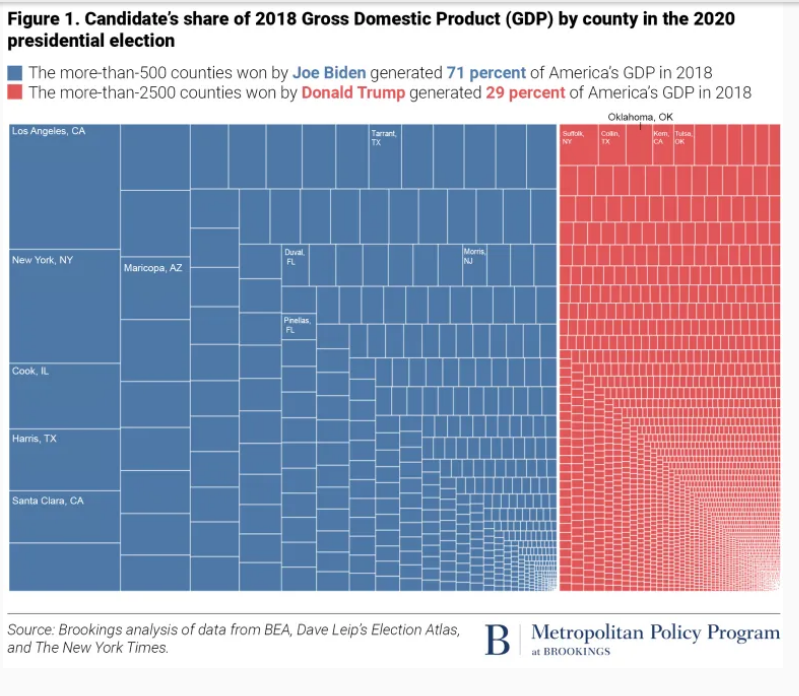

Just 6 of 50 states have split US Senate representation. WV, OH, PA, ME, WI and MT account for slightly less than 10% of the 2021 US GDP.

Republicans have 2 Senators in 22 states, which account for $6.6T of GDP.

Democrats have 2 Senators in 22 states, which account for $10.8T of GDP.

Splitting the GDP for the 6 split states 50/50 results in $7.5T in Republican states and $11.7T in Democratic states. The Democratic states have 57% greater GDP in 2021.

The Democratic percentage advantage in 1997 GDP per state is identical. Republican states produced $4.5T while Democratic states produced $7.1T. Between 1997 and 2021, Democratic and Republican states grew at equal percentages. In dollar terms, Democratic states added $4.6T, while Republican states added $3.0T.

Percentages are difficult to digest. One way to compare the 2021 GDP of the two parties is to use “paired comparisons” and then examine the remaining non-paired states. 13 roughly equal pairs can be identified. WY-VT, AL-RI, ND-DE, ID-MA, KS-NV, MS-NH, AR-NM, SC-OR, LA-AZ, MO-CT, TN-MN, IN-MD and NC-MA.

The remaining Republican states have lower $GDP figures but can be mapped to equal $GDP Democratic states. IA+NE+SD=CO. FL+TX=CA. KY+AL+OK+UT=IL.

This leaves 6 states that represent the $4.5T (57%) Democratic state advantage: Michigan ($0.5T), New Jersey ($0.6T), New York ($1.5T), Virginia ($0.5T), Georgia ($0.6T) and Washington ($0.6T).

The Post-Trump Republican Party is distinctively different, representing a broader share of the American geography, but a smaller share of its income, production and diversity. This split reinforces the polarizing tendencies of recent decades, making attempts to find “common ground” at the national level more difficult.

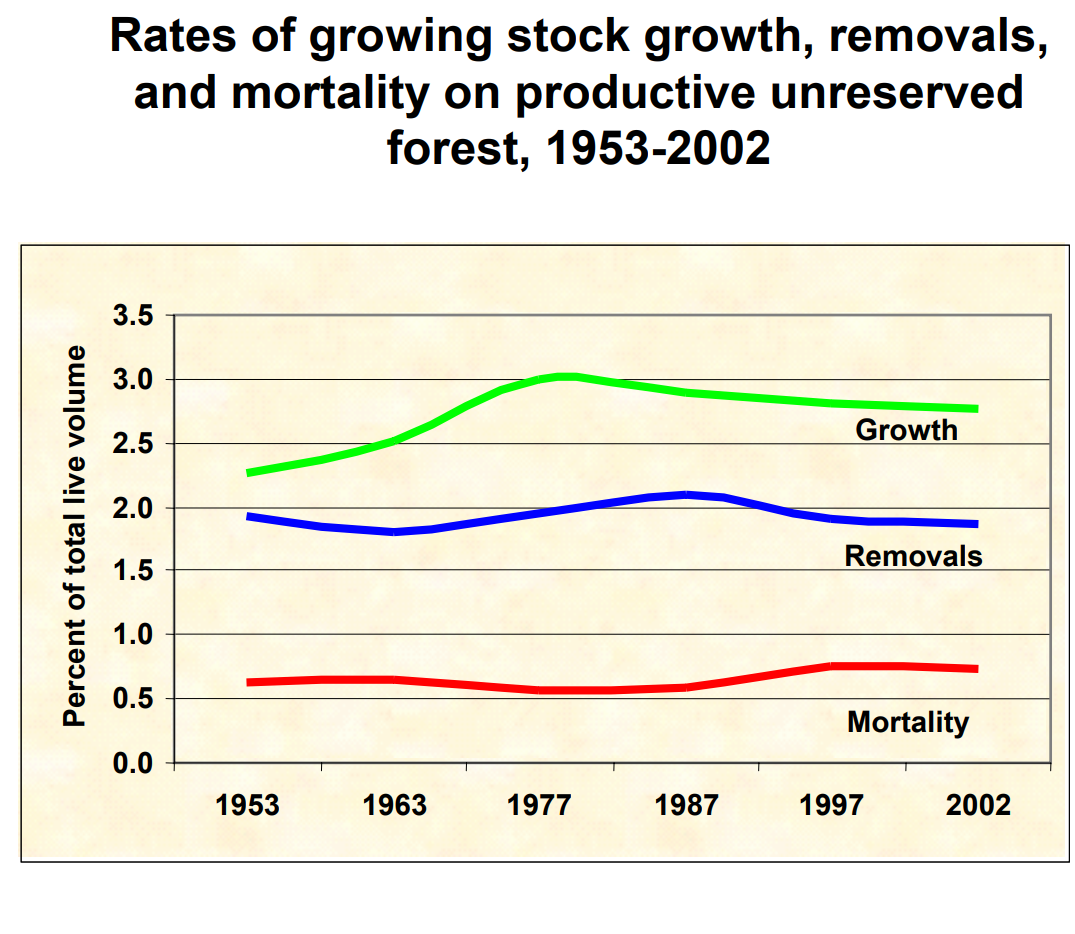

“Many challenges are associated with drought, wildfire, invasive species, and outbreaks of insects and disease—all made worse by climate change. Warming temperatures mean more energy in the atmosphere, which is consistent with severe weather events, such as floods, tornadoes, blizzards, ice storms, and hurricanes.”

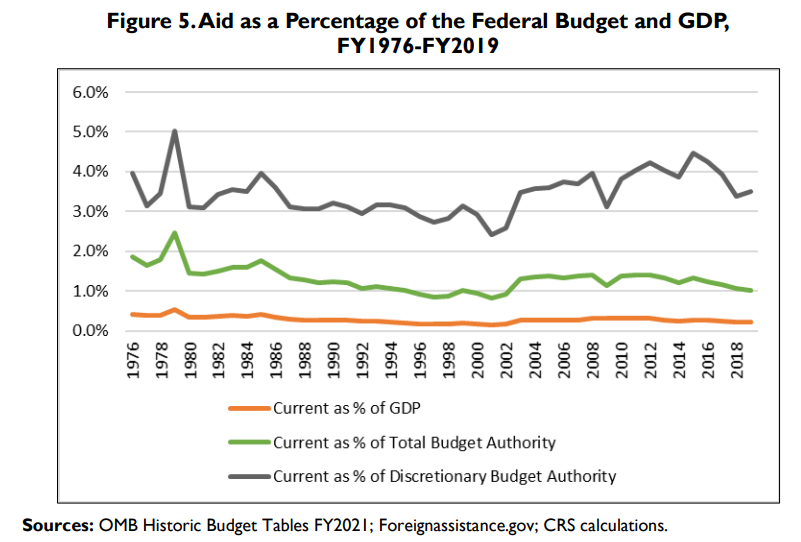

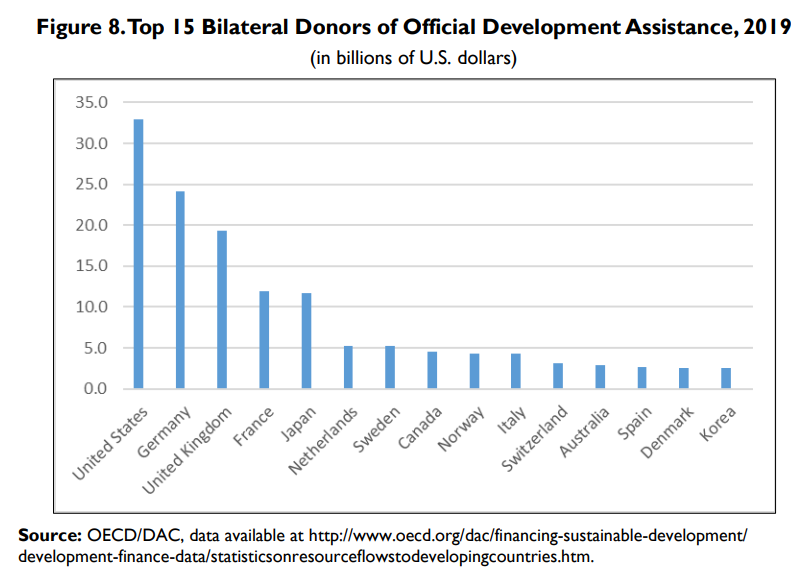

Africa 25%. Middle East 25%. Afghanistan $5B, Israel $3B, Jordan $2B, Egypt, Iraq, Ethiopia, Yemen, Colombia, Nigeria, Lebanon $1B each. Top 10 $16B, one-third of total.

Criticisms of Foreign Aid

Limited evidence that specific country investments provide political returns

Limited evidence of anti-terrorism campaign effectiveness (counterexamples)

Weak administrative structure and oversight at all levels

Direct evidence of individual country economic growth due to aid is limited

Some autocratic governments have benefitted from aid

Some aid is diverted to corrupt governments and individuals

Specific high priority countries have provided weak returns (Egypt, Pakistan, Afghanistan, Iraq)

Higher returns could be gained from investing in Western Hemisphere, Eastern Europe.

Health measures, disease rates, lifespans. Global health. Economic development results globally and in individual countries. US trade benefits from developing trade lanes. Global education. Increased number of democracies, commitment to mixed capitalist economies. Lower cost of defense. Terrorism activities thwarted. Improved strength of US alliances. Improved flow through NGOs, multilateral organizations improves effectiveness. Dollar allocation provides US policy leverage.

6-month time limit. A dozen or less bipartisan dignitaries. Retired ambassadors, investors, CEO’s, federal reserve presidents, etc. Make Mitch Daniels the chair.

Assign 2 projects. One to cut government waste. The other anti-inflation policies. No more than a dozen recommendations in each half. Presented to congress for simple yes/no vote, without major amendments allowed.

2. Spend Less Government Money

Fiscal spending is too expansionary for the current situation. Back off. Reduce infrastructure spending for now, spend it in the next recession. Reduce marginal defense programs that only have political reasons. Cut state government spending by 3%, which is budgeted to increased by 9%.

Increase immigration to improve labor supply. Cut tariffs to reduce supplies costs. Lean on local regulators to reduce zoning restraints and one size fits all building codes. Strategically require a higher share of affordable housing and multifamily permits annually in each metropolitan region. Phase-out the mortgage interest tax deduction for second homes.

Loosen regulations for 5 years to encourage increased “all of the above supplies” energy through drilling, coal, oil and nuclear. Suspend federal gas tax for 3 years. Negotiate oil price minimums/maximums between US/Europe/Japan and OPEC.

Reducing inflation is a complicated policy area. The solutions proposed by “experts” are rarely politically appealing. Competing political parties hesitate to provide “wins” to the other. However, 8% inflation after a 2-year pandemic while the US faces Russian war actions is a “national emergency”, worthy of an FDR like approach to “try a few things”. It is an opportunity to overcome individual industry opposition to things that make sense for the country. It is an opportunity to try some left and right solutions.

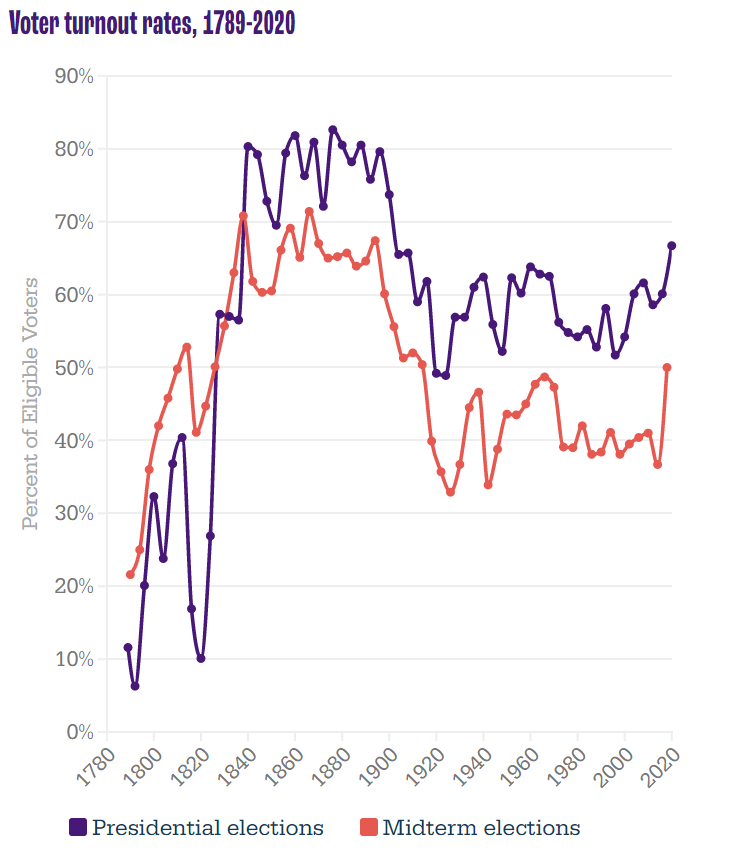

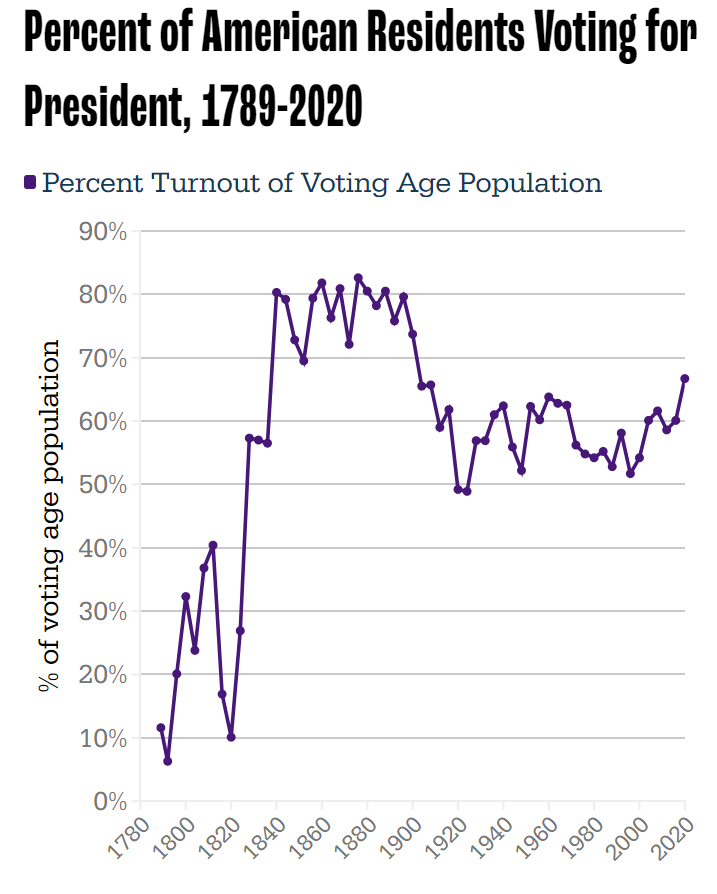

Setting aside turnout ratios, the growth in actual voters has been strong for a century. 40-48M voted in FDR’s elections. Kennedy and Nixon fought over 69M voters. Clinton and Bush, Sr. attracted 105M voters in 1992. But, Biden vs. Trump shattered records with 158M casting ballots.

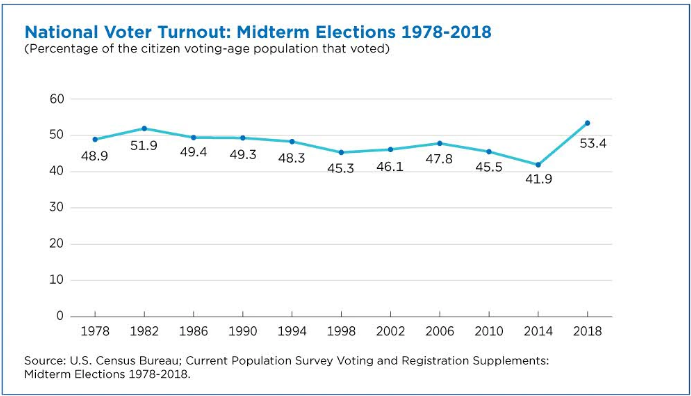

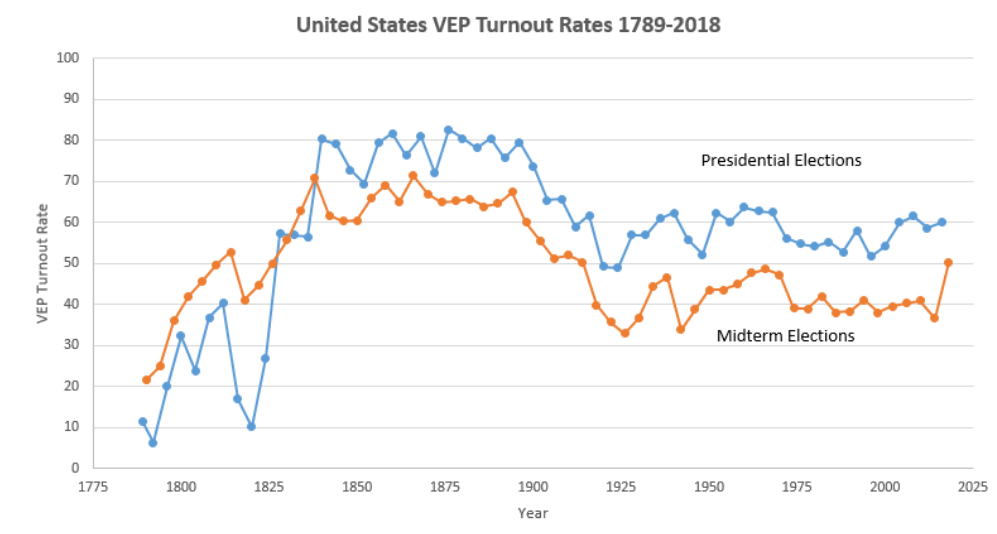

Midterm voting rates (as % of eligible voters) soared at 65% in the 19th century. They dropped to 50% at the start of the 20th century and then down to 45% for most of the 30’s to 60’s. They settled down to 40% thereafter. The 2018 election reached 50%, a full 13% points above the all-time low in 2014.

The slightly different measure, percentage of voting age population, shows the same pattern. 49% voting from 1978-94. Just 46% from 1998-2010. Record low of 42% in 2014, followed by an 11%-point climb to 53% in 2018.

Younger voters increased their turnout by 14 points (18-44), while older voters increased by a solid 8%. High school or less educated voters increased turnout by 7 points, while college educated voters added 12 points.

Long-term presidential and midterm voting (% of eligible voters) follows the same pattern. 80% turnout in the 19th century, dropping to 59% by 1912, then averaging 60% in the 30’s to 60’s. Further decline to just 55% for the 70’s-90’s. Minor increase to 60% in the oughts and teens, followed by 67% in 2020.

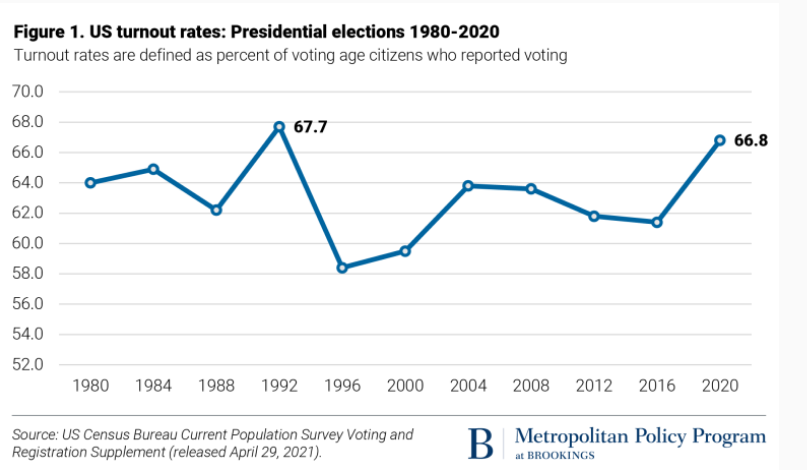

The more recent percent of voting age population shows 64% from 80-88, a one-time spike to 68% in 1992, decline to 59% from 96-200, slight increase to 61% for 04-16, and then a big jump to 67% in 2020.

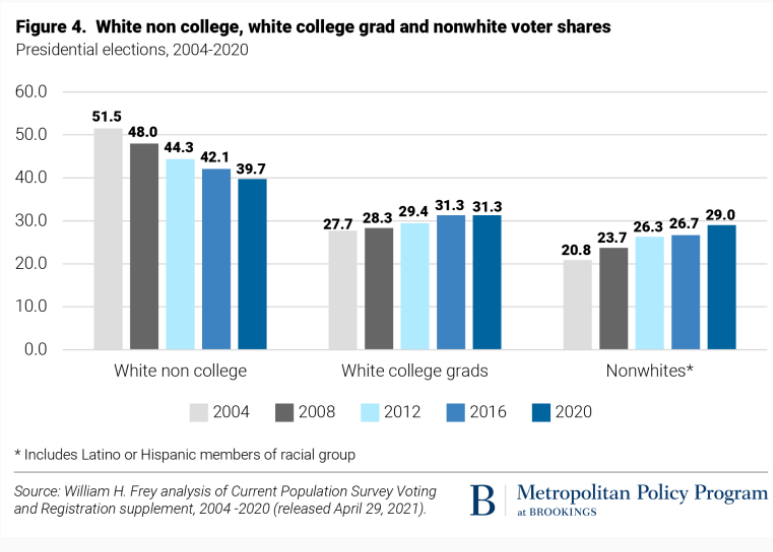

Turnout was up in all categories, but especially among Asian, 18-29 year olds and white non-college educated populations.

Voting by all racial groups of 18-24 year-olds was up significantly.

The two measures (% of eligible voters and % of population) track closely. The “election project” numbers show VEP at 63% from 1952-68, declining to 58% for 72-00, increasing a little to 61% for 04-16, before spiking to 66% in 2020.

Income really matters for voter turnout, with rates ranging from one-third to one-half to two-thirds. With increased lower income support for the Republican party, this is less of a partisan issue today.

Since 1969, Democrats have argued that demographic trends will overturn Kevin Phillip’s description of the Emerging Republican Majority. This remains a hotly debated topic.

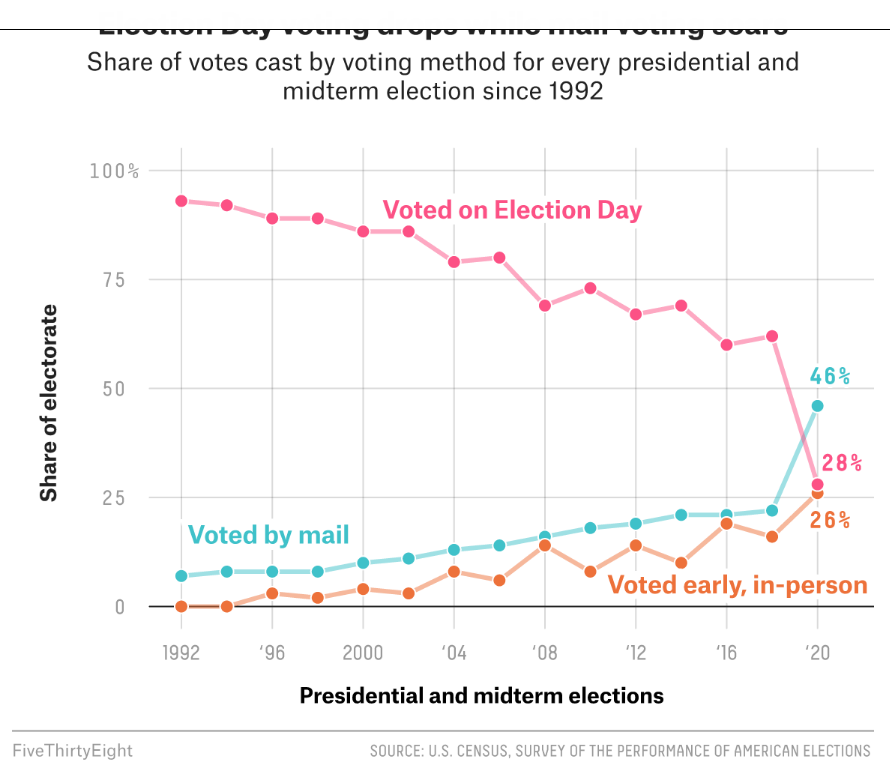

Election day voting decreased in 2018 and 2020 as mail and early, in-person voting increased. Many commentators claim that this change is a large driver of the increased turnout levels.

{kind=link}

{kind=link}