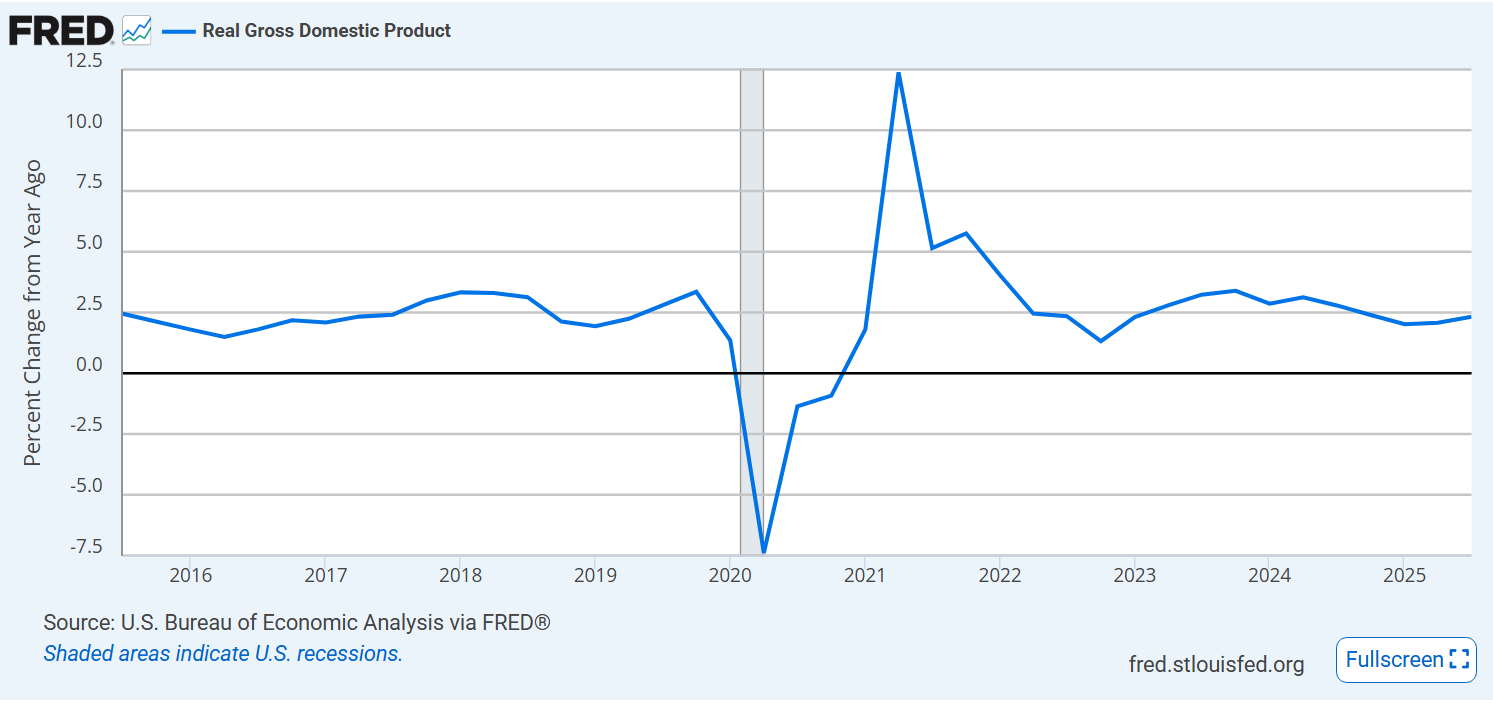

Overall, at the same core 2.5% growth rate seen for the last decade.

Labor productivity growth down a bit from the pandemic recovery bump.

Median wage growth remains at 2%, down a bit from pre-pandemic 2.5%.

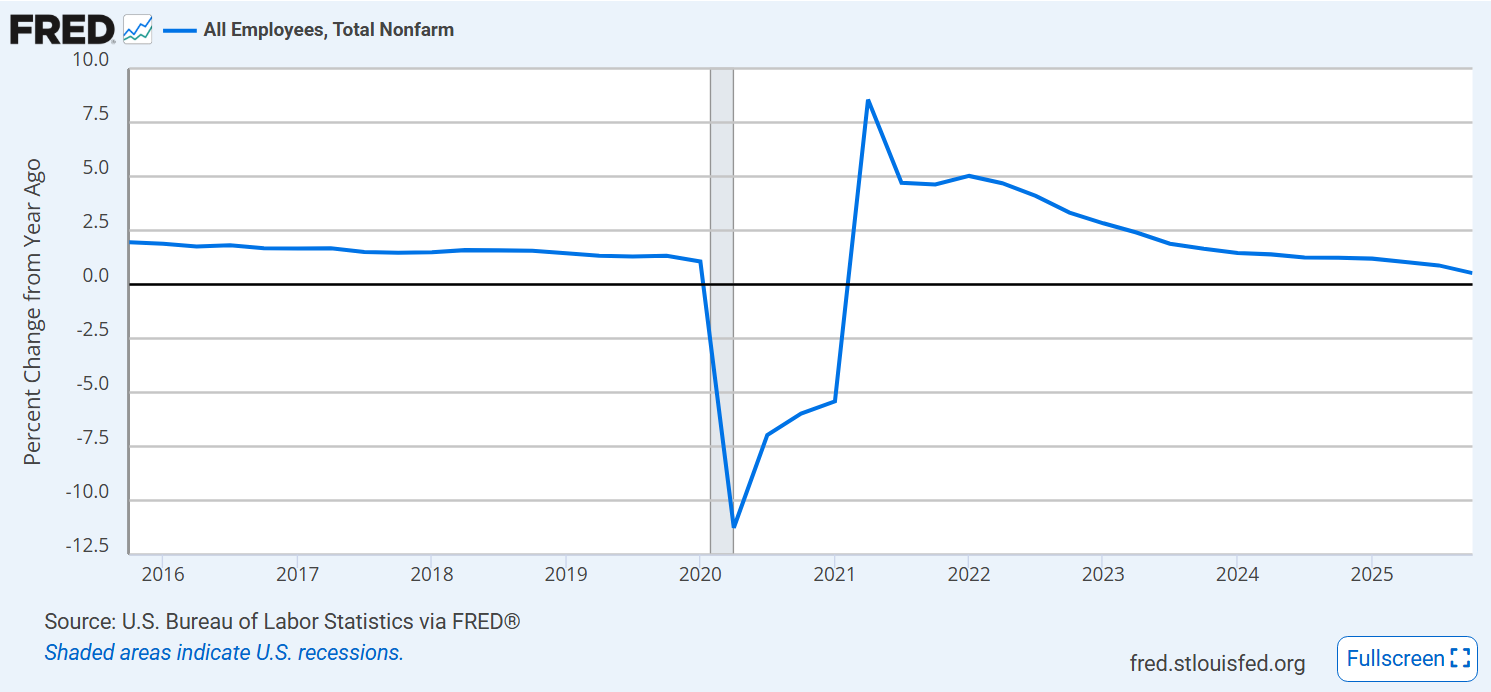

Job growth is very weak. Typically, this indicates a coming recession, but the reduction of the immigration labor supply makes historical comparisons difficult.

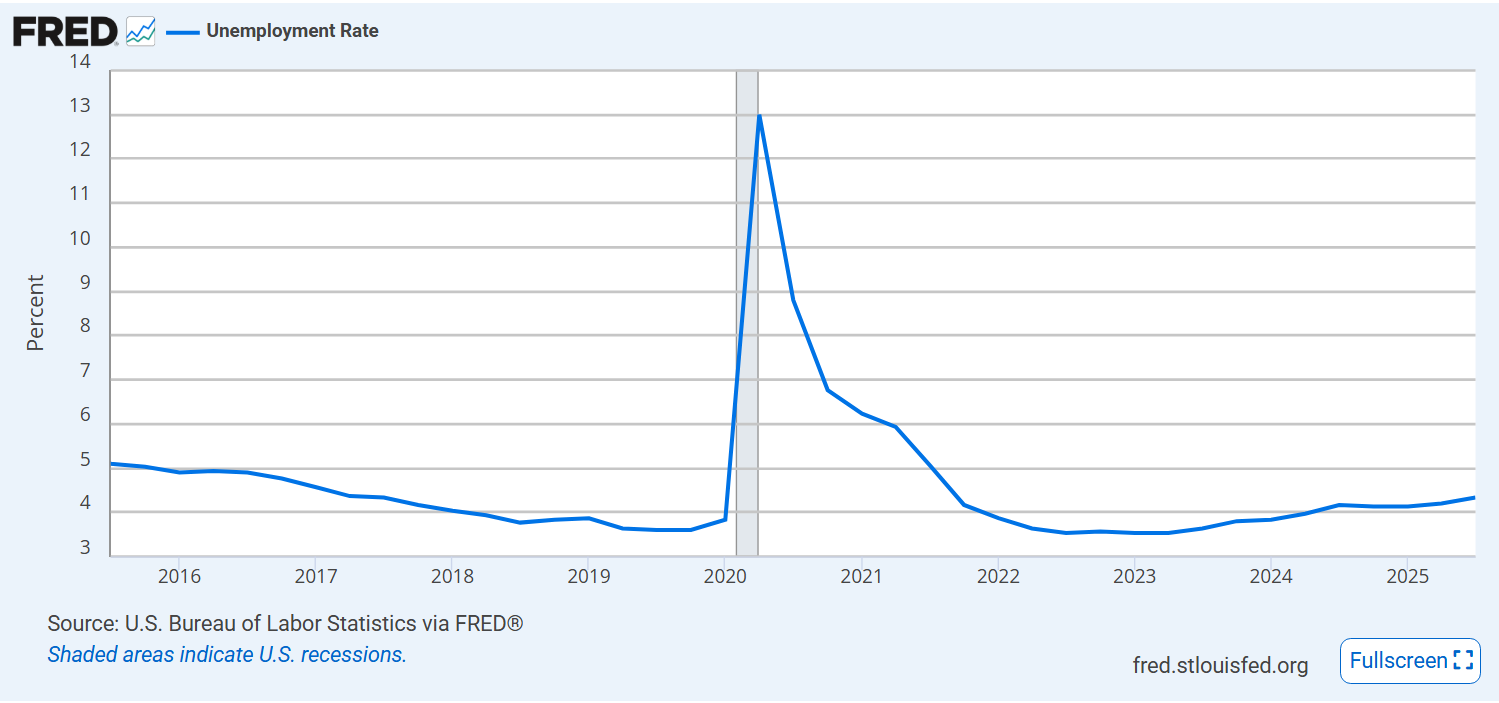

Unemployment rate remains at historically low 4.5% but it has been increasing for more than 2 years.

The “underemployed” rate shows the same relative level and trend.

Labor force participation hit record levels after the pandemic and has remained there.

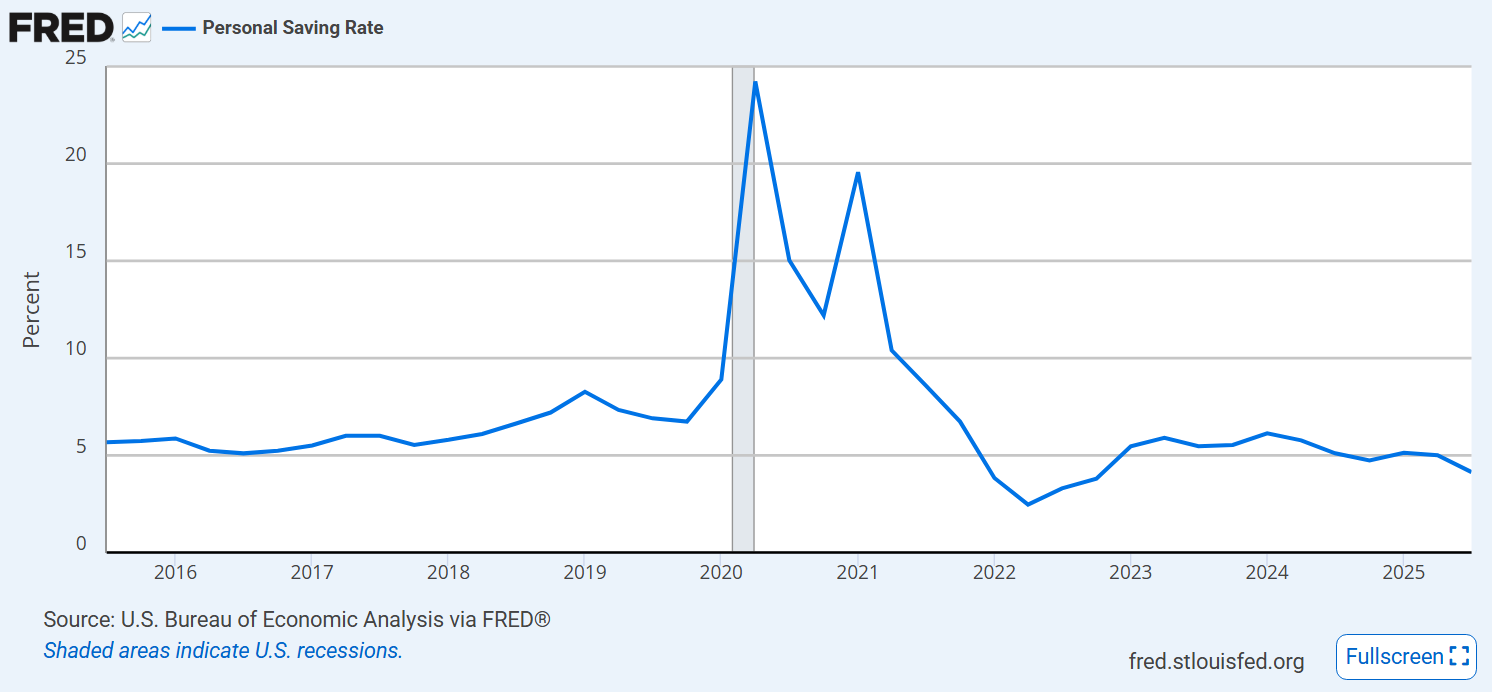

The personal savings rate is low, a bit below the pandemic and trending slightly downward.

Mortgage rates remain elevated, around 6.5%.

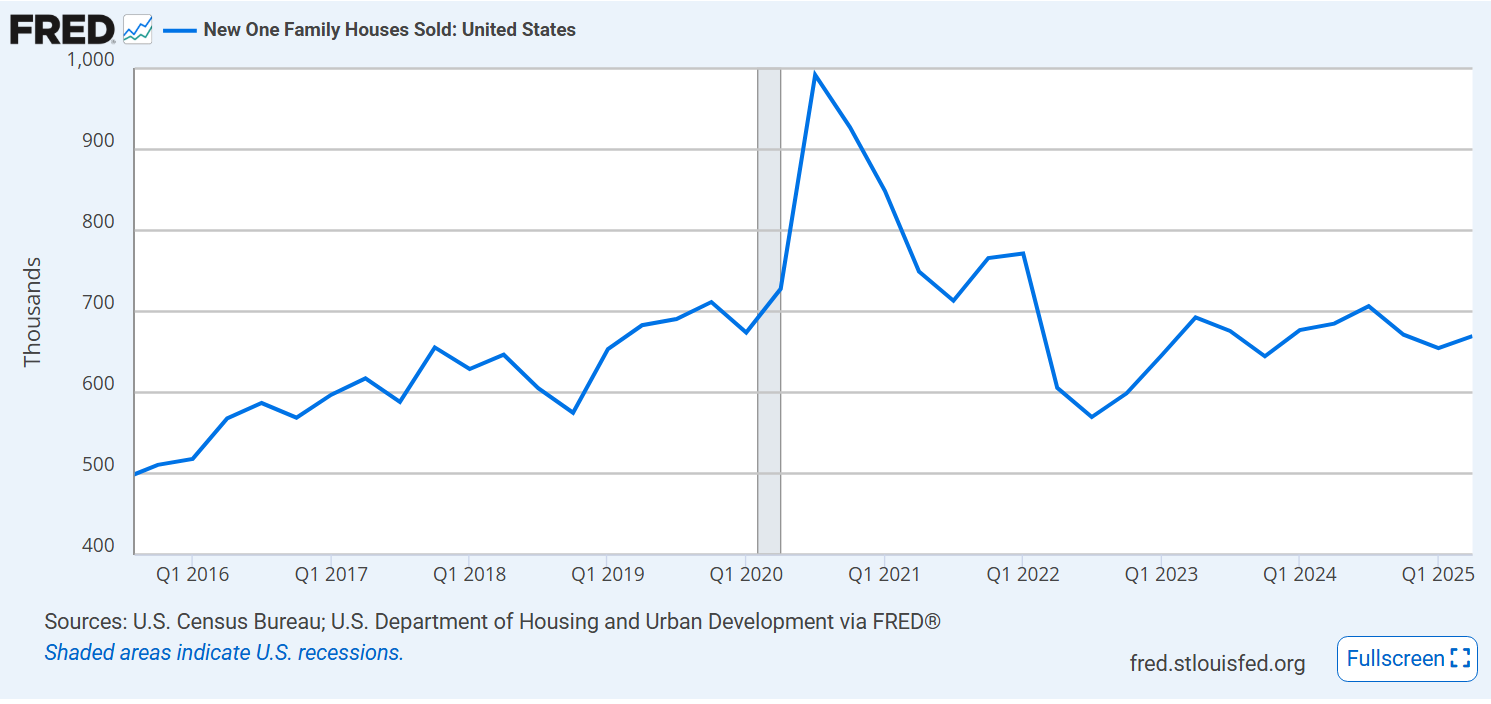

New home sales are pretty stable, at pre-pandemic level.

Housing prices jumped from $320,000 to $440,000 after the pandemic. They have fallen back by 5% in 4 years.

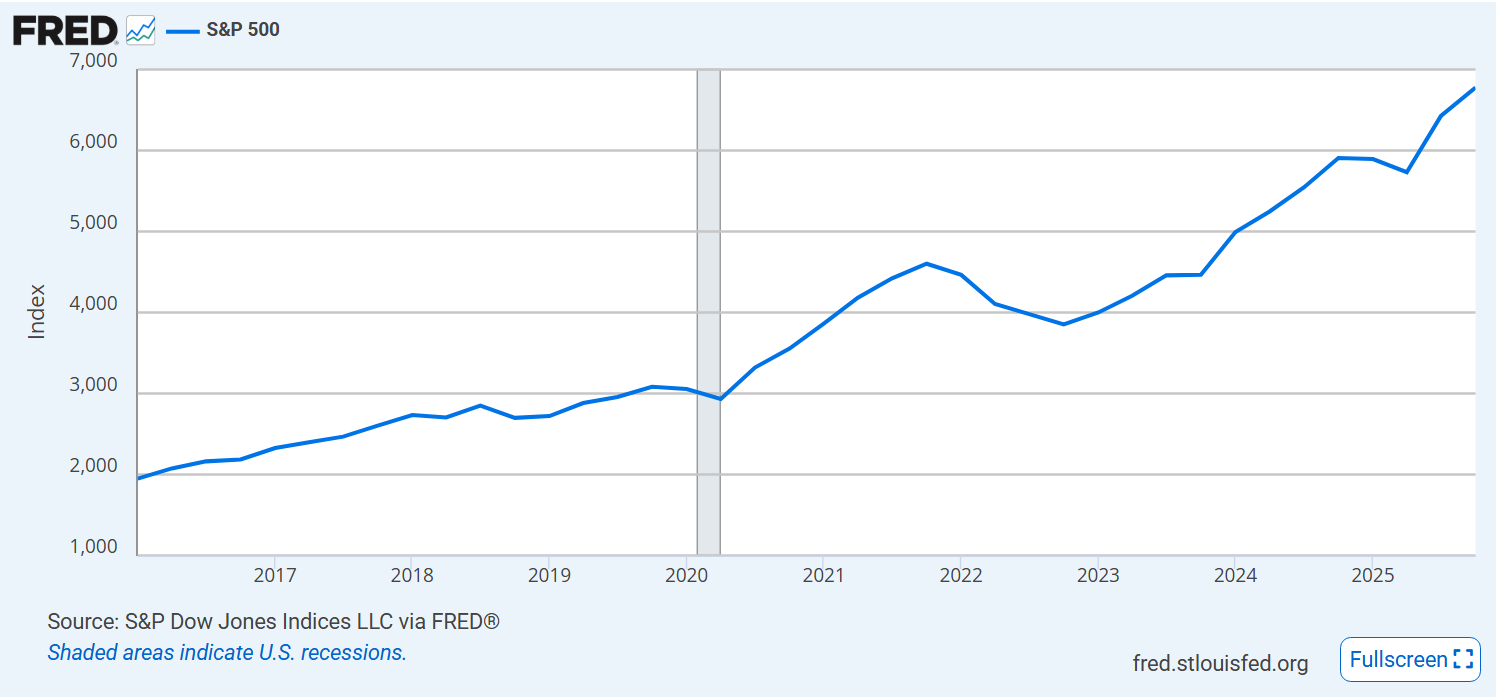

The US stock market continues to climb.

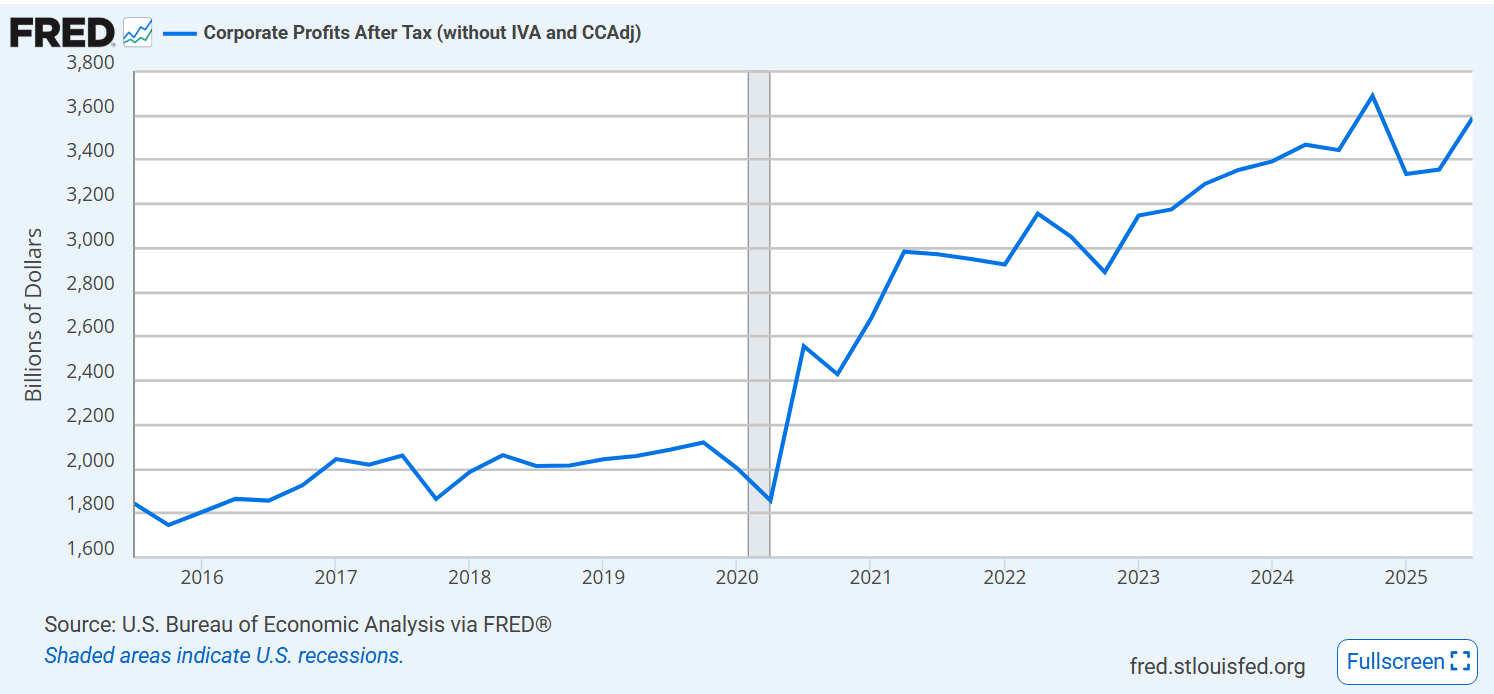

Corporate profits have roughly doubled since before the pandemic.

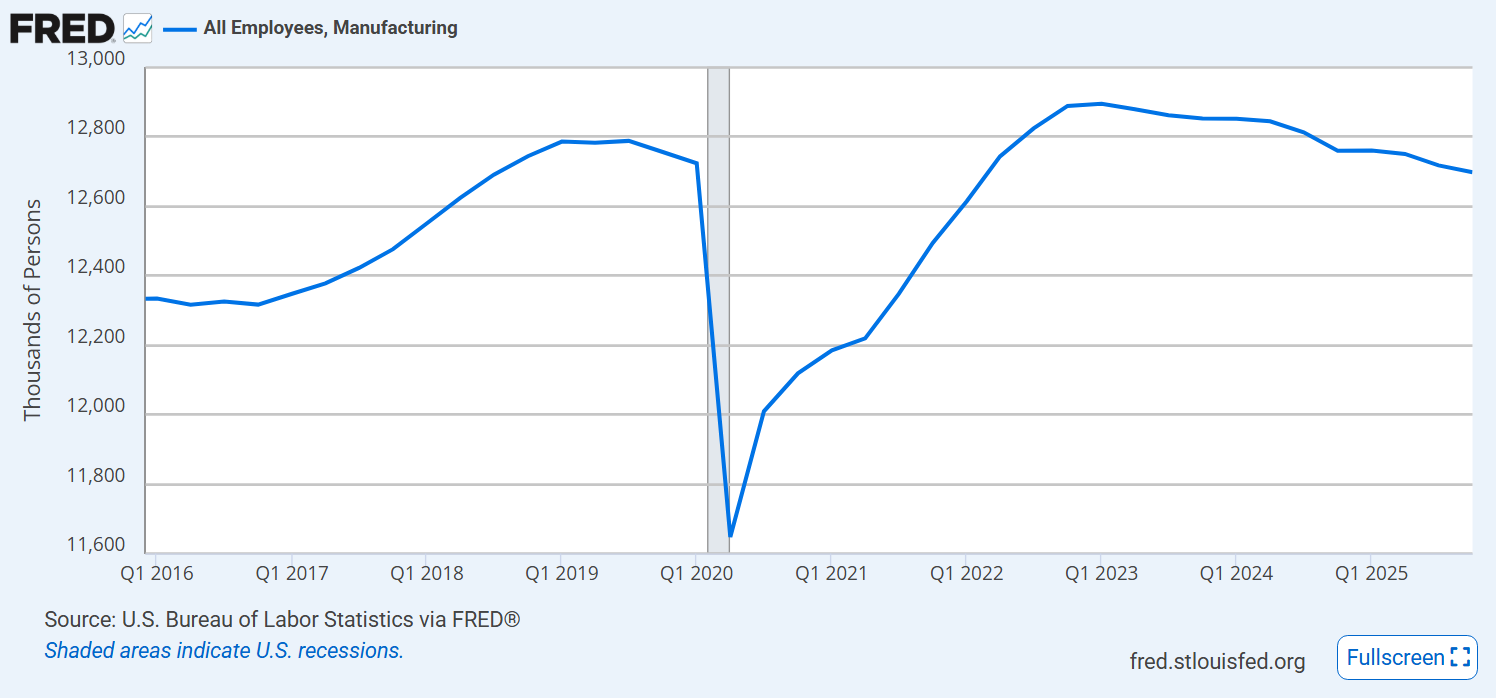

Manufacturing employment continues to decline.

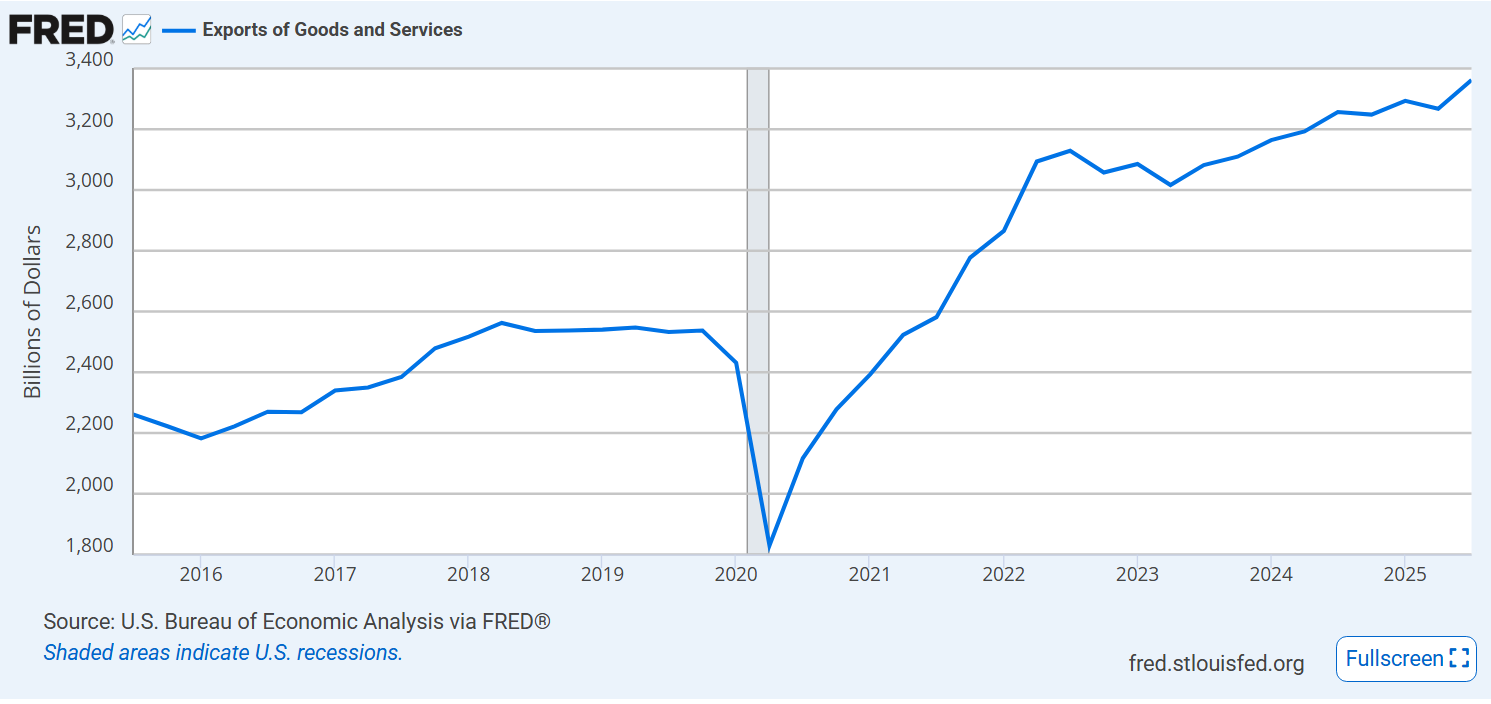

Exports are up 50% and still growing slowly.

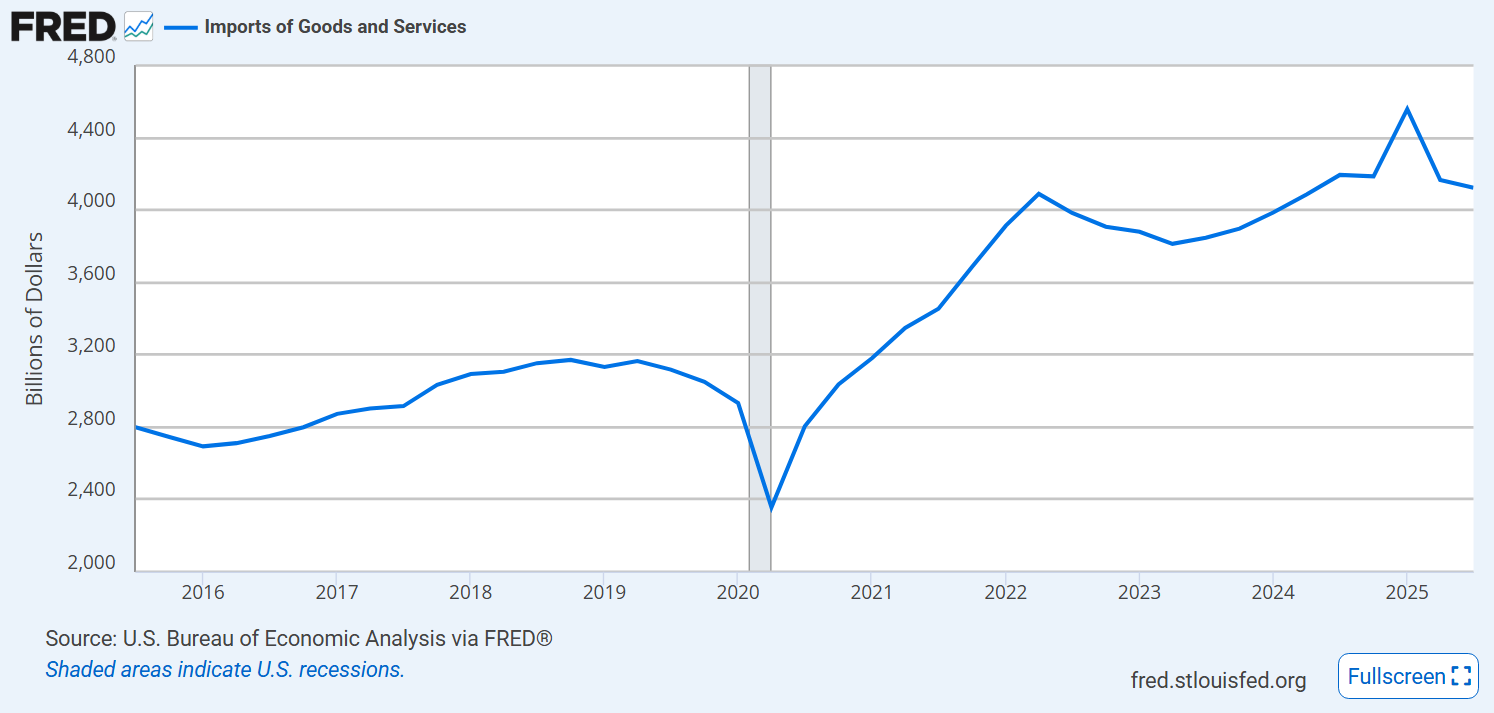

Imports also increased by 50%.

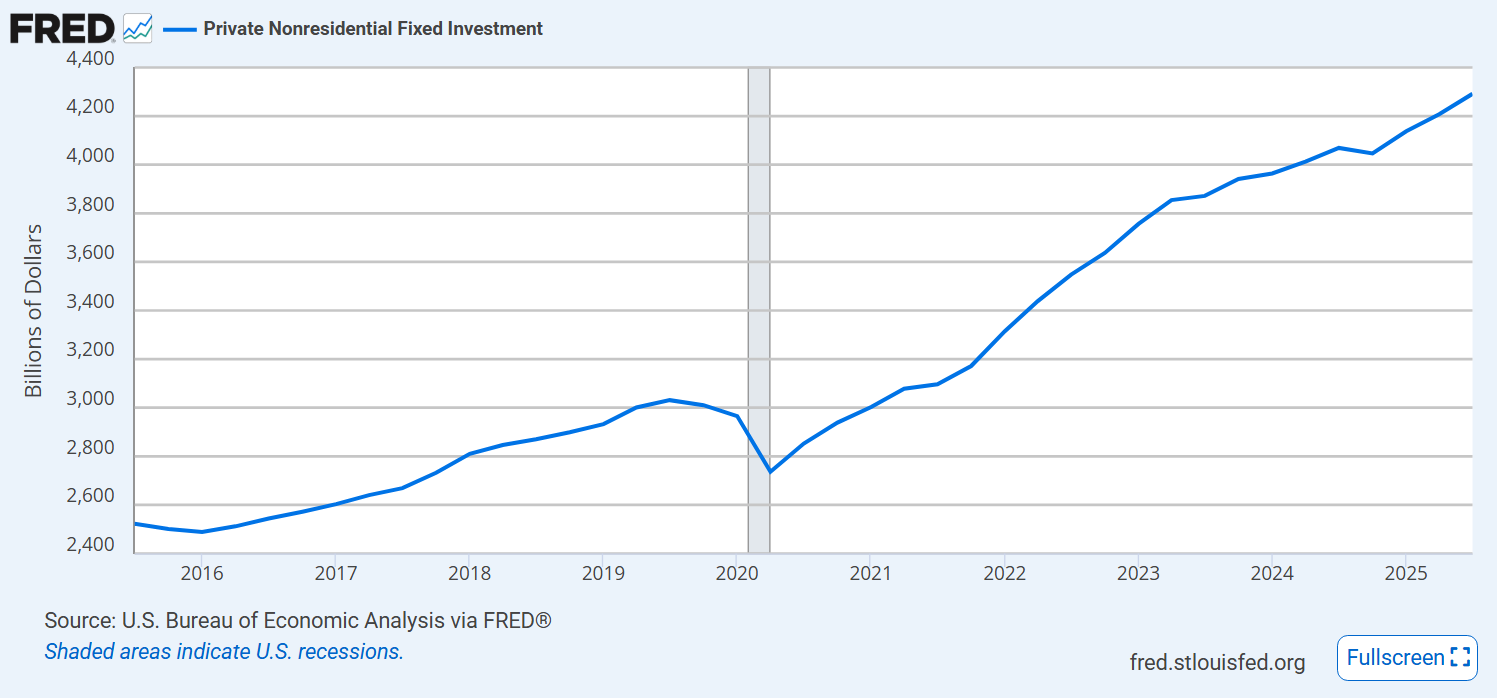

Businesses continue to invest.

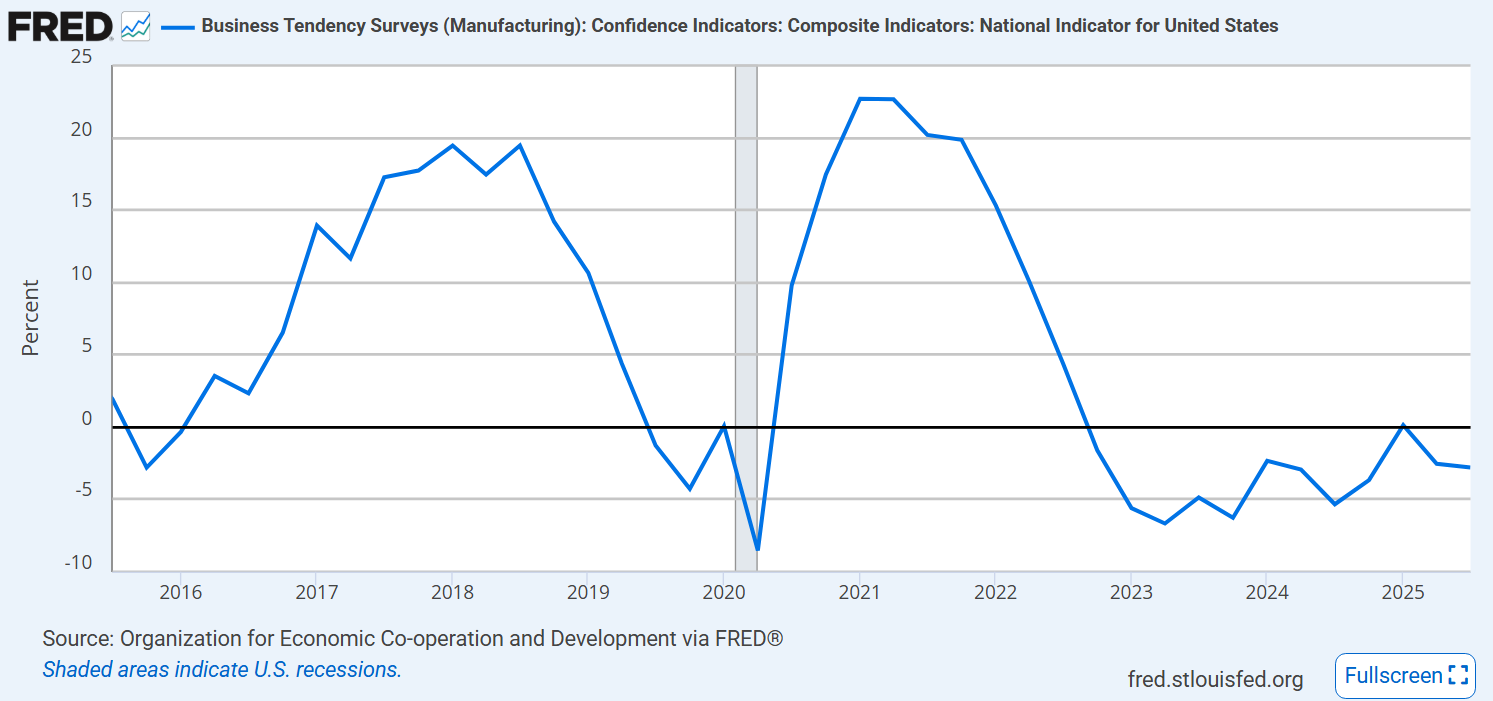

Business confidence remains weak.

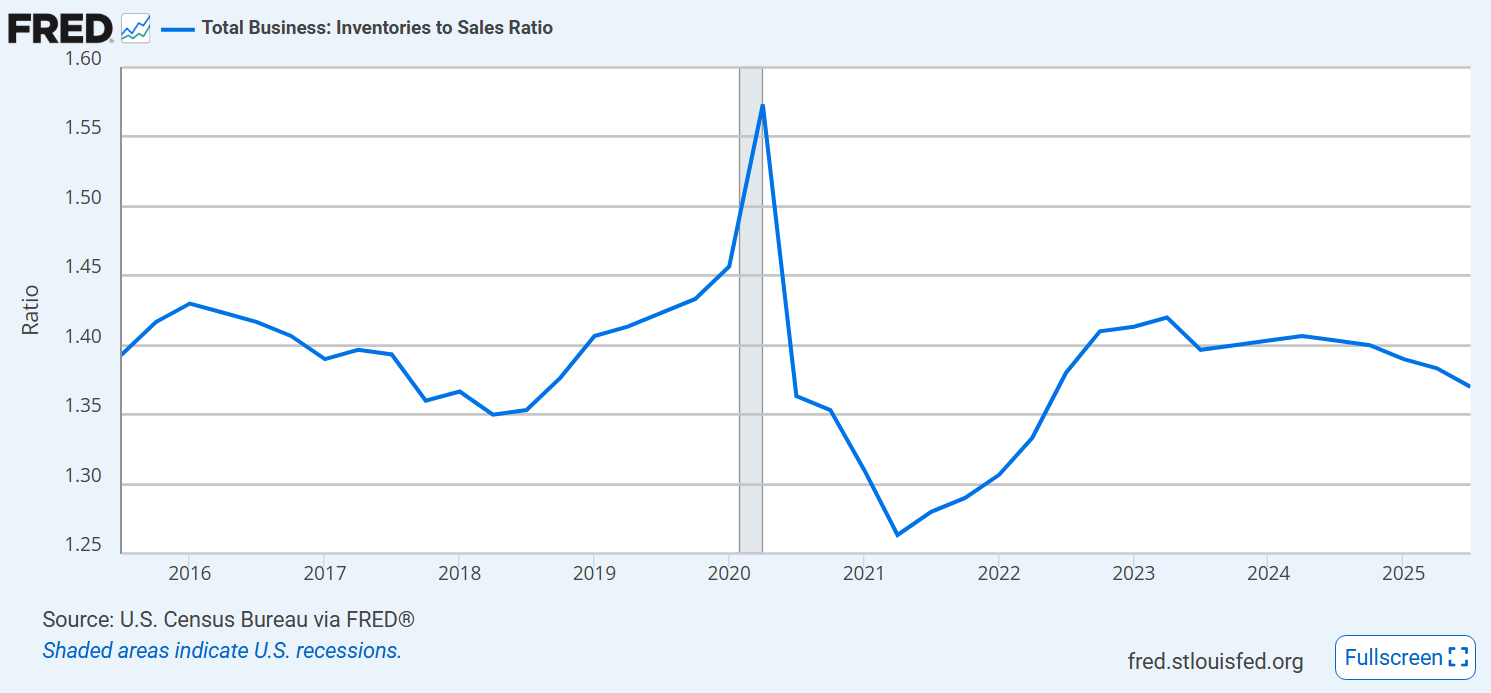

Businesses have maintained their target inventory to sales ratios.

Consumer confidence is down and weak.

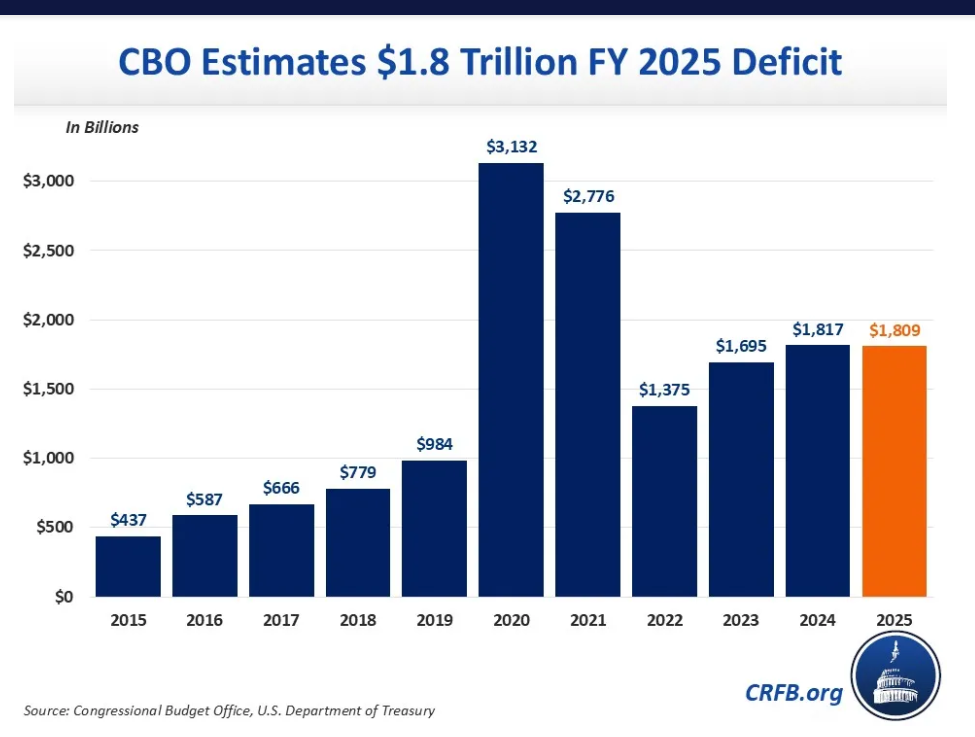

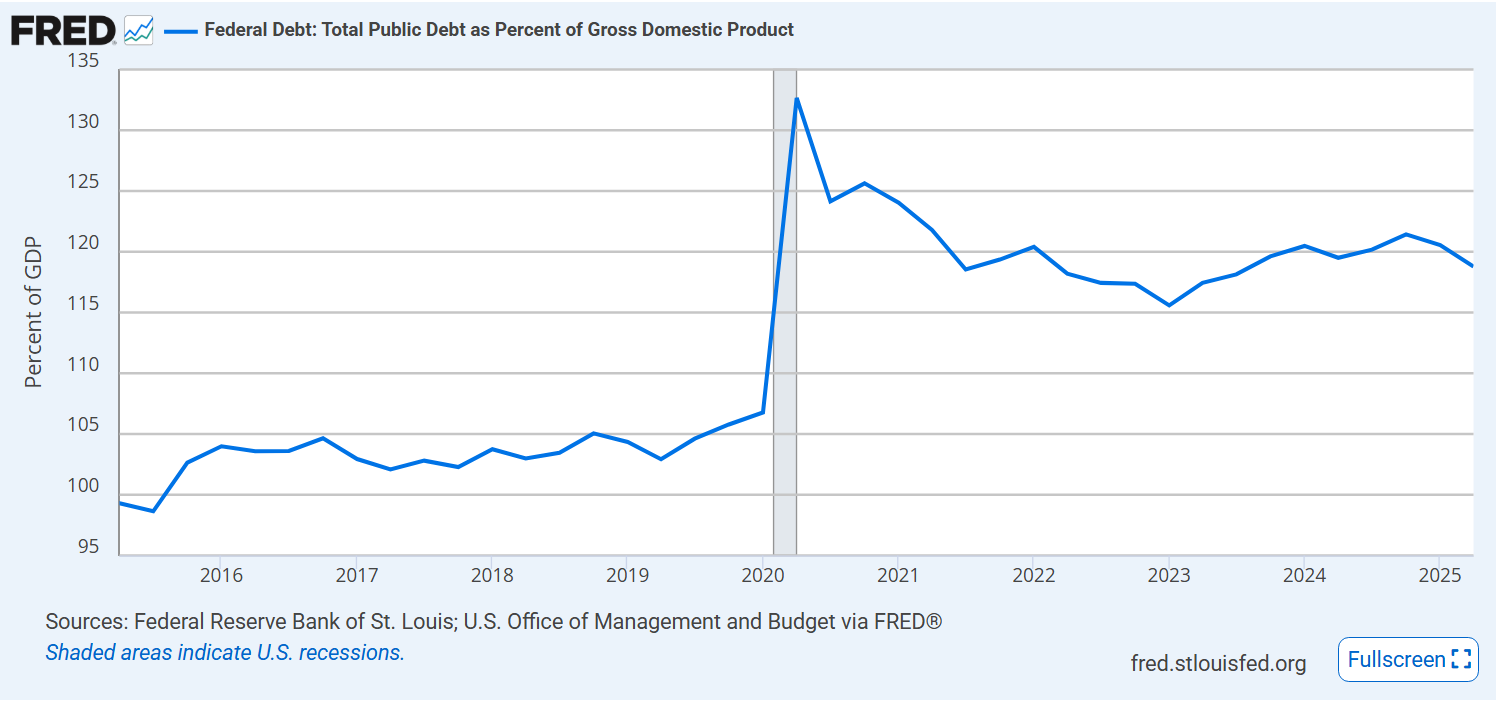

Federal debt % of GDP remains at 120%, up from 105%.

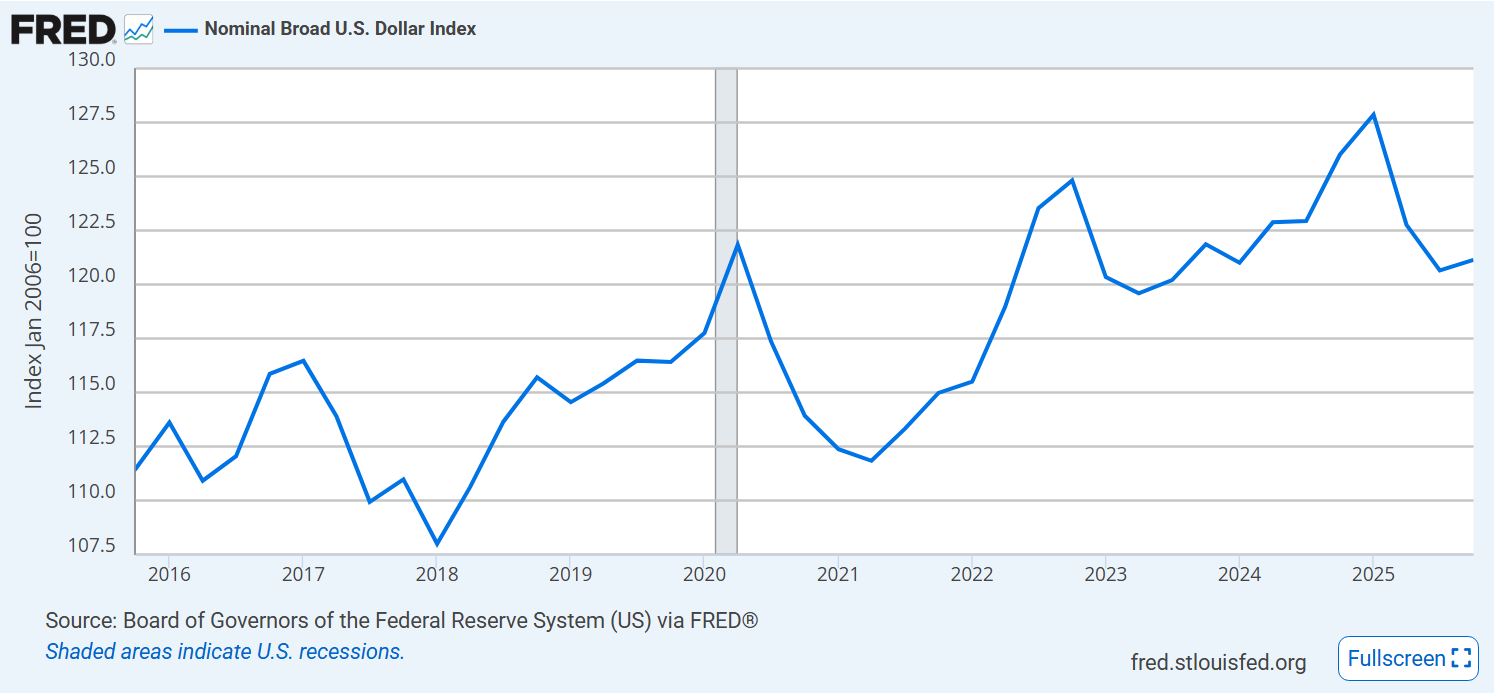

Value of the US dollar increased by 10-12% after the pandemic, but has retreated by 6%.

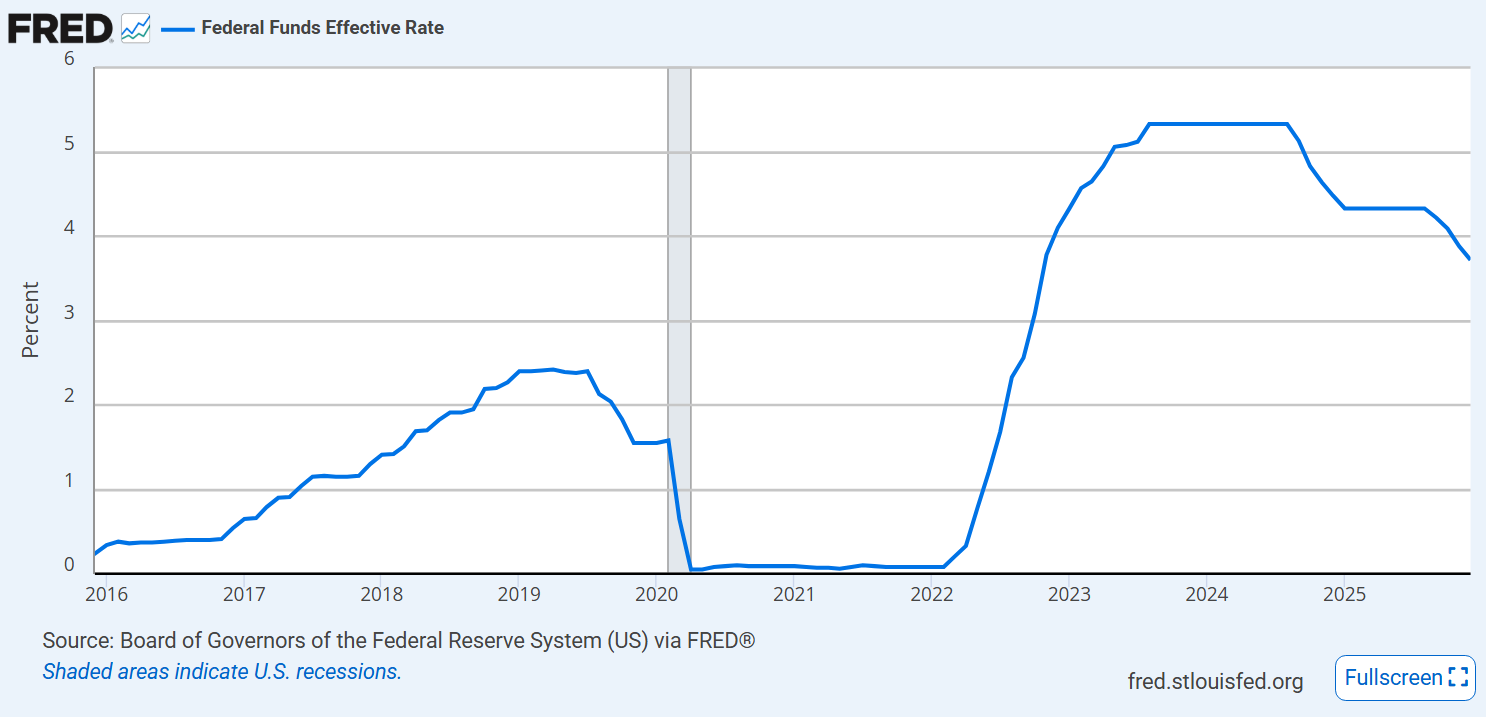

The Federal Reserve Board has reduced interest rates by 1.5%.

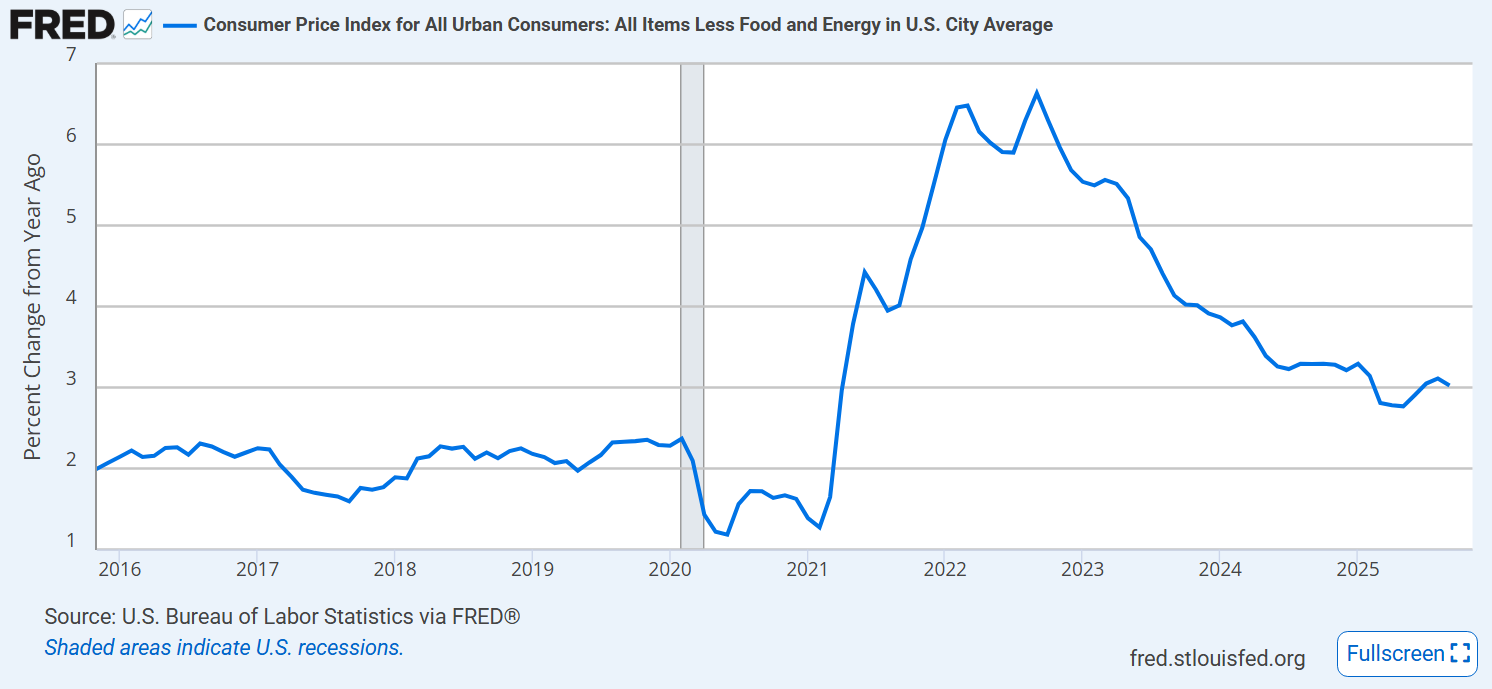

Core inflation rate has levelled off near 3%.

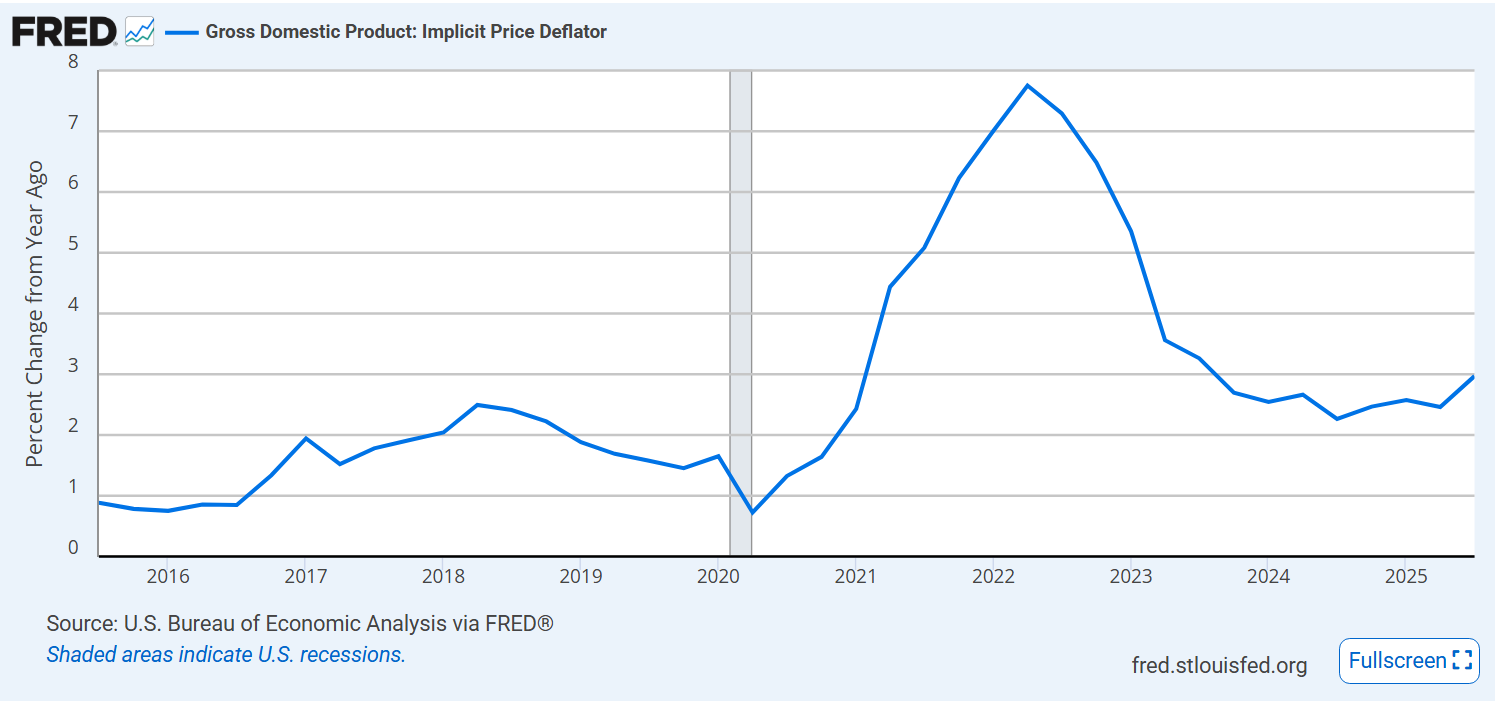

The GDP Price deflator measure of inflation is a little better, approaching 2.5%, but also level or growing.

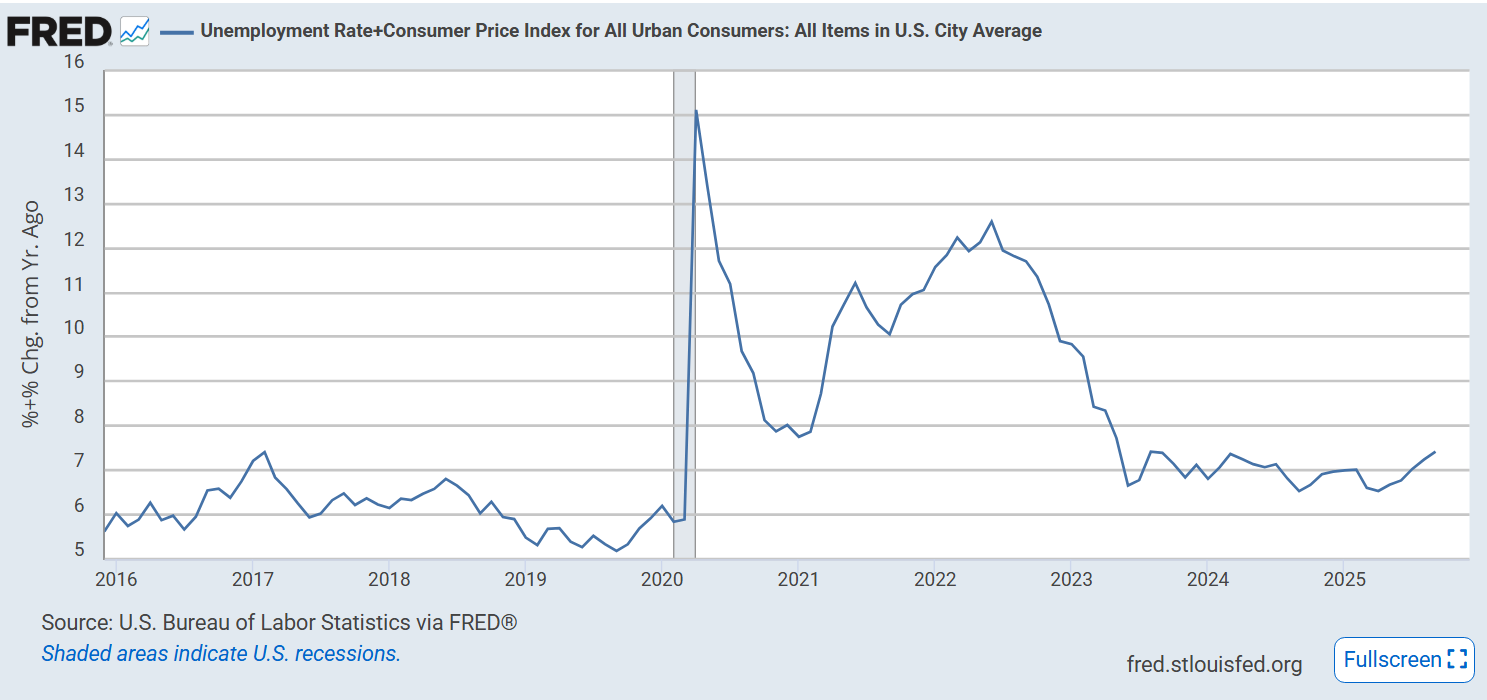

Misery index is up a bit at 7.5%.

Summary

Stock market is solidly up together with corporate profits and business investment.

Inflation and unemployment are up. Budget deficits and debt remain high. Dollar value is down. Manufacturing employment is down. Business and consumer confidence is down.

Other measures are comparable to the 2023-2024 Biden economy base; not improving as often claimed.

The US economy is increasingly resilient and not easily changed by small policy choices or “jawboning”.