The majority of “top 40” hits or “top 100” annual hits in 1967 were melodic and similar to the last 5 years of music. But a subset of 50 less popular songs pointed towards a very different future.

Most of these songs could not be created 5 years earlier or played on the radio in 1962. It’s very hard to explain the break from traditional music and views that began in 1967. Here goes …

“Folk music” was clearly becoming countercultural in 1967, questioning societal norms.

Classic R&B was adopting a sharper edge.

R&B/Soul/Jazz was starting to become much more funky.

The Beatles continued to crank out singles. Less pop, more questions.

The “rockers” were becoming much more “edgy”.

The Stones were adapting …

Jimi Hendrix offered a once in a lifetime music lesson.

Countercultural rock emerged as a major force in 1967, for good or for bad.

Summary

50 edgy new singles in 1967. 1967. 1967. The British invasion continued, with the Beatles, Stones and others making their music and lyrics more current, dynamic and experimental. Core US R&B/Motown/Soul groups adopted a more experimental and critical tone. Folk music poked at societal norms. Rock ‘n Roll leveraged the sharper, electronic riffs. The San Francisco sound wailed. The Doors “broke on through” to the other side. Jimi Hendrix emerged.

The world would never be the same. Music belonged to the young. The sound would be somewhat discordant. The message would be challenging. Musical standards would forever be so much higher.

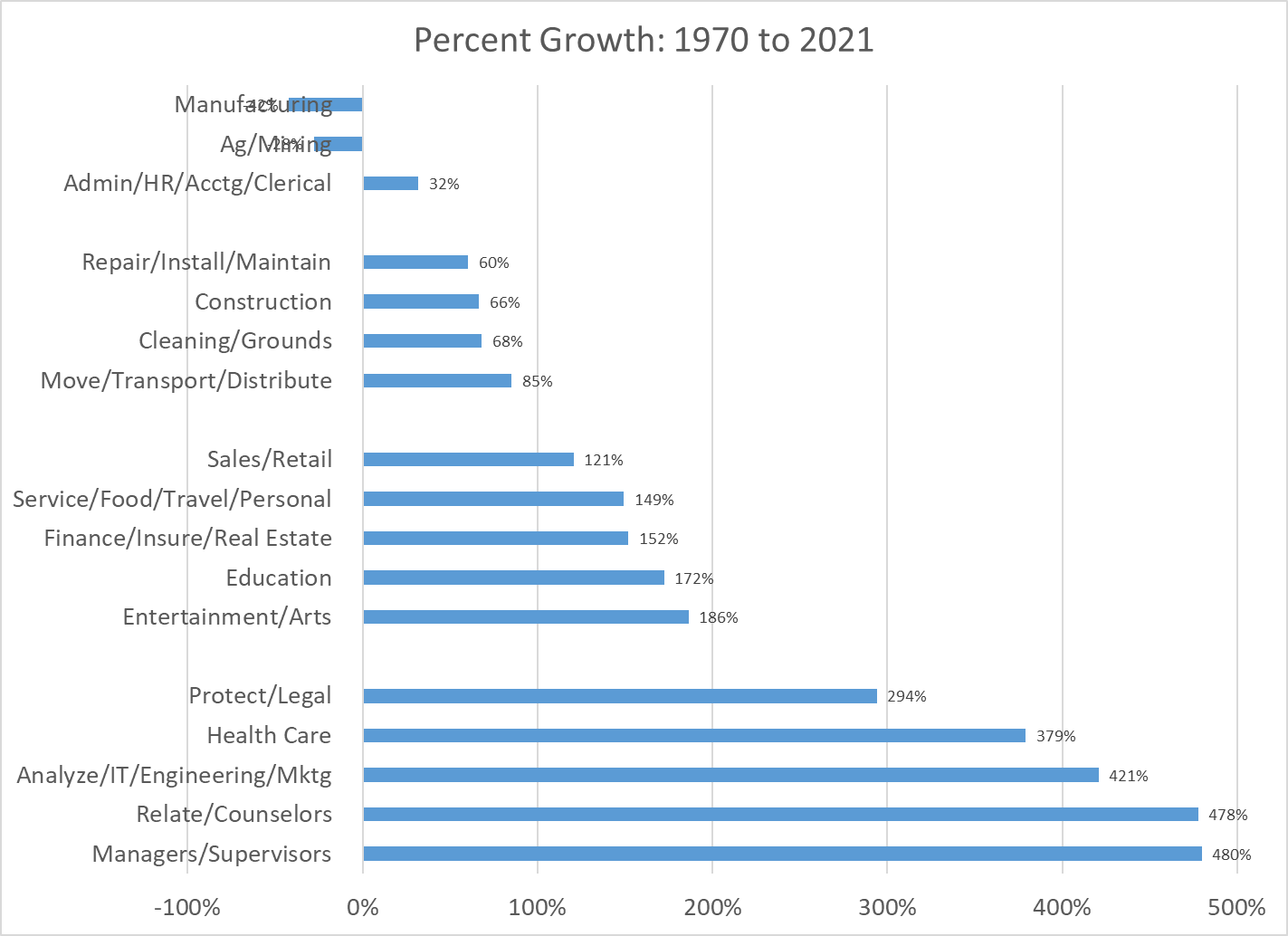

This is a follow-up article to my recent post on “A Very Robust Long-term US Labor Market (1970-2021). Rather than focus on total growth or the “skill-level” of jobs in the labor market, I want to focus on the roles or functions (like career clusters, similar to industries) played by the 150 million US workers in 2021. I’ve grouped the 500 detailed occupations into 17 categories so that we can look at subtotals ranging from 1% to 20% of the total, with an average of 16%. Enough detail to highlight the very significant changes in the last half-century.

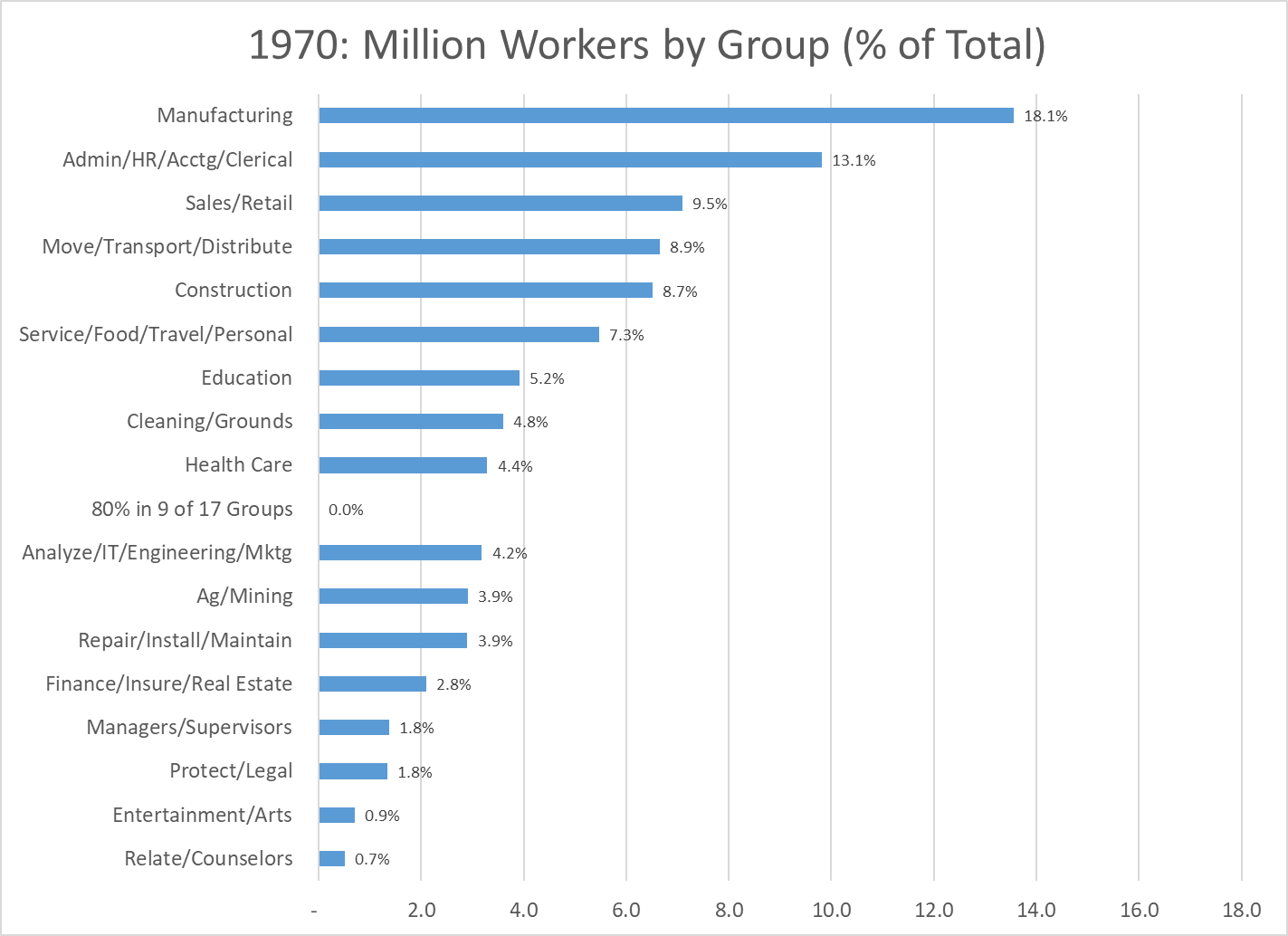

Let’s start with the 1970 data. 75 million employees. Manufacturing was the “big dog”, with almost 14 million workers, 18% of the total, a little less than one out of five.

Administrative workers, including clerical, HR and accounting staff at all job levels were the second largest group, with 10 million people and 13% of the total, one out of eight jobs. These two traditional categories accounted for 31% of the total, not quite one-third.

The next three groups each accounted for 9% of the total, one of every eleven employees. Sales workers, at managerial, professional and retail/clerical levels. Members of the logistics industry broadly defined, including both transportation and distribution staff. Employees of the construction industry. Once again, classic job functions in 1970 that would have been familiar in 1930.

The narrowly defined “service sector”, combining staff in the food service, travel and personal services industries contained 5.5 million workers, or 7% of the total. These six together included 70% of all workers.

Six other categories were each a much smaller 4-5% of the total: Education (KG-post secondary), Cleaning and Groundskeeping, Health Care, Analysis (finance, IT, operations, engineering and marketing), Ag/Mining and Repair/Installation/Maintenance.

The final five categories each averaged just 1.5% of total jobs: Finance/Insurance/Real Estate, Managers/Supervisors, Protection/Legal, Entertainment/Arts and Relating/Counselors.

By 1970 production agriculture had already declined to an immaterial share of the economy. The historically male and blue collar dominated Manufacturing, Logistics, Construction and Repair categories combined to account for 40% of all jobs; two out of five. The historically more female friendly Administration and Sales functions held 25% of all jobs, one in four. Education was the largest “information industry” at 5%, largely dominated by traditional elementary and secondary school teachers. A more broadly defined service group of food service, travel, personal service, cleaning/grounds and health care summed to 17% of the total, or one in six jobs.

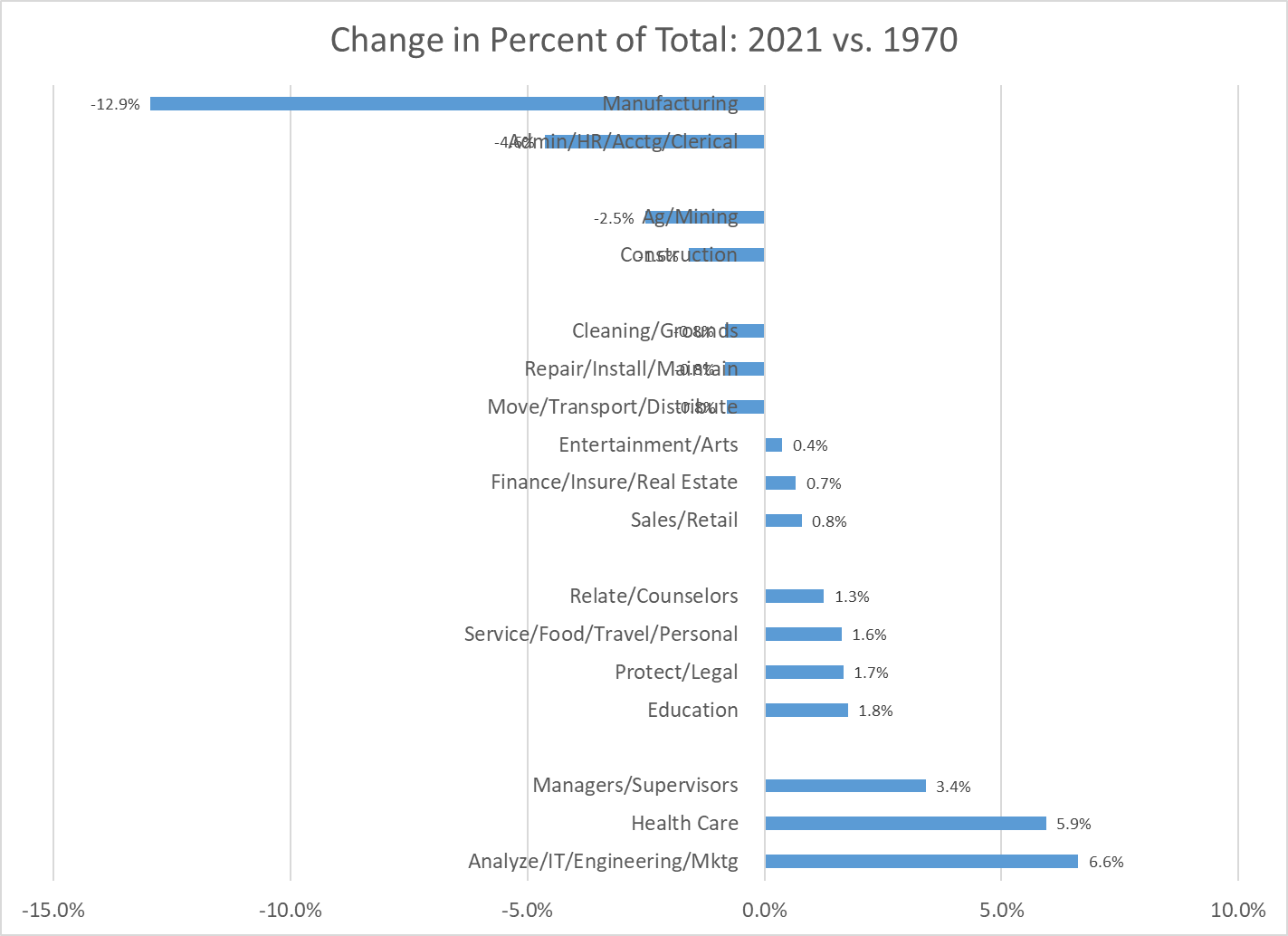

Six categories changed very significantly between 1970 and 2021. Manufacturing dropped from first place to tenth place, from 18% to just 5% of employment, from 14 to 8 million employees. US firms improved labor and overall productivity throughout this period, keeping the most productive firms and factories open, while closing and outsourcing work from the others. This was a tremendous change in the labor market, completed in just two generations of workers.

The Administrative category also declined markedly, from second place to fifth place, shrinking from 13% to less than 9% of total employment, but increasing slightly from 10 to 13 million staff. Process, computer and telecom changes drove improved productivity. Some administrative jobs were outsourced. While the Manufacturing sector lost two-thirds of its labor market share, the Administrative sector lost one-third.

The Ag/Mining group was the third losing category, dropping by nearly two-thirds from 3.9% to 1.4% of all employment. When politicians talk about “reviving” manufacturing, mining or production agriculture they are working against very strong long-term trends.

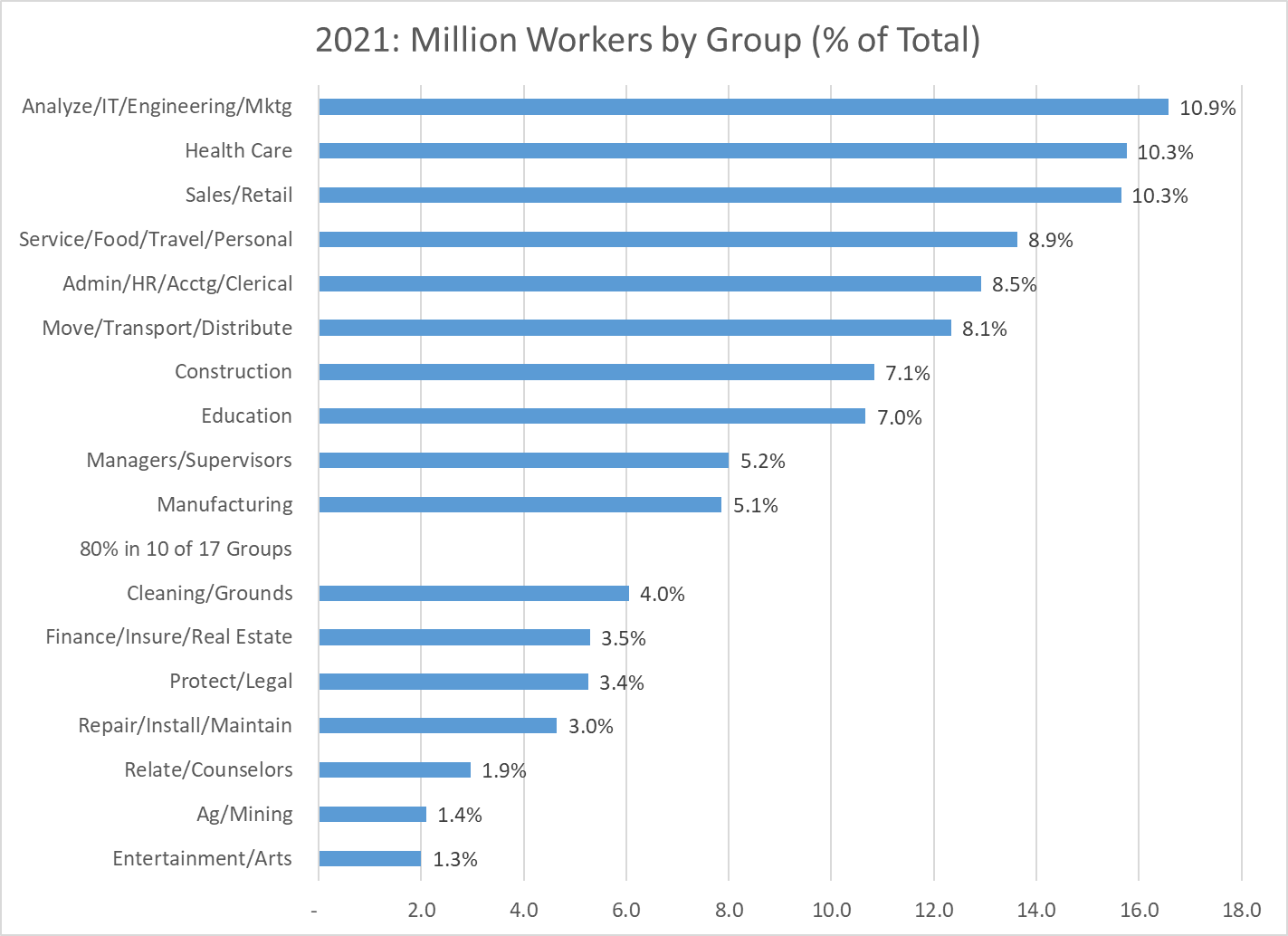

The largest growth was in the “Analysis” category, which grew by two and one-half times as a share of the total, from 4% to 10%. There was incremental growth in the existing Engineering sub-category, adding 2 million roles. The IT category grew added almost 6 million roles from a base near zero. The operations, finance, marketing analysis group added another 6 million positions to its base of 1.5 million. The “Analysts” category rose from tenth place to first place as firms became more complex and found ways to better employ the talents of individuals with high level analytical skills. At 11% of the economy, one out of every nine jobs falls into the analysis category.

Health Care increased from ninth place to second place, moving from 4.4% to 10.3% of all jobs (2.5X). The number of jobs grew by 13 million, from 3 to 16 million.

The Managers/Supervisors category climbed from fourteenth to ninth place, rising from 1.8% to 5.2% of the economy, adding almost 7 million jobs. The 1970 detailed coding was somewhat different from the modern approach, with many supervisors and managers grouped with other professions or industries. My best guess is that on a comparable basis, the 1970 category would have been closer to 2.5 million than the reported 1.4 million managers and supervisors. This would have put this group in thirteenth place in 1970. Hence, the growth as a share of the total market would be smaller, from 3.3% to 5.2%, but still quite significant. Once again, larger firms with more complexity demanded more managers and supervisors.

In total, we have 20% (1/5 workers) leaving the Manufacturing, Administration and Ag/Mining sectors and 16% (1/6 workers) joining the Analysis, Health Care and Managers sectors.

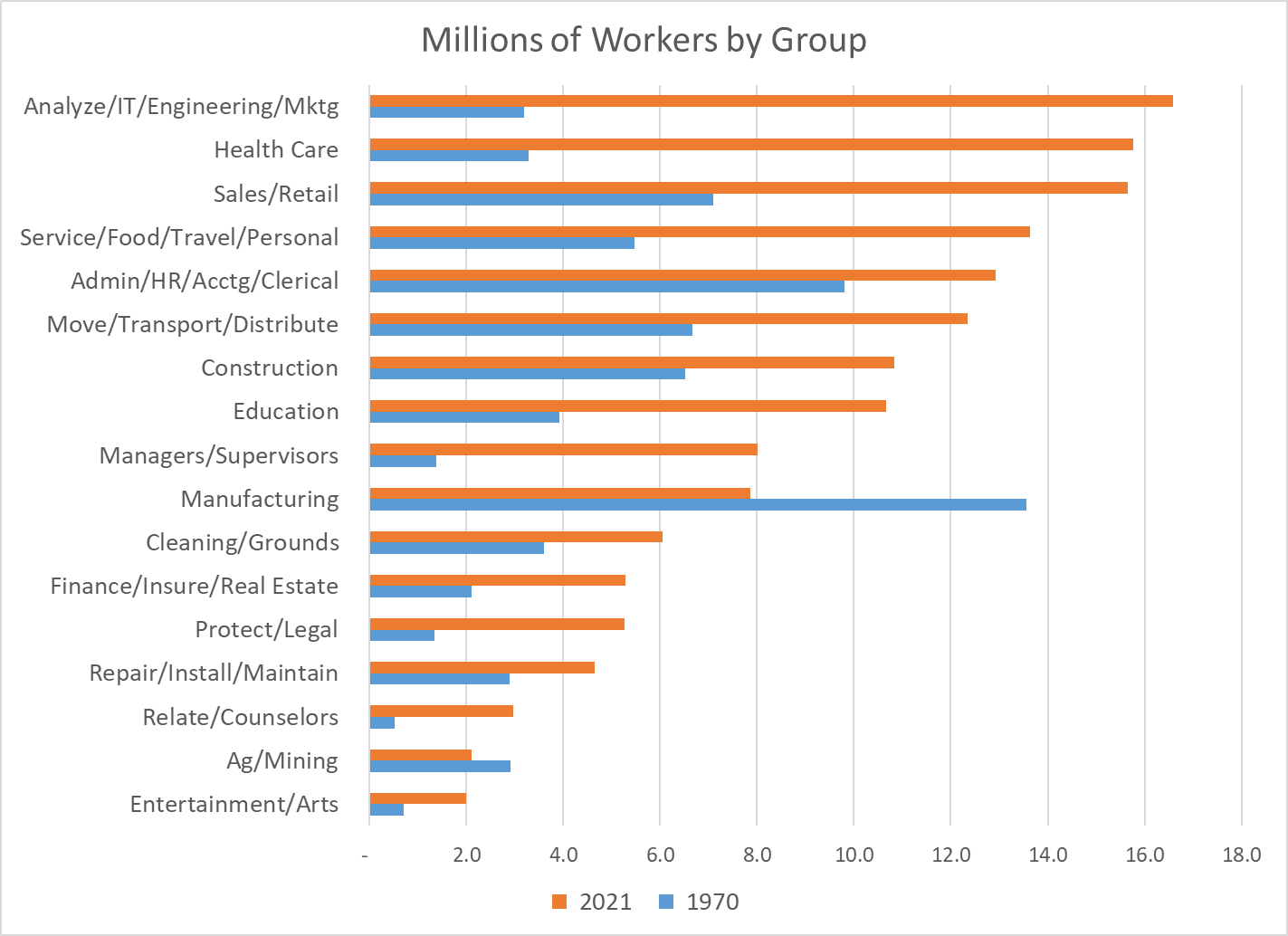

Comparing the millions of employees in 1970 to 2021 by sector clearly shows the massive changes in the labor market. The Health Care and Analysis sectors leapt from a small 3 million workers each to 16 million workers each. Manufacturing fell in absolute terms from 14 to 8 million workers. The Sales and Service sectors began as large sectors, so their relatively normal growth still added about 8 million roles each. Construction and Administration began as larger sectors and were able to add 3 million employees each, despite slower than average growth rates. Logistics grew slightly slower than the market, but added 6 million workers. Education grew faster than average, adding 6 million colleagues.

Relative growth rates as a percentage of the 1970 base or as a percentage of the total mostly tell the same story. Manufacturing, Administration and Ag/Mining have declined sharply. Analysis, Health Care and Management have grown materially.

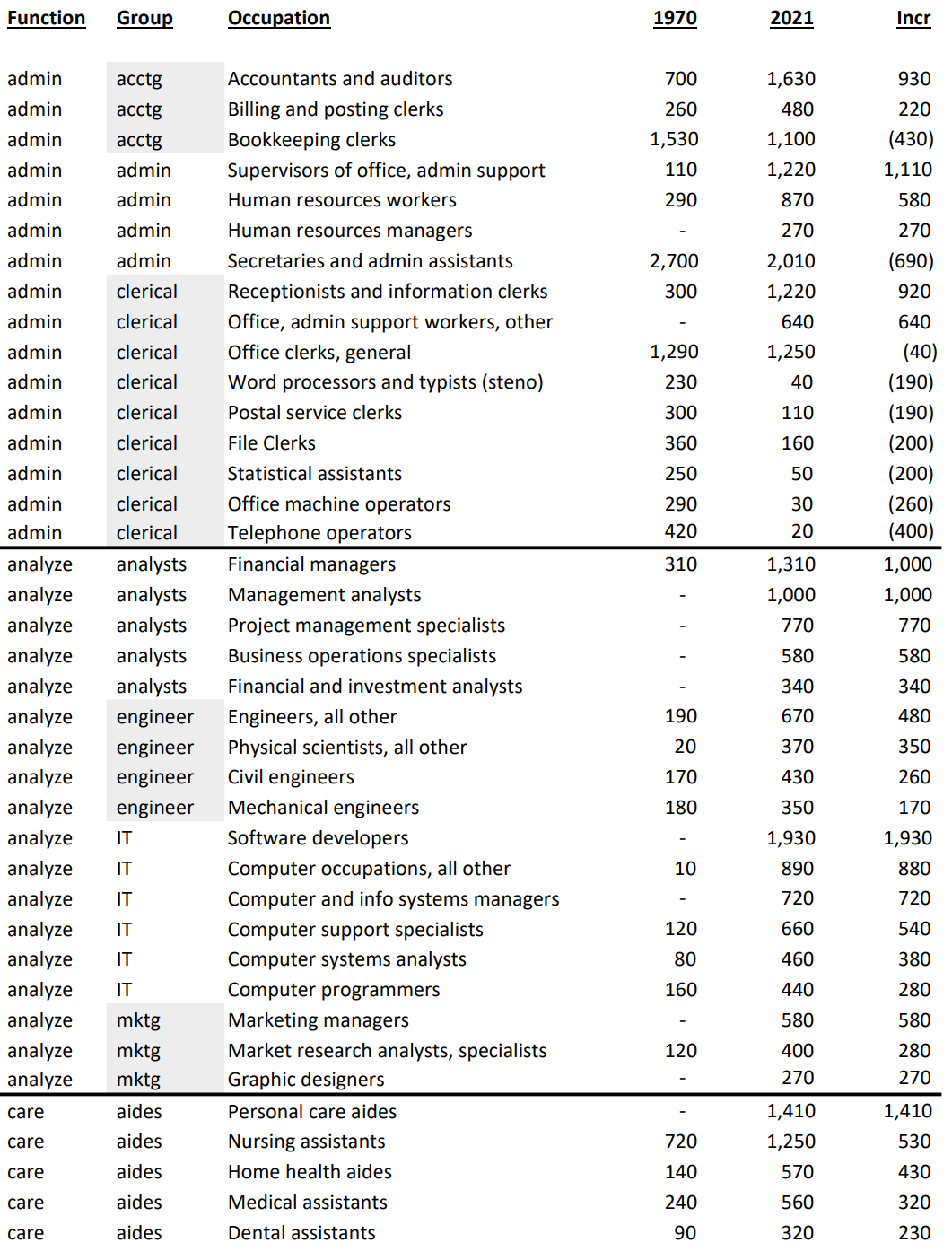

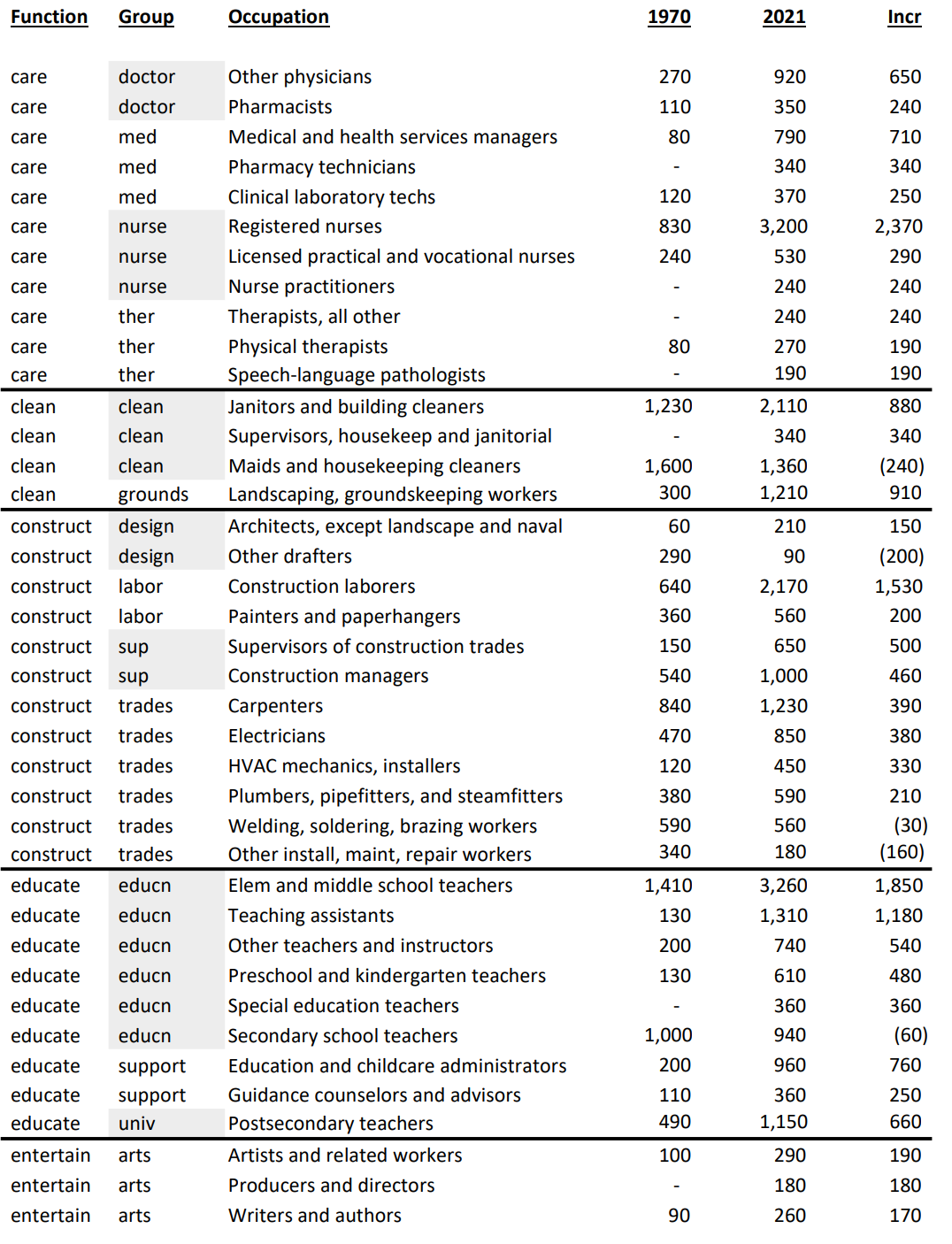

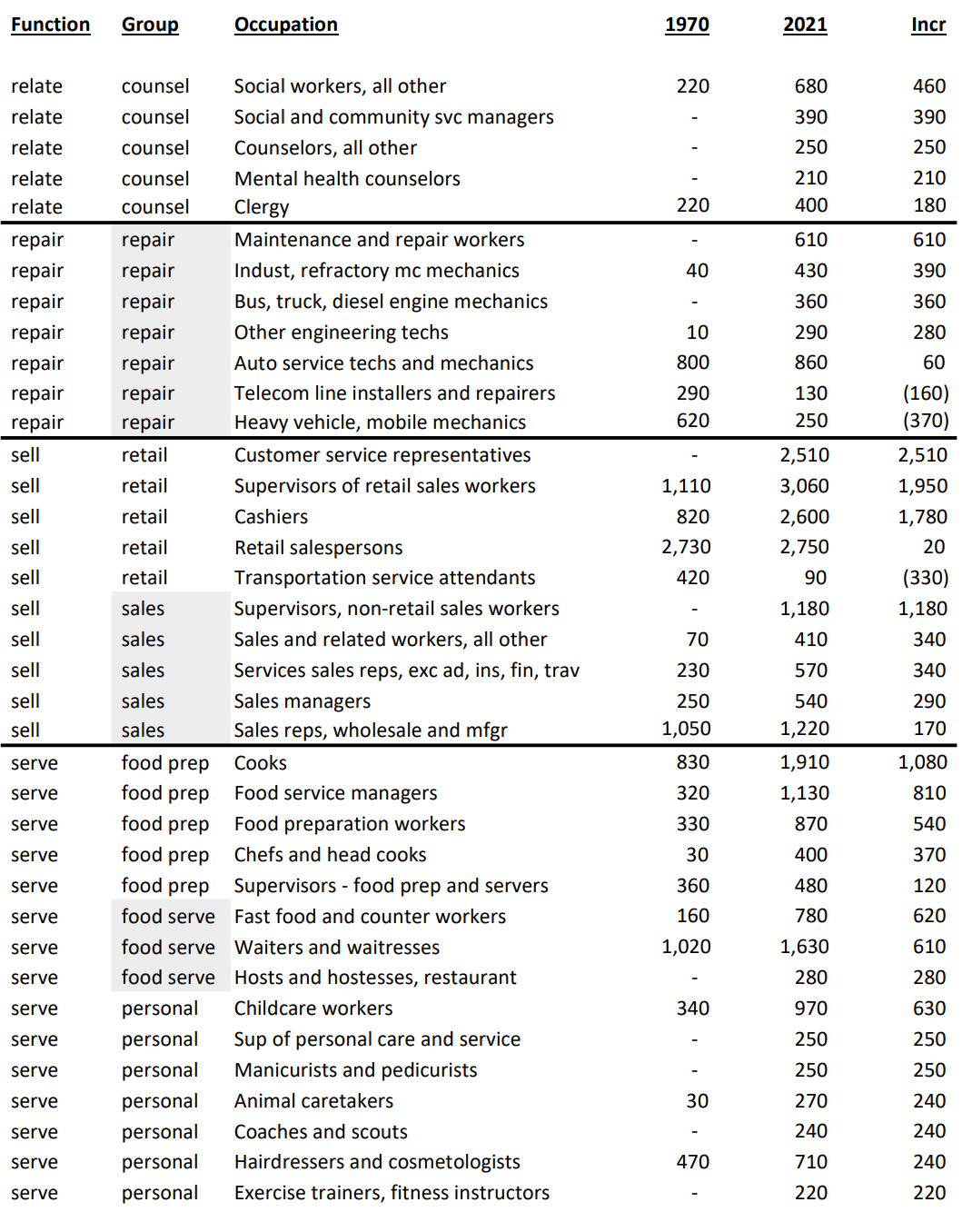

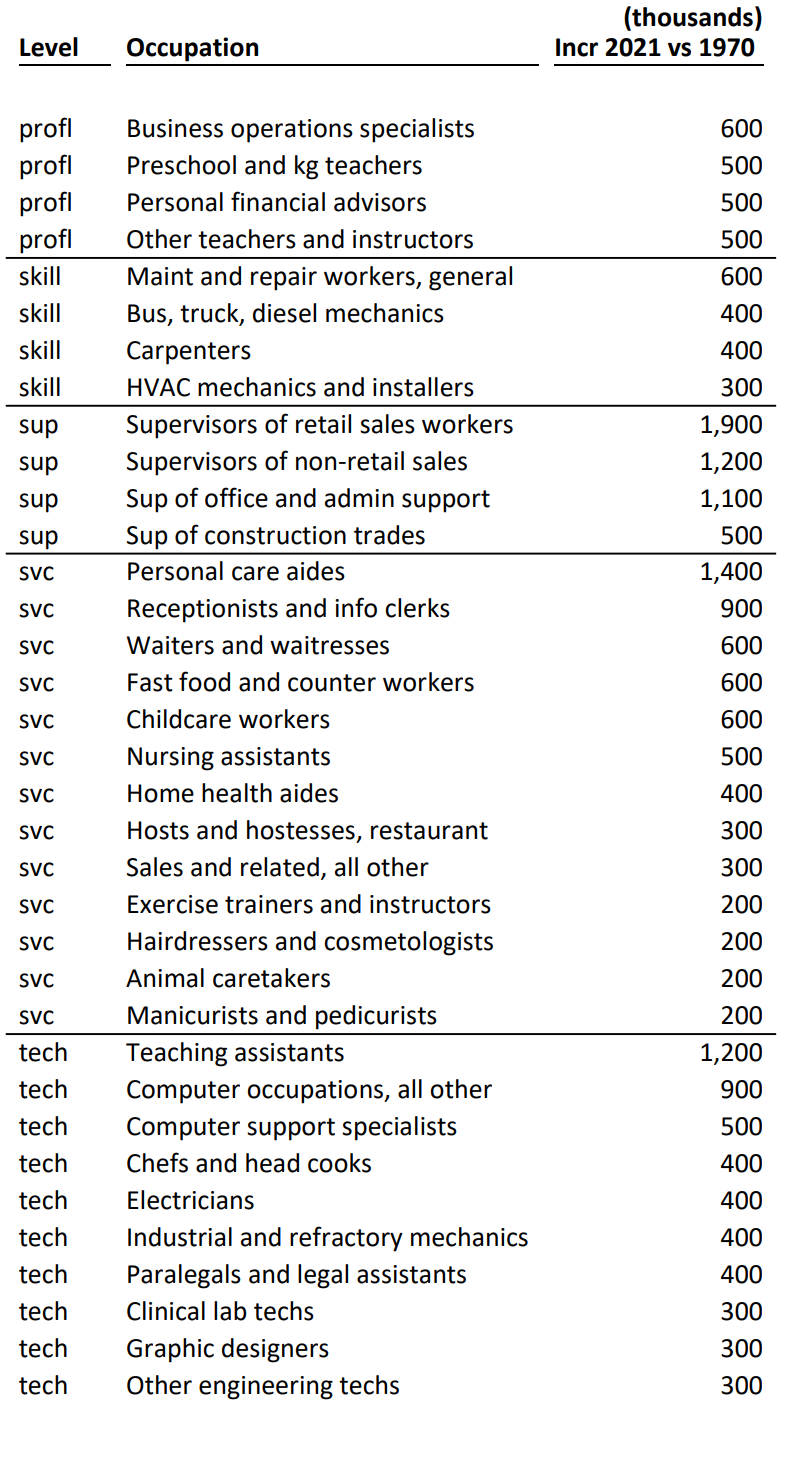

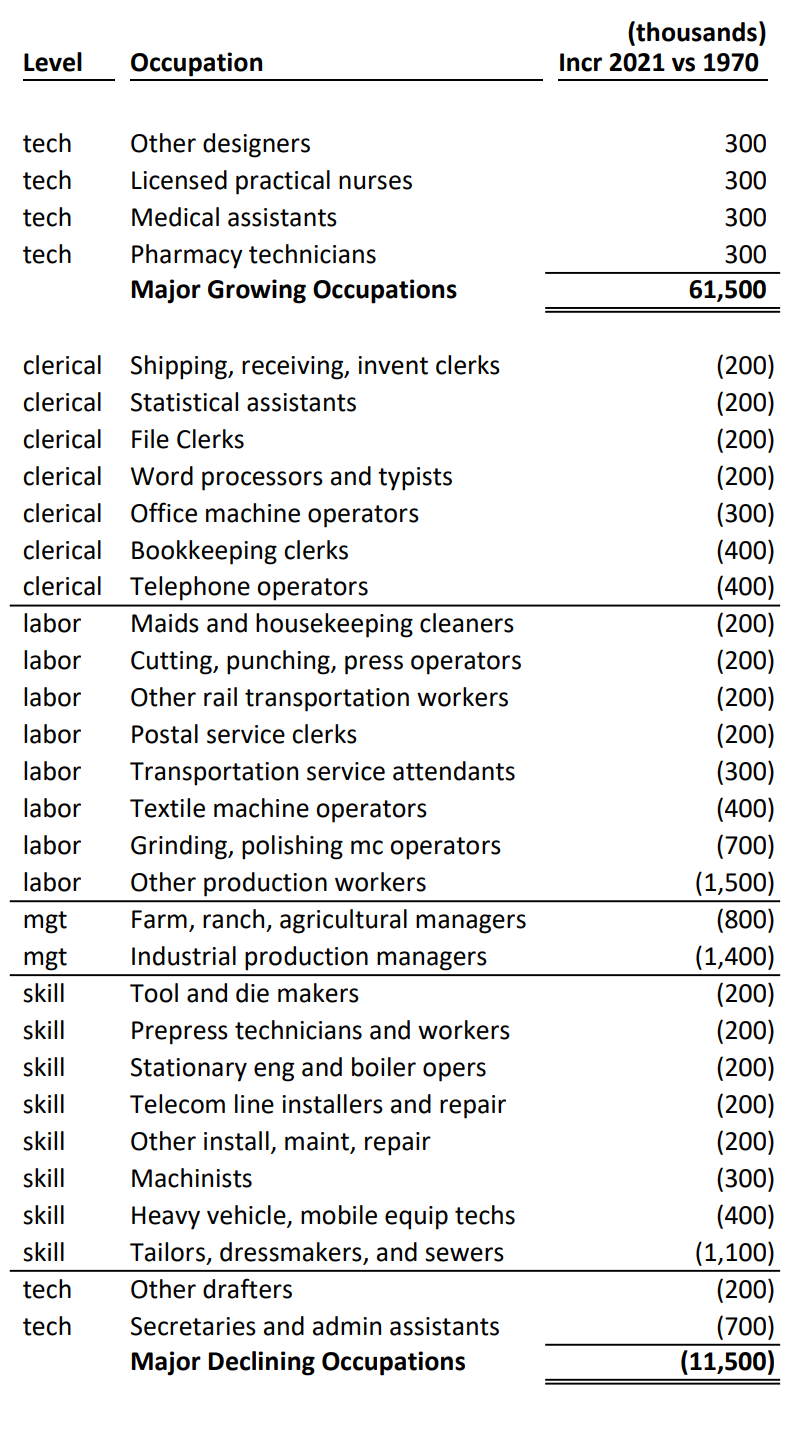

The 152 largest detailed occupations and those with the greatest change in employment are documented below. They account for 91 million jobs, 59% of the 2021 total.

Economists assert that the principles of comparative advantage drive national economic activity. In essence, nations, firms and individuals rationally do what they are “relatively” best at, which changes through time. We see this reduction in the role of agriculture, manufacturing and mining across long periods in the US.

Economists assert that consumers’ tastes change as they have higher income and the relative prices of goods change. Once basic “food, clothing and shelter” needs are met, people turn to other “needs” and “wants”. These tend to be “services” and we also see this transformation.

Economists assert that profit maximizing firms will employ labor that provides a return on the investment based on the marginal or incremental value added by the labor resource. In a more complex economy, professional and managerial skills are in greater demand. Firms (and not-for-profits and governments) have adapted very well to these major changes in the last 50 years.

These changes are not without major pain to individuals, firms and local economies. The general trends in the economy (more automation, greater trade/outsourcing, more services, more personal care, greater role for analytical skills) are clear. Nations, firms, individuals and regions that adapt to the trends will be relatively successful. This requires wise individual and political choices and investments.

A Dozen False Claims of Journalists, Analysts and Pundits

Job growth is too slow, there are not enough jobs.

All of the good jobs are gone, there are fewer good jobs.

The only growth has been in “low wage”, service jobs.

There are no “blue collar” jobs, no “hands-on” work is available today.

Jobs are all “dumbed down”, no real content remains.

Automation, computers and artificial intelligence are eliminating all jobs.

There is no room for advancement at work.

The economy is inherently stagnant, firms are unable to create new positions.

We’ve become a nation of shopkeepers.

There’s no hope for millennials in the job market, Boomers are leaving a disaster.

More and more jobs are subject to the “imposter syndrome”, they really do nothing.

This time is different, we have reached the “end times” for jobs.

The Data Says …

The US Census Bureau and the US Bureau of Labor Statistics attempt to measure the detailed occupations in the evolving US labor market. I have selected 1970 as a baseline because it is effectively prior to the “computer revolution” and within my lifetime of observing the labor market. The US economy was still essentially in the post WWII boom period with manufacturing clearly the most important industry in 1970. Prior to Japanese or Chinese competition. Prior to the “energy crisis” and environmental concerns. Prior to improved social, political and economic opportunities for women, racial and other minorities.

We had 153 million people working in the US labor market in 2021.

The total measures and the detailed measures are somewhat inconsistent between 1970 and 2021. But, they are adequate to make basic comparisons. The labor force doubled in 50 years. 75 million new jobs created! 15 million new jobs each decade. 1.5 million new jobs each year, on average.

The detailed occupation categories have also changed. The 500+ categories in 1970 are very different from 2021, but the basic measures are roughly consistent. I have mapped the 1970 categories onto the 2021 categories. In 1970, the “undefined” responses were in the 10% range and not reallocated back to the detailed occupations as is done currently. Self-employed individuals were measured differently. Managers and supervisors were measured differently. The current definitions are better aligned with the current jobs. The 1970 categories provided much more detail on the manufacturing sector.

Employment by Job Level

Total employment more than doubled.

The highest level “manager/supervisor” jobs category nearly tripled. 18 million manager/supervisor jobs were added between 1970 and 2021. In 1970, there were 10 million manager/supervisor jobs; 13%, or one out of every 8 positions. The newly added positions are 24% of the labor force in 1970. The 28 million current manager/supervisor roles are 37% of the total 1970 work force. Opportunity, indeed. In 2021 terms, manager/supervisor roles are 18% of the work force, more than one of every six positions.

Professional jobs (college degree plus required) also tripled, growing from 14 to 41 million, an increase of 27 million new jobs. This increase is 36% of the 1970 work force. The manager, supervisor, professional subtotal is 23 million in 1970 (31% of the total). It has grown to 69 million (3X) in 2021, reaching 45% of the labor force. The number of “premium” jobs tripled, while the share of “premium” jobs increased by almost 50% in this half-century. Good news, indeed.

“Skilled” labor jobs were flat across 50 years, declining as a share of total jobs by one-half, from 10% to 5% of the economy. However, their neighbor, technical jobs, increased faster than the economy, adding 10 million high quality positions. The combined skilled labor (trades) and technician/technical level positions increased from 15 to 25 million, overall. This two-thirds growth is slower than the overall labor market’s doubling. Hence, this job level decreased from 20% to 16%, or from one in five to one in six positions. This is a “glass half-full or half-empty” situation. The 14% of the total labor market growth for premium positions is offset by a 4% decline in middle skilled positions, resulting in a 10% increase of combined middle and premium positions as a percentage of the total.

Lower skill level jobs accounted for nearly half of all jobs in 1970; 37 of 75 million. They comprised a decreased 39% of the total in 2021, 59 million out of 153 million. A smaller share of “lower skill” jobs seems like progress. Yet, even here, we have a growing labor market, with 59 million jobs in 2021 versus just 37 million jobs in 1970; 50% more.

The “physical labor” category grew from 22 to 32 million jobs, but it declined from 30% to 21% of the work force. Relatively fewer jobs, absolutely more. The clerical workforce encountered a similar, but less extreme change, growing from 11 to 15 million jobs, but declining from 14% to 10% of the work force. The “service sector” grew twice as fast as the overall economy, increasing from 4 to 12 million jobs and from 6% to 8% of all jobs. The “service sector” is growing disproportionately, but it is a relatively small part of the overall economy, just 8% of the total in 2021.

In total, the lower skilled clerical, labor and service groups combined, grew from 37 million to 59 million positions, but declined from 49% to 39% of all jobs. I see this as progress and look forward to the next half century reducing this category to just 30% of all US jobs.

At the detailed level, we have 70 occupations driving 62 million new jobs, 82% of the 1970 base. We also have 27 occupations experiencing a 12 million jobs loss, 15% of the 1970 base. Joseph Schumpeter’s “creative destruction” model of a dynamic economy is validated. Changes in demand and technology eliminated 12 million jobs, 15% of the total, across 50 years. The US economy is capable of permanently destroying and replacing a quarter million positions each year, about one-fifth to one-third of one percent of total employment.

Let’s go back to the dozen negative claims. Is there support in the details? Are there “good” jobs being destroyed? I only see declines due to “natural causes”: improved IT, telecom, process/quality/manufacturing, international trade, railroad, textile automation/imports, ag productivity, printing and DIY office options.

On the upside, what do we see? Management and supervisor roles growing in all areas in a more complex environment with higher sales volume, more products, faster product introduction, more exports, more outsourcing of functions, greater customer demands in all dimensions, global sourcing and competition.

Technology supplemented/infused positions at all levels. Cashiers, customer service reps, distribution employees, tellers and drivers today leverage IT systems and processes.

Increased specialization/technical skill in many service/technical areas. Retail terminals. WMS. HRIS. EDI. Customer service scripts. Web based transactions.

Increased professional skills, sophistication and impact in all areas.

More professional teachers, nurses, analysts, accountants, lawyers, HR, real estate and financial advisors.

Diverse technical computer, automation, lab, design, legal, teaching, culinary and design technical positions.

More medical, food service and personal care service roles.

Summary

In the last 50 years the US labor market has doubled in size and added an increasing share of managerial/professional/technical positions.

In my next blog, I’ll focus on the next level of detail: 17 categories of the US labor market.

It’s time to revisit the state of the US economy. The media and stock market are overreacting to the positive news today that the US economy added about 250,000 jobs in September. Pundits and investors deem this as a “too hot” labor market which will drive higher inflation and force the Federal Reserve Board to further increase interest rates to slow the economy. We need to look at history, components of the economy and specific measures carefully to evaluate our position.

In a nutshell, the US Congress and President spent so much to offset the pandemic that we have classic inflation from higher demand and lower supply. At the same time, the Fed increased the money supply and lowered interest rates to zero to ensure that the banking sector did not provide a “credit crunch” to businesses or households. Foreign governments and banks acted similarly. This allowed the world economy to work through the pandemic with minor negative effects. However, the boost to the economy was too much and governments and central bankers were slow to reduce the stimulus they provided. The world was tightly focused on “recovering” to the pre-pandemic GDP and employment levels during 2021, so major changes in government spending and the money supply were not implemented until near the end of 2021. By the start of 2022, it was clear that growth was unsustainable and inflation was rising quickly, so policy makers needed to adjust. They have now done so and the impacts can be seen. So far, the economy is slowing, official recession or not, to low/zero growth and looks to remain at that level through the end of 2022 with low/slow growth expected in the first half of 2023.

We can call this a “soft landing”. We can call this a “growth recession”. We can call this a “recession” or a “recessionette”. There is no evidence of a “major recession” with 2% GDP declines or 3% unemployment rate increases or “50% declines” in housing starts or bank lending freezes or massive industry balances to liquidate or … Inflation is high and seems to have peaked. It is not coming down as quickly as most experts (or me) predicted during the first half of 2022, but many factors indicate that we are not in a self-perpetuating inflationary spiral.

With the benefit of hindsight, real GDP growth during 2018-19 was somewhat above trend and unsustainable. A 2% excess output doesn’t seem like much, but it does matter. The economy at the end of 2021 was in roughly the same place with 3.5% style unemployment. 4Q, 2021 was more than $1 trillion higher (5%) than 4Q, 2020. 5% real annual economic growth is very rare for a large, modern, developed economy. This was after the immediate pandemic bounce. The 3rd and 4th quarters of 2022 are likely to be reported as essentially flat with the 2nd quarter. Consensus forecast is near zero growth in the first half of 2023, returning to 2-3% growth in the second half.

US government budget deficit will be $2 trillion lower in the fiscal year ending September, 2022. This is good news. The “excess” spending was capped more than one year ago, so the trend rate is part of the current core economy. “Excess government spending” is not driving inflation today. It contributed to the inflationary build-up during 2021 into the first half of 2022 (economic stimulus works with a lag effect).

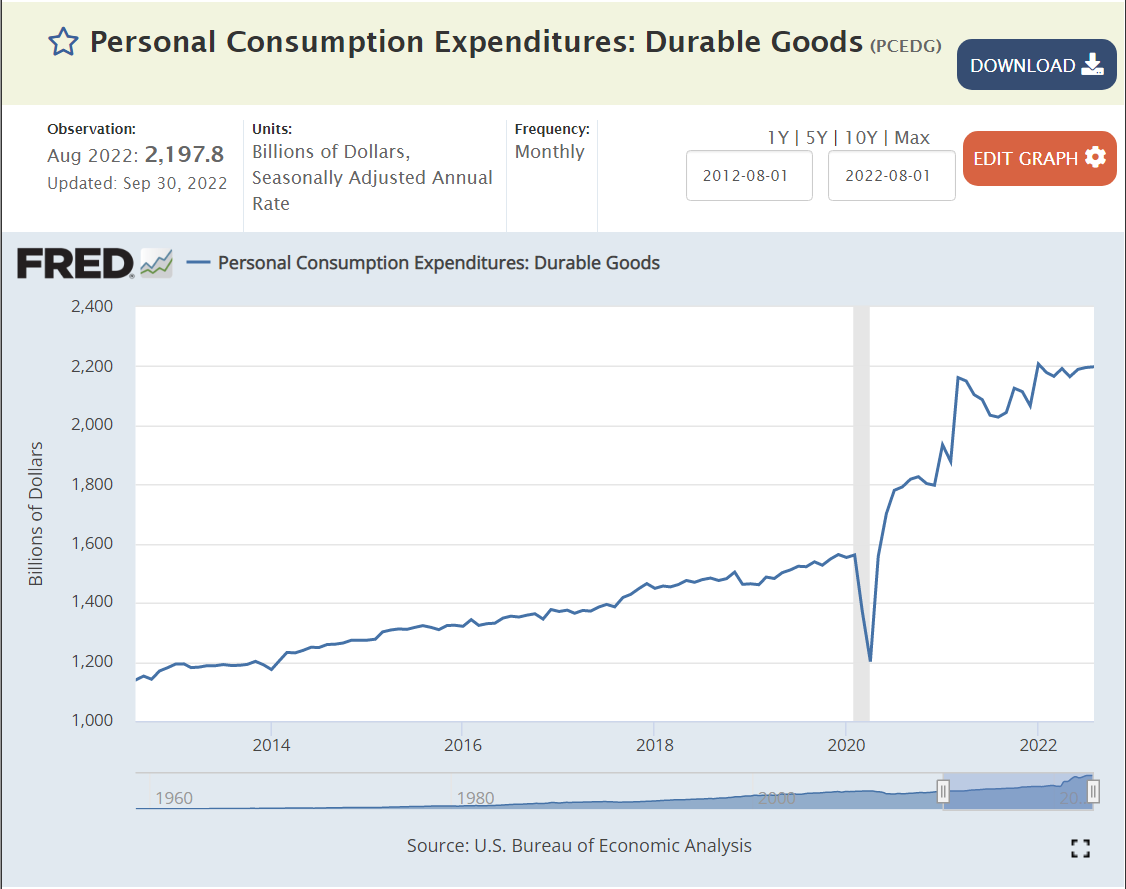

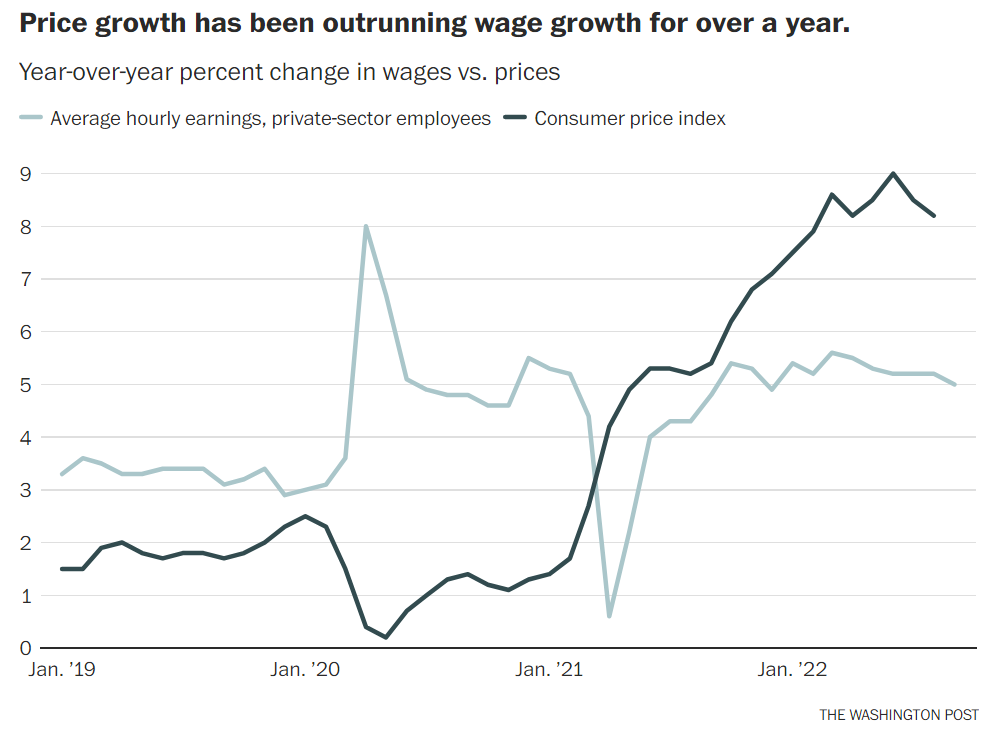

The increased money in consumers’ pockets lead to a 30% increase in purchases of durable goods. Consumers had money. They were afraid to consume in-person services. They bought stuff. They’re still buying stuff. The transition from buying goods to buying services has been slower than expected. This has led to extended supply chain disruptions (globally), higher demand for many commodities and increased goods prices which feed higher inflation and higher demand for labor. The total demand for durable goods has flattened and prices have stopped increasing. This is a much-improved situation from late 2021.

Consumers did save some of their extra earnings during 2020 and the first half of 2021, but as prices increased and services became available, consumers chose to spend more and reduce their savings rate down to just 4% of income, well below the 7-8% of the prior expansion period. So, part of the “excess demand” in late 2021 was the drawdown of savings. That cannot happen again. It’s possible that low consumer confidence will reduce spending in the next year, but flat spending is more likely.

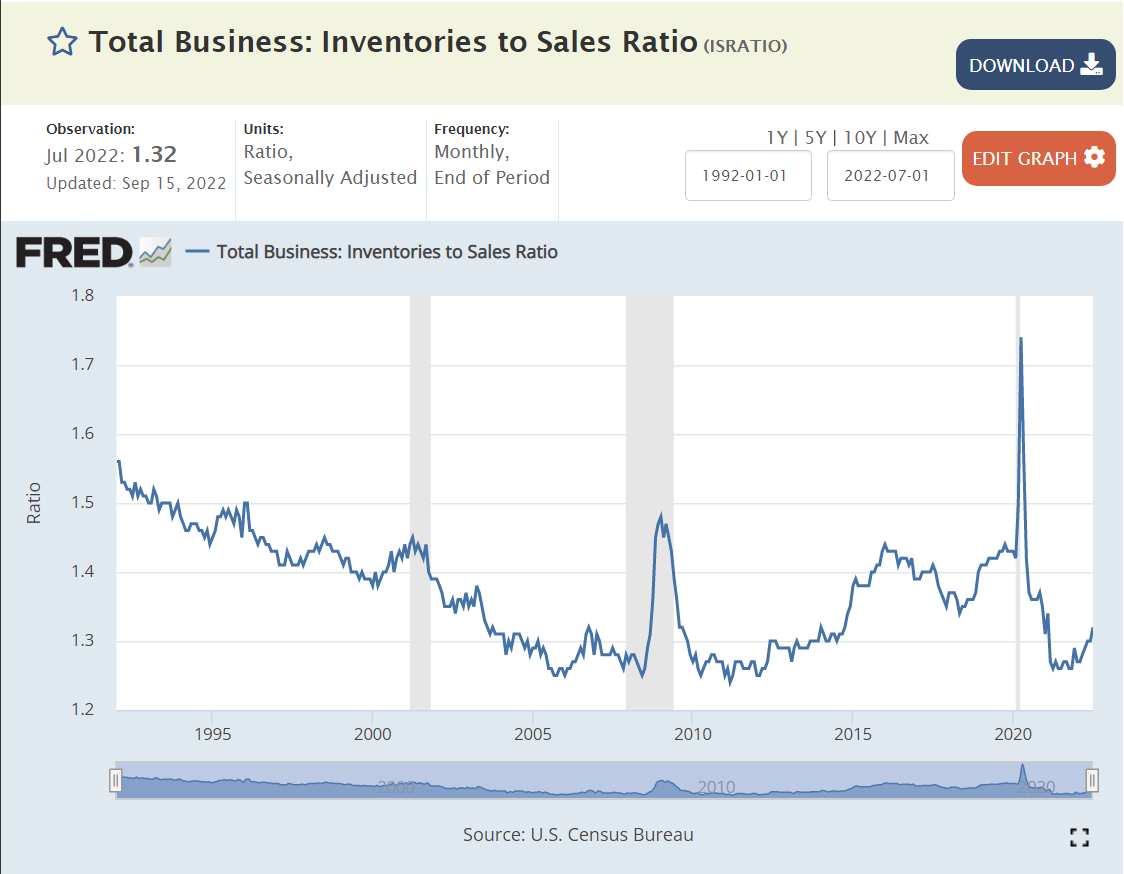

Most business cycle recessions show a clear build-up and subsequent liquidation of business inventories. Inventories were reduced (involuntarily) in the recovery from the pandemic and have increased a bit since then. There is no current indication of a pending “inventory recession”. In a “zero growth” retail holiday sales season, there will be some eternally optimistic retailers that have to cut prices to move goods, but this happens nearly every year.

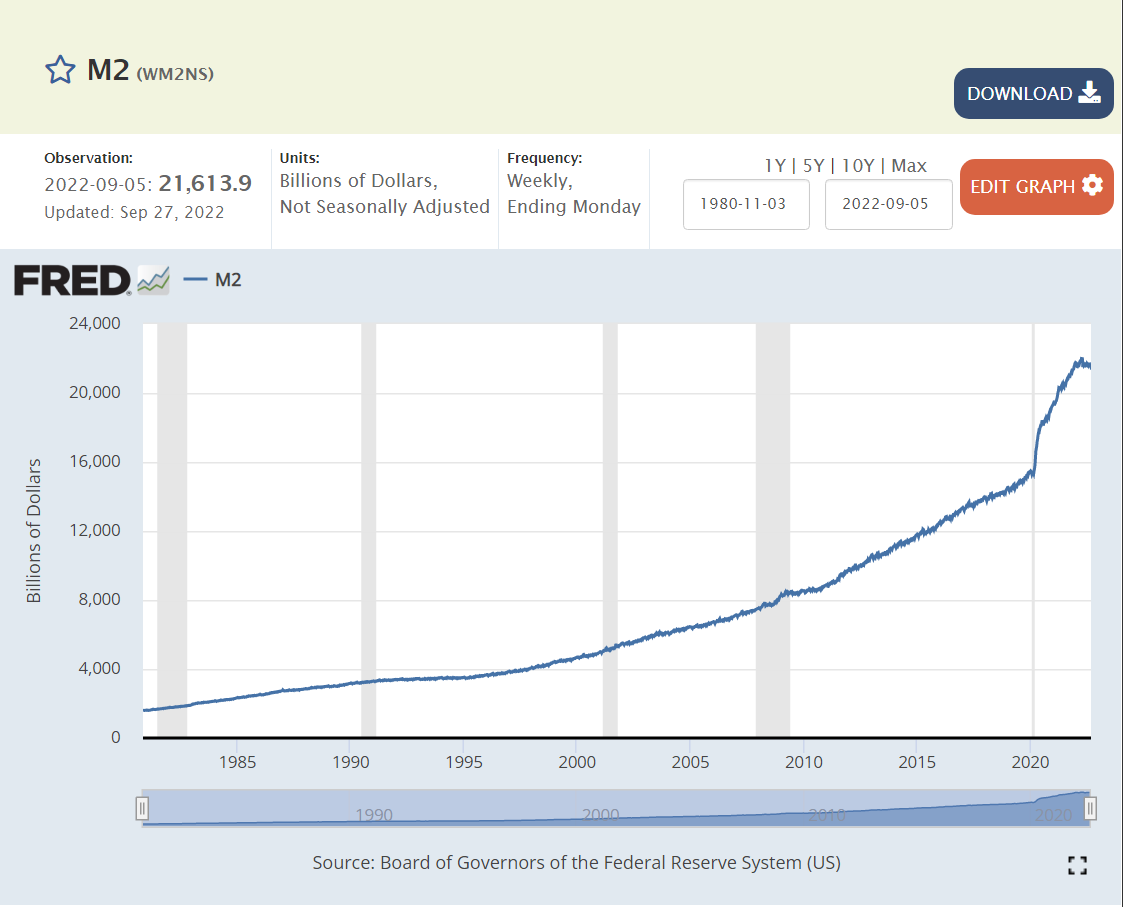

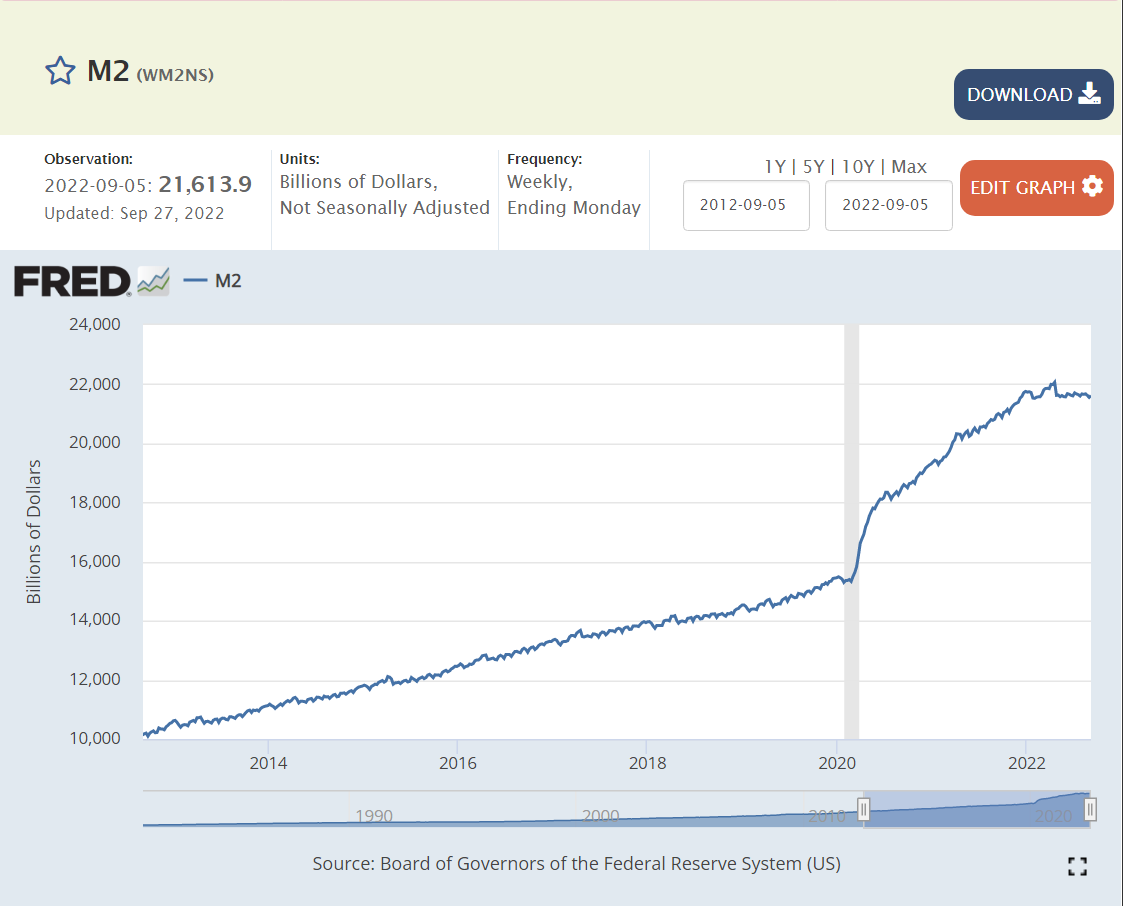

The Fed increased the money supply by an historically unprecedented 25% in response to the pandemic. And then by another 10% during 2021. In hindsight, the 25% was too much and the extra 10% was irresponsible. Fortunately, the money supply growth ended by the fourth quarter of 2021 and has remained flat.

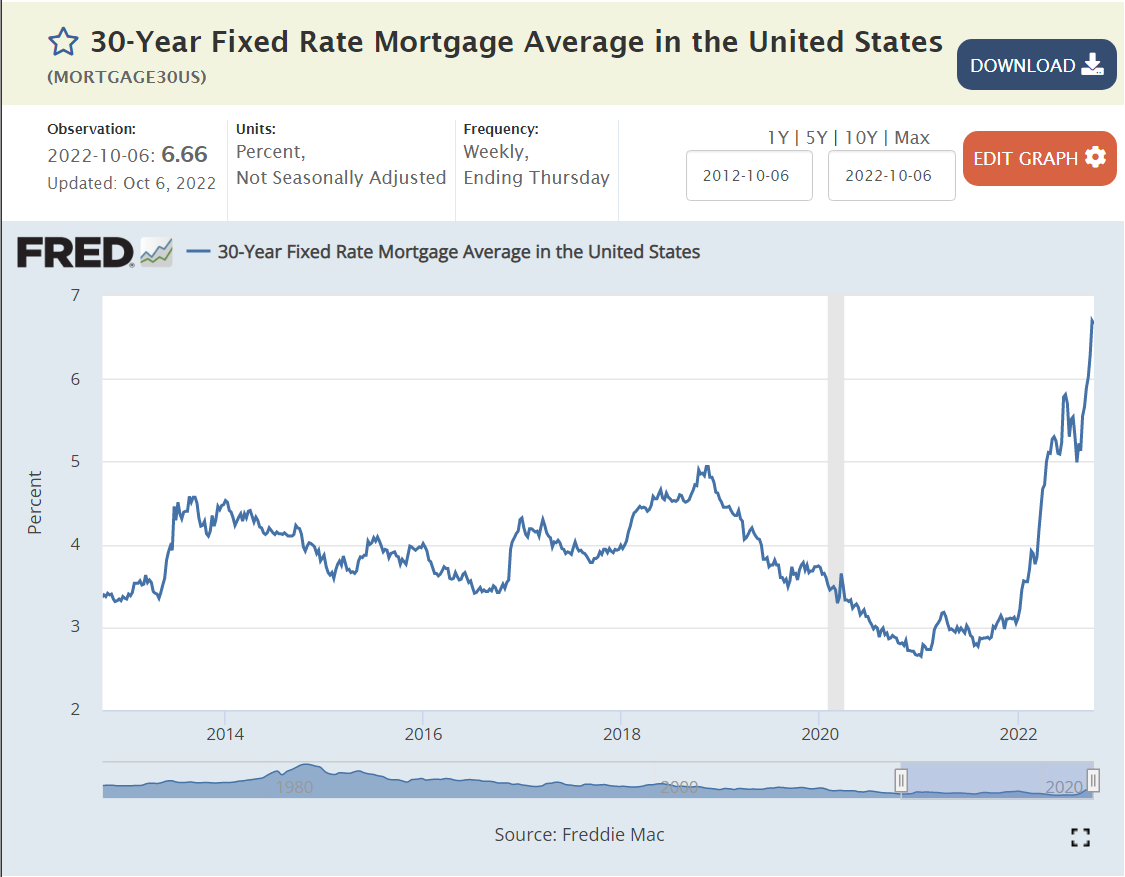

Mortgage rates were held to less than 3% for 2 years to support the recovering economy. They have now more than doubled, in excess of 6%. These higher interest rates will slow economic activity in many dimensions: lending, home buying, consumer credit, consumer spending, business investment, risk taking, stock prices, etc. Higher interest rates work with a lag to slow economic activity. They were still at “crazy low” rates at the end of 2021. The impact of higher rates is now being felt.

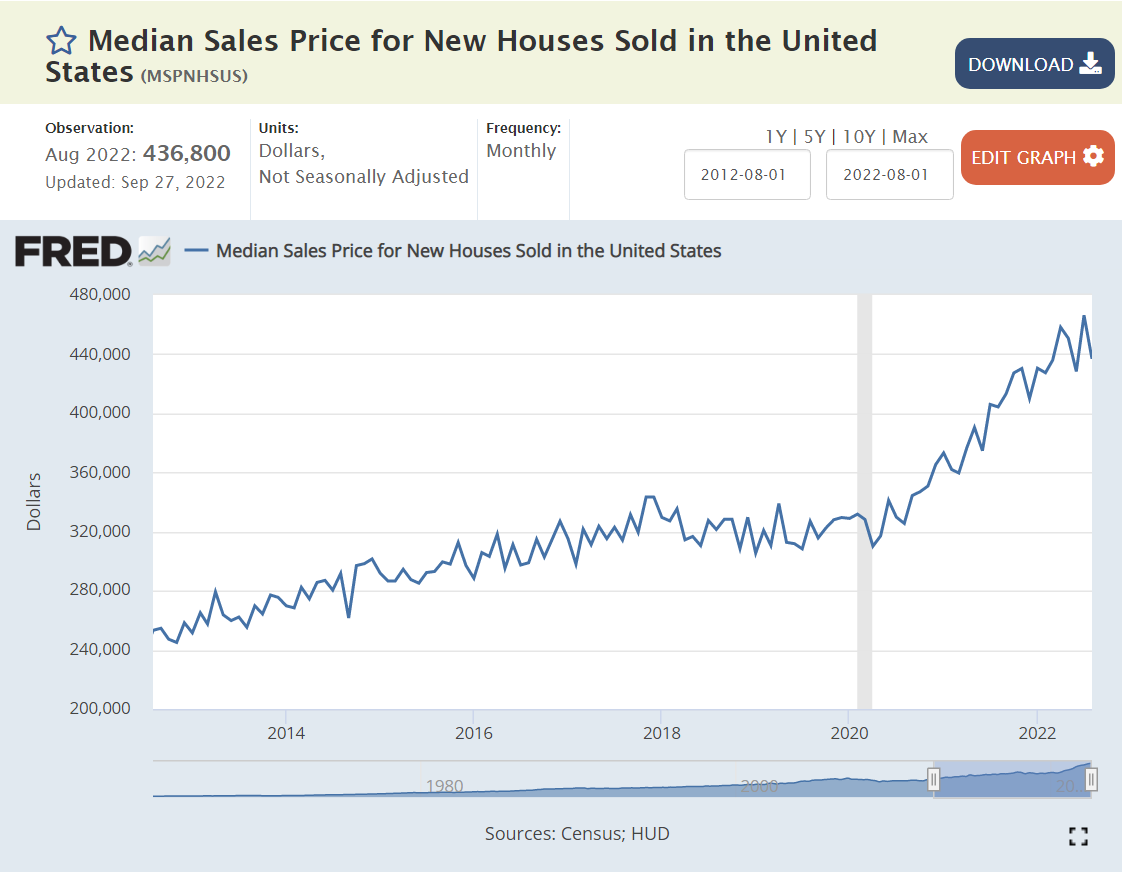

With extra savings, higher earnings, lower unemployment, restricted services available and historically low mortgage rates, consumer demand for housing grew rapidly while supply increased marginally. Housing prices (and rents) grew by 30%. Demand has now slowed. Housing inflation has slowed, perhaps to zero. This is a major channel through which GDP is decreased and inflation is reduced. Home purchases usually trigger thousands of dollars of additional move-in and fix-up expenditures.

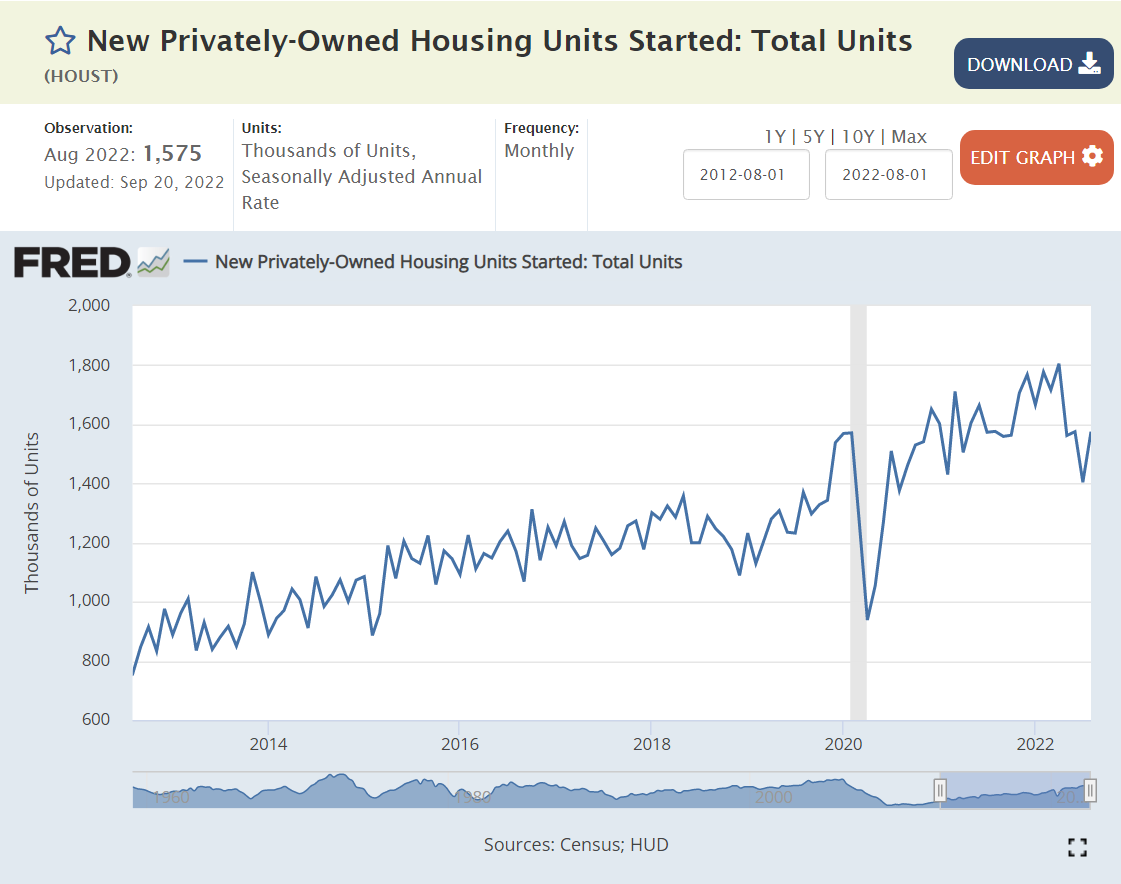

Housing sales and new housing starts have adjusted to the new interest rate environment. Note that the level of new housing starts remains above the pre-pandemic level, so some further decline is possible in the second half of 2022.

The US and global stock markets very quickly rebounded from the initial pandemic fear levels (-25%) back to the pre-pandemic levels which were more than 10% above the 2018-19 trend line. Stock markets increased after the initial pandemic recovery by 50% in line with growing profits. They have since dropped by one-quarter, a combination of lower expected future profits and higher interest rates increasing corporate financing costs and the cost of equity investors’ funds. Lower stock market prices usually have a negative “wealth” effect, with nominally poorer investors spending less in the current economy.

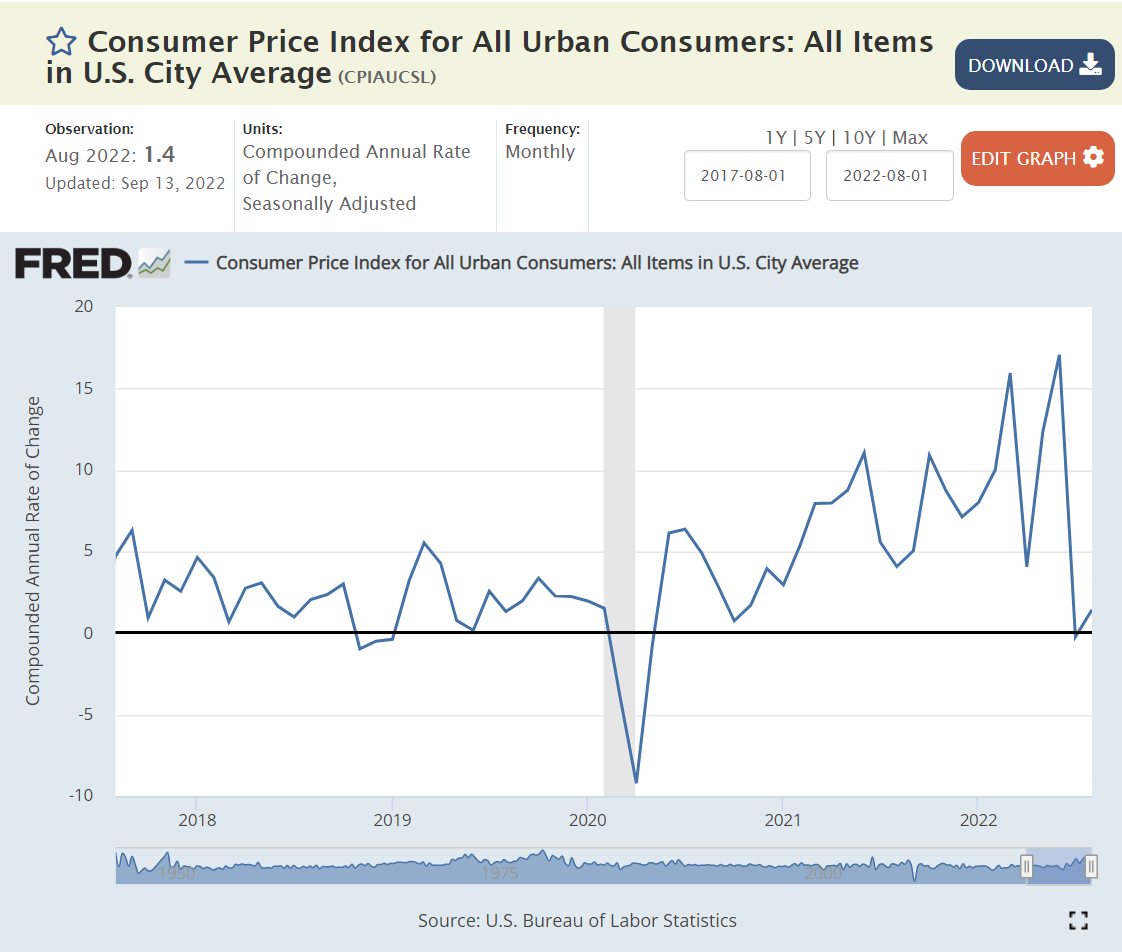

By the second quarter of 2021 we started to see 7-10% annual inflation rates. Increases finally slowed (or stopped) in the last 2 months. Reported inflation on a 12 months apart basis will remain above the 2% target level for the next 9 months, as high monthly inflation during the end of 2021 and the first half of 2022 remains in the measurements. Experts have a wide range of inflation forecasts for the first half of 2023, ranging from 3% to 8%. Most expect inflation to be close to the 2% target by the second half of 2023.

Producer price increases followed the same general pattern as consumer prices. They appear to have reached their peak. Producer prices better reflect global prices, especially the higher price of most commodities. Note the 30% increase in US demand for durable goods.

Global energy prices played a significant role in recent inflation. The last few months displayed an easing of prices, but recent OPEC+ decisions to reduce output indicate oil prices rising some again.

Job openings were at a historical high before the pandemic and quickly returned to that level by the end of 2020 and then nearly doubled in the next year+ as businesses saw opportunities to profit from the expanding economy, but could not find workers at the somewhat elevated prevailing wage rates. The number of unfilled jobs has dropped by nearly 2 million recently, from 12 to 10 million. The labor market is returning towards “normal”, but with 10 million open positions, the number of net new positions added is likely to increase throughout the fourth quarter, even as the Fed attempts to slow the overall economy.

The US labor force participation rate slid from 67% to 66% to 63% from 2000 to 2009 to 2015. It dropped by 1.5% due to the pandemic (61.5%) and has since partially recovered to 62.3%, still a full 1% below the recent peak rate just before the pandemic. The labor market recovery has been good, but not great.

The core, 25-54 year old labor force participation rate has increased by 1.5% since the pandemic to more than 82.5%, less than one-half percent below the recent high of 83% before the pandemic. By this measure, the labor market is recovering nicely, but not completely.

Retirement age workers have not returned to the work force, with more than 1.5% of potential workers choosing to not join the labor market. Employers will need to be more innovative to attract workers back into the labor market.

Summary

The economy is slowing down, inflationary pressures are easing, but the labor market still looks strong. Slow to zero growth for the prior (3rd) and next 3 quarters is likely as inflation falls from 7-8% to 2-4%. Unemployment rates may increase, but it appears that the total number of employees will increase slowly during this low/zero growth period.