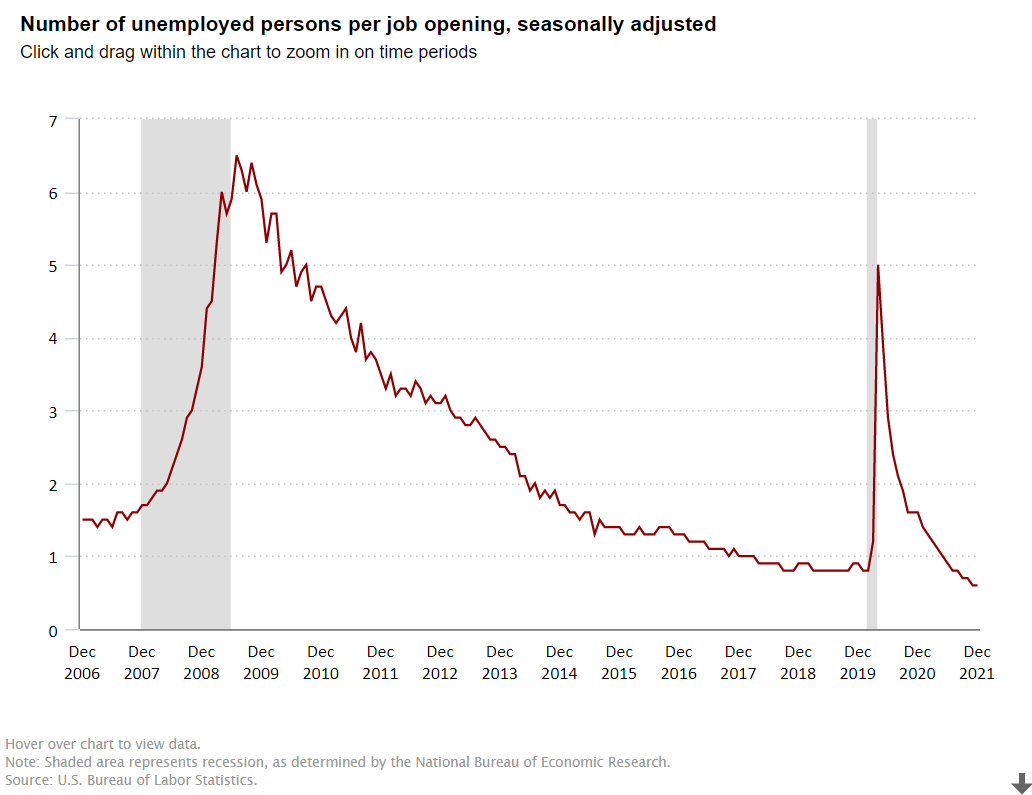

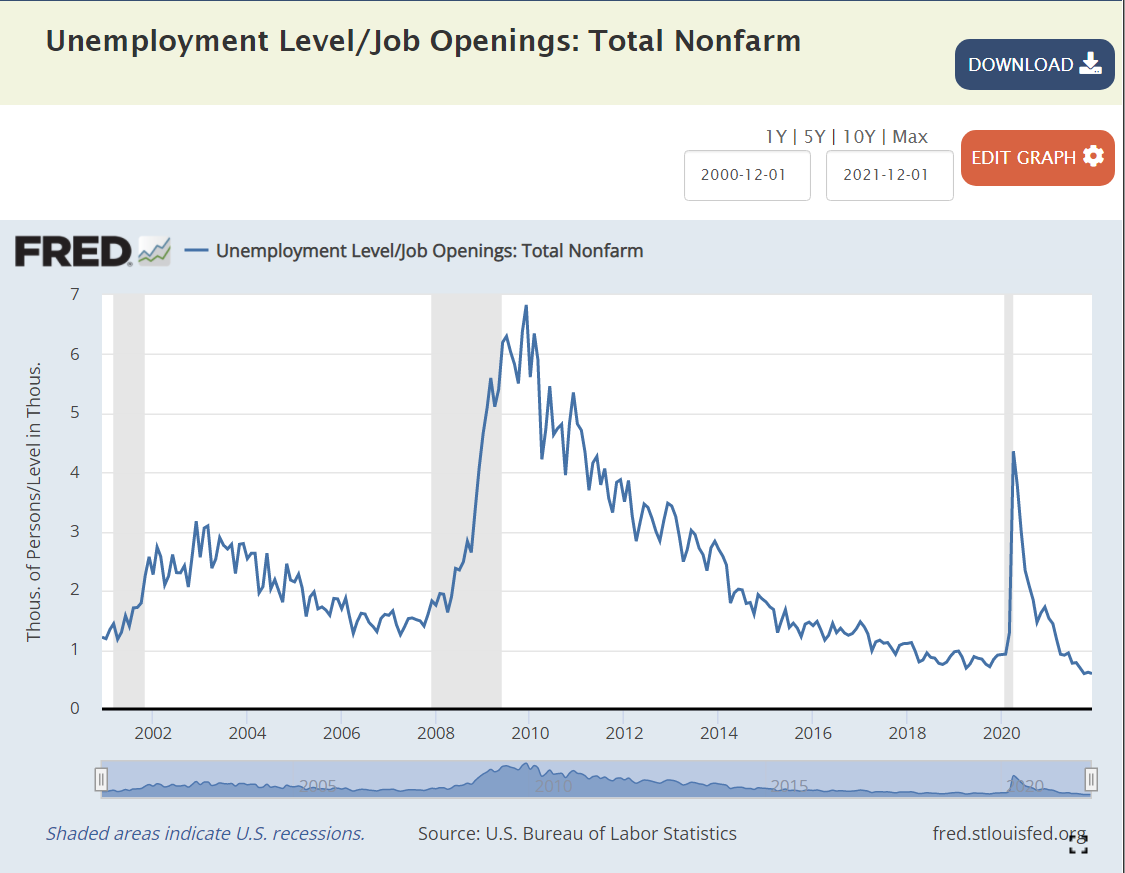

I want to focus on one measure, the ratio of the number unemployed to the number of job openings, to highlight the strength of the American economy in the last dozen years.

The Bush economy was widely criticized for its “jobless recovery” following the economically healthier Reagan and Clinton presidencies. The presidency started at close to 1 unemployed person per job opening. The recession pushed this up to 2.5x and then 3.0x. In labor market terms, this is a huge difference. At 1:1 or 1.5:1, unemployed workers expect to be re-employed quickly. At 3:1, some may enter the dark days of the “long-term unemployed”. After 3 years, the economy DID recover to 1.5:1, but it was unable to improve further. The “Great Recession” was a brutal job killer, pushing this measure of labor market tightness up four-fold, from 1.5X to more than 6X before its peak in the first half of 2010, as Obama and congress and the federal reserve bank wrestled with the situation.

Obama: Recovery and “New Territory”

Between April, 2010 and April, 2012, the economy cut this ratio in half, from 6x to 3x, a very solid performance. It took 3 years, until April, 2015, to complete the next 50% reduction, from 3x to the historically “very solid” 1.5X. The economy continued its growth for the next 2 years, but at a slower pace, reducing this ratio to 1.3X.

Trump: Even Better

The Trump economy continued to improve for the first 18 months of his term, reducing this ratio from 1.3X to 0.8X by September, 2018. This was a time of record low unemployment and economists recalculating their standard of “full employment”. While the economy continued to grow, the unemployment rate continued to decline and the stock market continued to climb, THIS measure had reached its minimum before the 2018 mid-term elections. It remained steady at the very positive level of 4 job seekers for every 5 jobs (0.8) for the next 17 months, until the pandemic disrupted everything. The ratio quickly shot up to 5X, not as high as the 6X that Obama faced, but very high. It quickly recovered to 1.4X by the end of Trump’s term. This was partly job recovery and partly fewer job seekers, but it was an amazing recovery in historic terms. Recall that 1.5X was “a good as it got” during George W. Bush’s presidency.

Biden: Even Better, Again !

In the first 6 months of the Biden presidency, this ratio dropped from 1.4X back down to the prior record level of 0.8X. Yes, by July, 2021, there were 5 jobs available for every 4 job seekers. This was as low as the ratio had previously fallen, even as the Trump economy piggybacked on the Obama economy and continued its extraordinary run. The ratio continued to fall in the next 6 months to 0.6X, an unheard-of level. 5 jobs for every 3 job seekers. It’s “no wonder” that voluntary job quits are at unprecedented levels. For, perhaps, the first time in American history, “everyone who wants to work, can find a job”. Whether you are right or left, Dem or Rep, this is “good news”. This is “great news”. Wages for the “bottom 20%” are rising in real terms. Income inequality is declining, a bit. The economy seems to be able to digest this new condition. And, the economy is not done growing, innovating, creating businesses, creating jobs, exporting, etc. About 2% of Americans are likely to be attracted back into the workforce in the next year or two, keeping the headline unemployment rate from going much below 4%, but pushing US real GDP growth to 4% in 2022 and close to 4% in 2023.

Summary

The “Great Recession” and the “once in a century pandemic” have been unable to disrupt the ongoing progress of the American economy and labor market. As a nation, IMHO, we have cultural and political challenges, but we “aught” to appreciate the power of the American economy to move forward.

Not many French language songs or artists have “crossed over” to the US pop charts in the last 80 years. I poked around youtube to find 50 worth a listen. Enjoy!